Chief Investment Officer | Principal

The past year was challenging for professional market forecasters. As the year began, caution was in the air—and for good reason. In 2023 the S&P 500® Index produced a total return of 26.3%, ranking among the top 25 years in the index’s 97-year history. Resulting from that strong performance was a less-than-ideal starting position for 2024. One year ago, the index’s price sat at an elevated perch of 20 times its forward-earnings estimates, an above-average valuation that caused forecasters to urge caution regarding the year ahead.

Rather than producing subpar returns, however, the S&P 500® powered forward for another remarkable year in 2024, posting a total return of 25%. Since the index’s inception, such back-to-back 20%+ years have occurred only 12 times. Unsurprisingly, forecasters are again urging caution as we move into 2025, citing higher-than-average valuations as a good reason to do so. History, however, provides a different view: of the 11 prior back-to-back occurrences of 20%+ returns, the S&P 500® produced positive returns in the ensuing year eight times, with an average total return in year three of 9.7%.1

As interesting as these facts may be, we are not among forecasters offering views on next year’s market returns. As we illustrate below, today’s current stock prices offer questionable value in predicting next year’s return. Rather than presenting short-term views, we offer a longer-term perspective, more precisely 10-year expectations for returns of major investment asset classes. We trust that these expectations prove useful for both asset allocation and financial planning purposes.

“[T]ake advantage of what has happened instead of speculating on what may happen.”

This core tenet from Goelzer’s investment philosophy captures our approach to forming Capital Markets Expectations (CMEs). Conspicuously absent from what follows are assumptions about what might occur in the future, such as the impact of artificial intelligence on corporate margins or the effects of deglobalization on economic growth. You can find these prognostications in other CME presentations, many of which are worthy of reading.

In our experience, however, the more assumptions included in these forecasts, the more opportunity for errors. For that reason, we design our CMEs based on data that is already known and project existing, long-term trends to extend into the future. Our equity-return forecasts, for example, extrapolate the 20-year trend of U.S. corporate earnings 10 years into the future. To that trend we combine a regression-to-the-mean valuation to arrive at our 10-year return expectation. The simplicity of this model is its strength, and the model’s results have proven reasonable over the years.

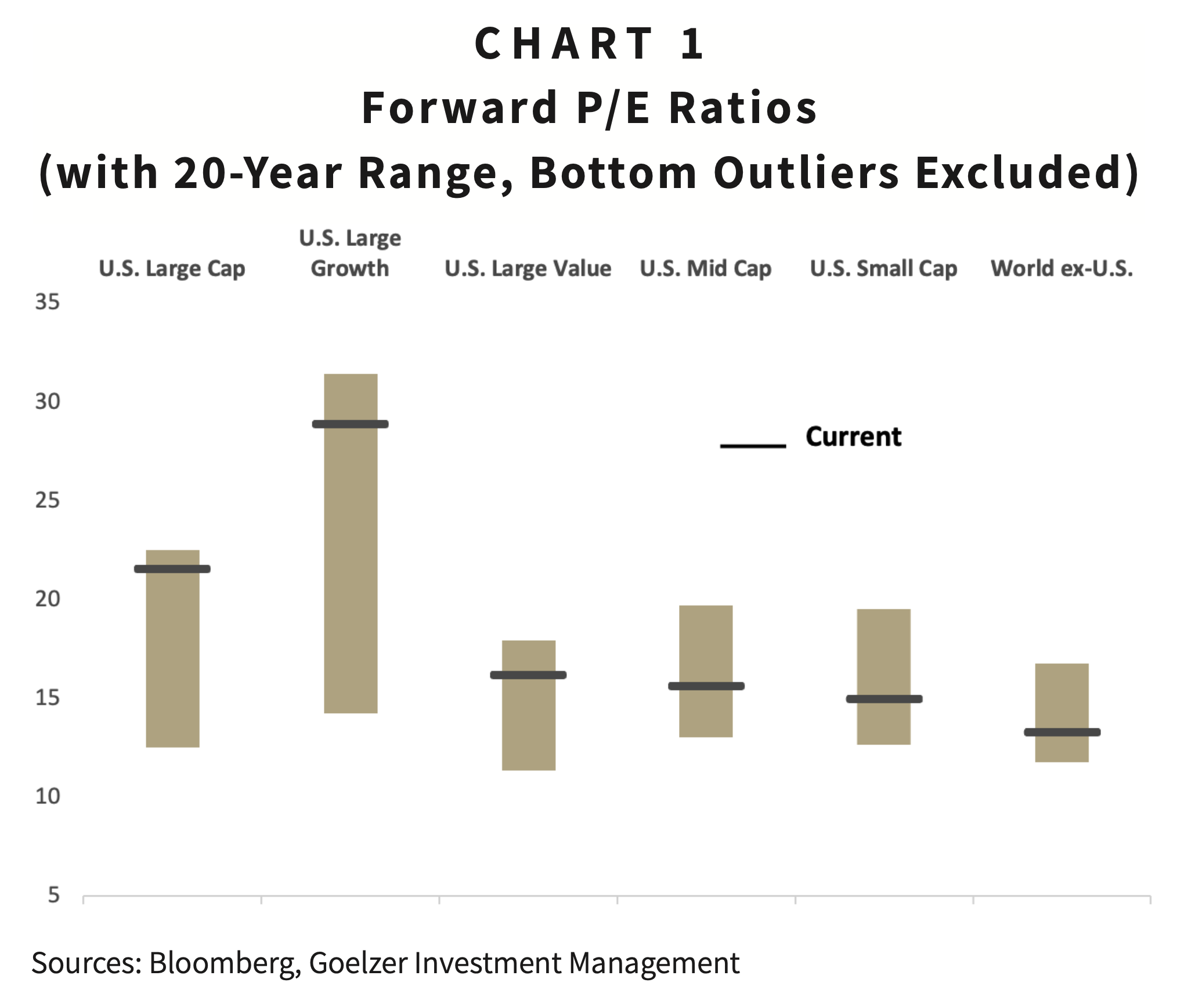

So what has happened that most affects forward return expectations? In equities, two years of 20%+ performance among U.S. large-cap stocks have left the S&P 500® Index well-above its long-term average valuation. As a result, our 10-year outlook for U.S. large-cap stocks compares less favorably to our outlooks from the prior two years. However, as we have noted in our other Insights papers, a select group of large technology stocks with high earnings growth have driven the bulk of the S&P 500®’s performance. Because many stocks outside of this select group have not equally participated in the S&P 500®’s ascent, we find better return potential in other sectors of the U.S. stock market, particularly among mid- and small-cap stocks.

As Chart 1 suggests, we also find relative opportunity in stocks outside of the U.S. That opportunity exists in part from the cheaper valuations of international stocks.2 However, those cheap valuations exist for a reason: for the past five years, earnings growth from the MSCI ACWI ex U.S. Index, which includes stocks in both developed and emerging markets, has been moribund. Our models do not expect a dramatic rebound in their earnings, but rather the continuation of an uninspiring trend of 1% growth.

The recent appreciation of the U.S. dollar and the relative cheapness of foreign currencies, however, give us cause for optimism on international stock returns. Cheaper foreign currencies should support the profitability of international companies, and the prospect of the dollar declining from its current level to its longer-term average should support the conversion of international stock returns into U.S. dollars. For those reasons—in addition to attractive starting valuations—our models point to marginally superior return prospects from international stocks relative to U.S. large-cap stocks.

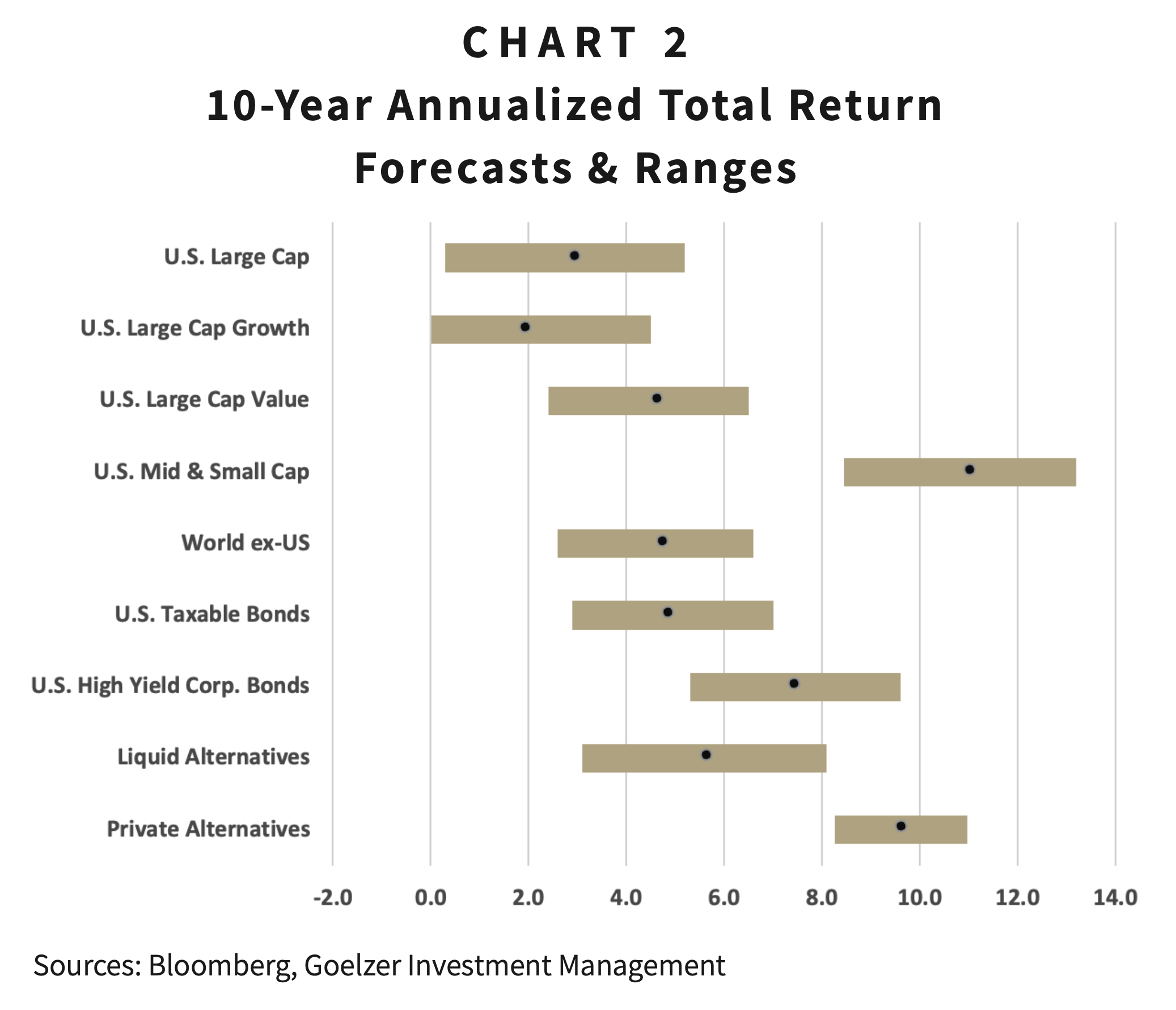

In fixed income markets, strong U.S. economic growth and persistent inflation concerns have kept interest rates above their long-term averages.3 These higher rates create a positive backdrop for bond returns, as sources both of income and of potential price return should interest rates fall. The latter prospect also supports our return outlook for alternative asset classes such as private equity, real estate, and private credit. Our comprehensive CMEs for 2025 are listed in Chart 2.4

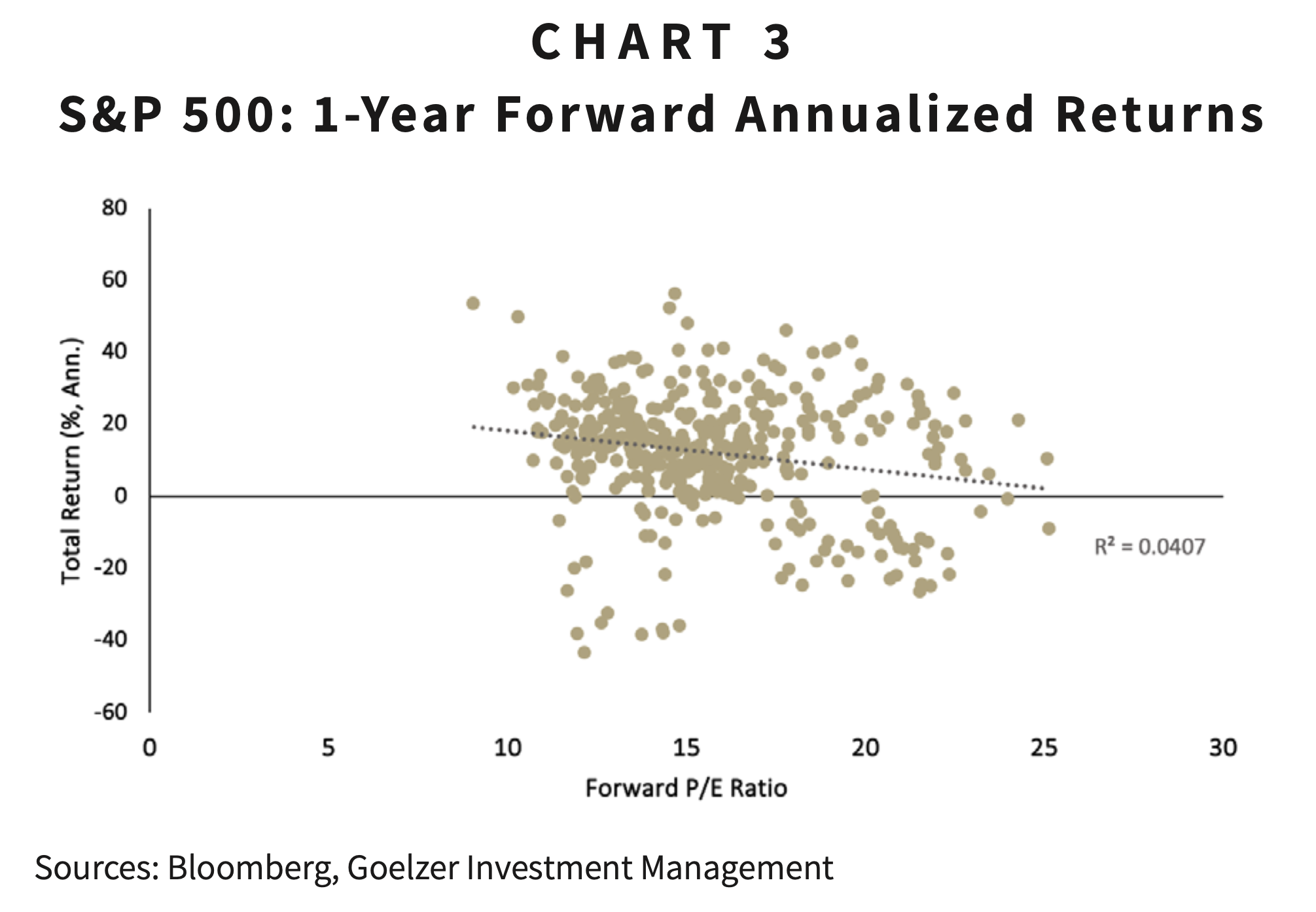

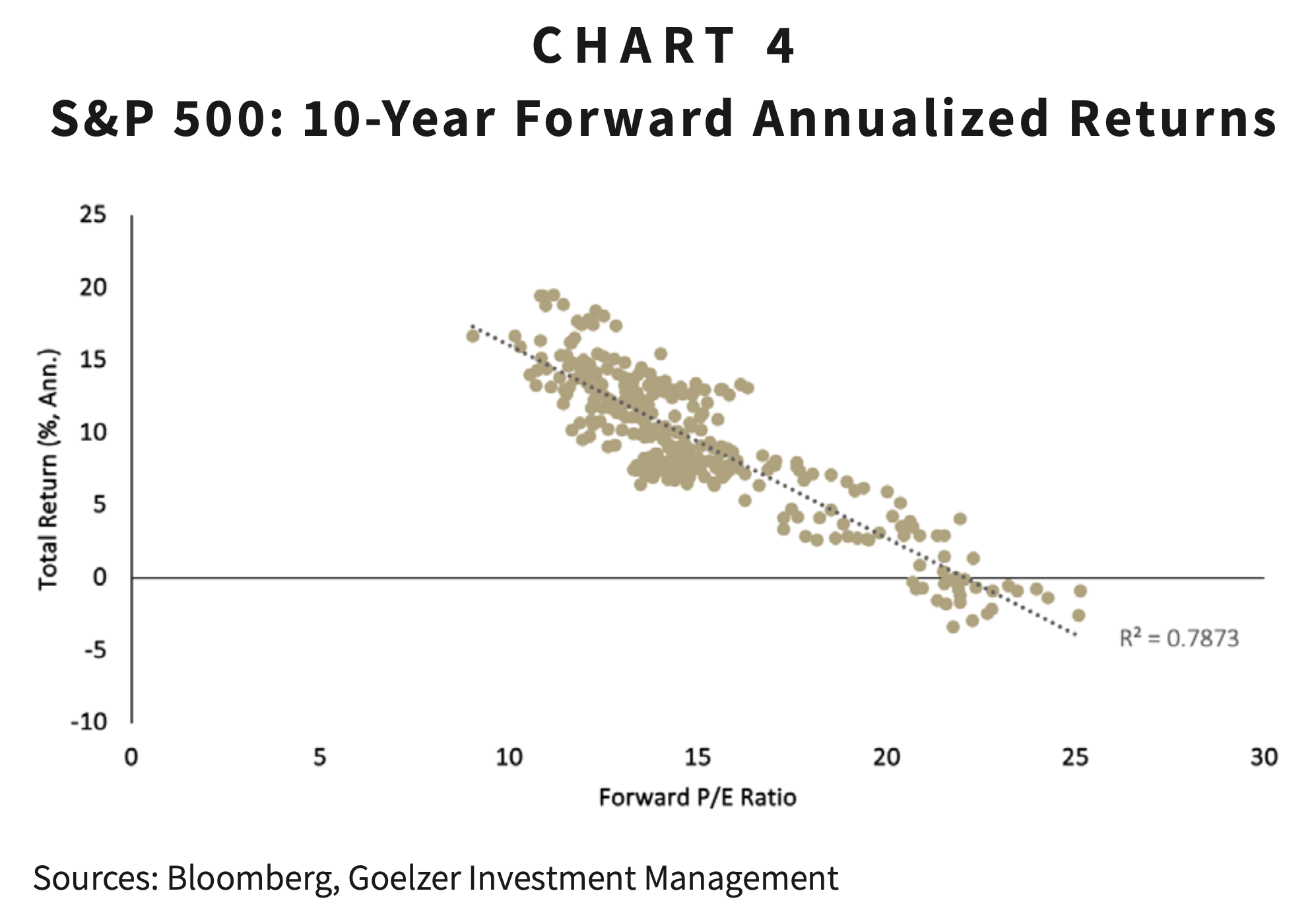

Past performance and the resulting valuation of major asset classes are key drivers of our return forecasts. However, as critical as valuation may be in determining long-term investment returns, valuation offers little help in predicting the near-term future. The charts below emphasize this point. Each chart begins with the S&P 500’s starting valuation and then plots the index’s return in the period that follows. The relationship between starting valuation and future returns strengthens as the return horizon extends. The convergence of plots on the second, 10-year chart illustrates that stronger relationship.

Charts 3 and 4 are also useful reminders of what our CMEs are—and are not—intended to show.5 Our forecasts are not short-term predictions of market returns; rather they are reasonable estimates of 10-year returns based on variables that have proven central to those returns over time. These estimates also provide a view of potential relative returns across asset classes, a view that is critical to making sound asset-allocation decisions.

In addition to offering specific long-term return forecasts, we have also placed ranges around each of our asset-class expectations. These ranges are equally critical for asset-allocation decisions. Asset classes with more volatility may indicate a relatively high expected return, but also a wider range of potential returns. In other words, the volatility of that asset class may result in a lower realized return than an asset class with a lower expected return, yet a tighter range of expected returns. Therefore, a naive allocation to the asset class with the highest expected return may not deliver the optimal investment outcome.

The past two years of strong performance of the S&P 500® Index admittedly results in a modest 10-year outlook for U.S. large-cap stock returns. To that point, we should note that all forecasts are based on a single point, namely December 31, 2024. As the future unfolds and markets change, our forecasts will also change. Temporary stock-market declines, for example, could result in less-expensive valuations and higher expected returns for investors with cash to invest or portfolios to rebalance. Investors with well-crafted investment plans and the discipline to act on them should be well suited to meet the occasion.

1S&P 500 Index, total returns, as of December 31, 2024. Data accessed from Bloomberg.

2 Valuation based on 20-year average forward price-to-earnings ratios, quarterly observations. Excludes bottom 20% of observations over the 20-year period. Indexes used include the following: S&P 500, Russell 1000 Growth, Russell 1000 Value, S&P Mid Cap, S&P Small Cap, and MSCI ACWI ex-US. Data as of December 31, 2024.

3 The 20 and 30-year average yields-to-worst of the Bloomberg U.S. Aggregate Bond Index were 3.29% and 4.13%, respectively. As of December 31, 2024, the index’s yield-to-worst was 4.91%.

4 Indexes used include the following: S&P 500, Russell 1000 Growth, Russell 1000 Value, S&P Mid Cap, S&P Small Cap, MSCI ACWI ex-US, Bloomberg U.S. Aggregate Bond, and Bloomberg U.S. Corporate High Yield. Liquid alternatives forecast is based on long-term trends for commodities, public real estate, and other public equity and fixed income strategies included in Goelzer’s Non-Traditional Strategy. Private alternatives forecast is based on a buildup methodology and assumes an equal allocation to private equity, private credit, and private real estate. Forecasts as of December 31, 2024. Return estimates are based on market indexes and do not represent Goelzer portfolios or investment strategies.

5 S&P 500 Index, total returns from December 31, 1994 through December 31, 2024.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.