Gavin W. Stephens

CFA

Chief Investment Officer

Chief Investment Officer

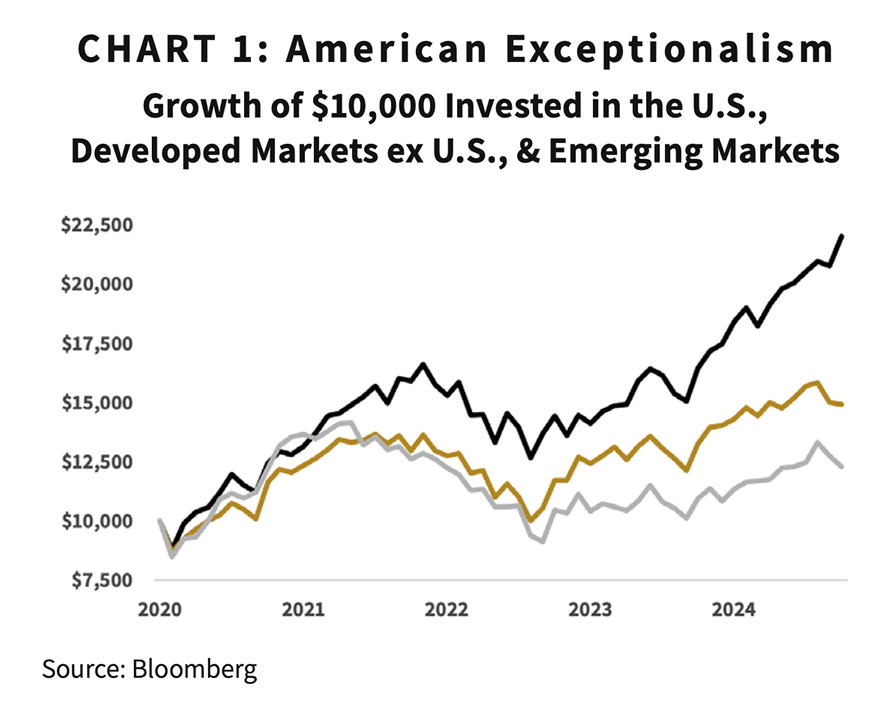

For the past decade, the U.S. economy and stock markets have been the envy of the world. Aided by the growth of its technology sector, the U.S. economy grew at an average rate of 2.7% over the past 10 years, while major developed economies such as the EU and Japan grew at much slower rates of 0.4% and 0.8%, respectively.1 Combined with this higher growth, relatively higher interest rates in the U.S. helped attract capital, sending the prices of U.S. stocks and other assets higher. During this period, the U.S. stock market assumed the largest share of total world market capitalization in 30 years (67%), leading many to describe this period as one of “American Exceptionalism.”2 Investors in U.S. stocks have fared much better than investors in other developed or emerging markets, as Chart 1 shows.3

For the past decade, the U.S. economy and stock markets have been the envy of the world. Aided by the growth of its technology sector, the U.S. economy grew at an average rate of 2.7% over the past 10 years, while major developed economies such as the EU and Japan grew at much slower rates of 0.4% and 0.8%, respectively.1 Combined with this higher growth, relatively higher interest rates in the U.S. helped attract capital, sending the prices of U.S. stocks and other assets higher. During this period, the U.S. stock market assumed the largest share of total world market capitalization in 30 years (67%), leading many to describe this period as one of “American Exceptionalism.”2 Investors in U.S. stocks have fared much better than investors in other developed or emerging markets, as Chart 1 shows.3

A challenging first quarter for U.S. stocks—and an even more dramatic selloff to begin the second quarter—has thrown this trend into question. Some economists and market strategists have even gone so far as to suggest that we are now facing “the end of American Exceptionalism.”4 In what follows, we note how this sentiment has shifted so dramatically and acknowledge the real challenges facing the U.S. economy and financial markets. While these challenges are formidable, we ultimately propose that the unique characteristics of the U.S.—particularly its demographic advantages and its culture of innovation—should not spell the end of this exceptional era.

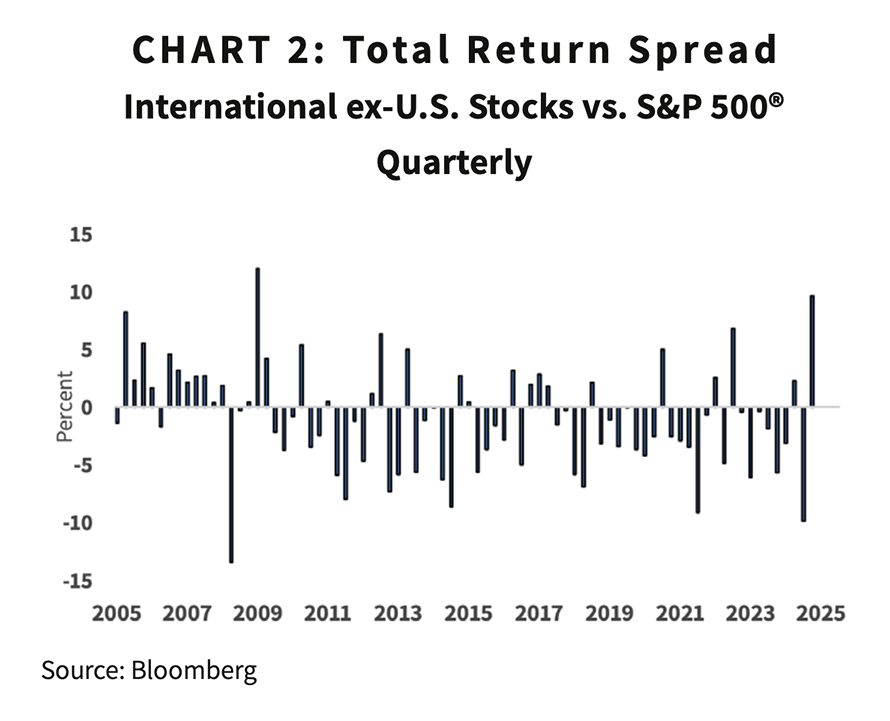

While the first quarter was a challenging period for investors in U.S. stocks, it delivered a dramatic turnaround for international stocks, which outperformed U.S. large-cap stocks by nearly 10%.5 To be sure, this year’s outperformance of international stocks is largely a simple reversal of last year’s underperformance. As many noted at the year’s outset, large-cap U.S. stocks, especially those of higher-growth companies, were trading at historically high valuations and were “priced for perfection.”

The elevated prices of U.S. large-cap stocks resulted from a remarkable two-year run for the S&P 500®. That rally gained steam following the fall elections, the results of which investors interpreted as favorable for U.S. corporate earnings and stock prices.

Optimism over the U.S. economy and corporate earnings has begun to fade, however. The expansion of tariffs on imports—which, as announced, could cover over 60 countries—is estimated to raise the U.S.’s effective tariff from about 3% to a rate as high as 25%.6 As the stock market made evident in the days following the announcement of these broad tariffs, investors are generally skeptical of tariffs’ ability to contribute to economic growth. Rather, the pass-through effects of tariffs—in the form of higher consumer prices, lower corporate margins, and reduced global trade—have led analysts to lower their expectations for the near-term growth of the economy and corporate earnings.

In addition, while the U.S. government is focused on reducing its level of fiscal spending, governments in Europe are pursuing expansionary fiscal policies to bolster infrastructure and defense. The net effect, especially in the first quarter of the year, was an improved growth outlook for Europe and a more pessimistic one for the U.S.

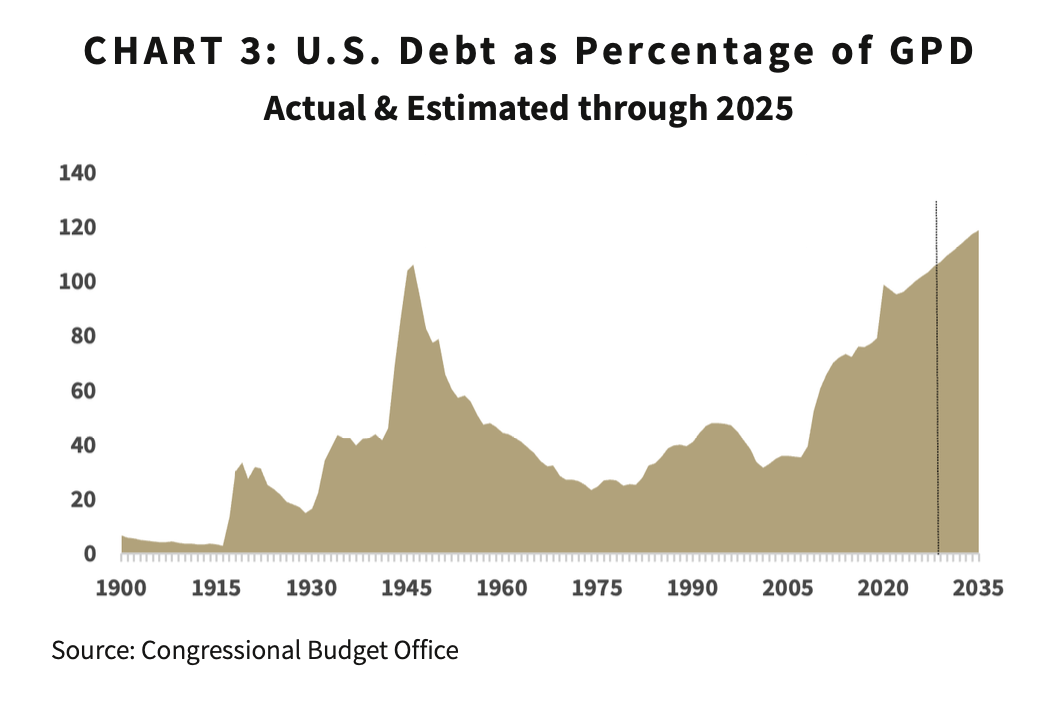

In addition to anxiety over near-term economic growth, investors are increasingly concerned about the U.S.’s growing debt. In 2024, the U.S. budget deficit reached 6%, and its overall debt increased to nearly equal the country’s GDP.7 As interest rates have risen in recent years, the cost of servicing that debt has become more onerous. See Chart 3.

Federal spending on interest is now the second-largest line item in the federal budget—behind only Social Security—and ahead of defense and Medicare.8 Attempts to reduce federal spending may help slow this trajectory, along with potential income from increased tariff duties. In the meantime, the increasing U.S. debt burden raises the specter of even sharper federal budget cuts or higher taxes in the future—both of which would cloud the economy’s growth prospects.

Those questioning the durability of America’s exceptional era are correct to note these real challenges that the U.S. faces. Yet, as challenging as these issues may be, the U.S. maintains long-term, seemingly durable advantages that should help the country retain its status as the preeminent economy for investment. Among these advantages are favorable demographics and a culture of risk-taking and innovation supported by deep, liquid capital markets.

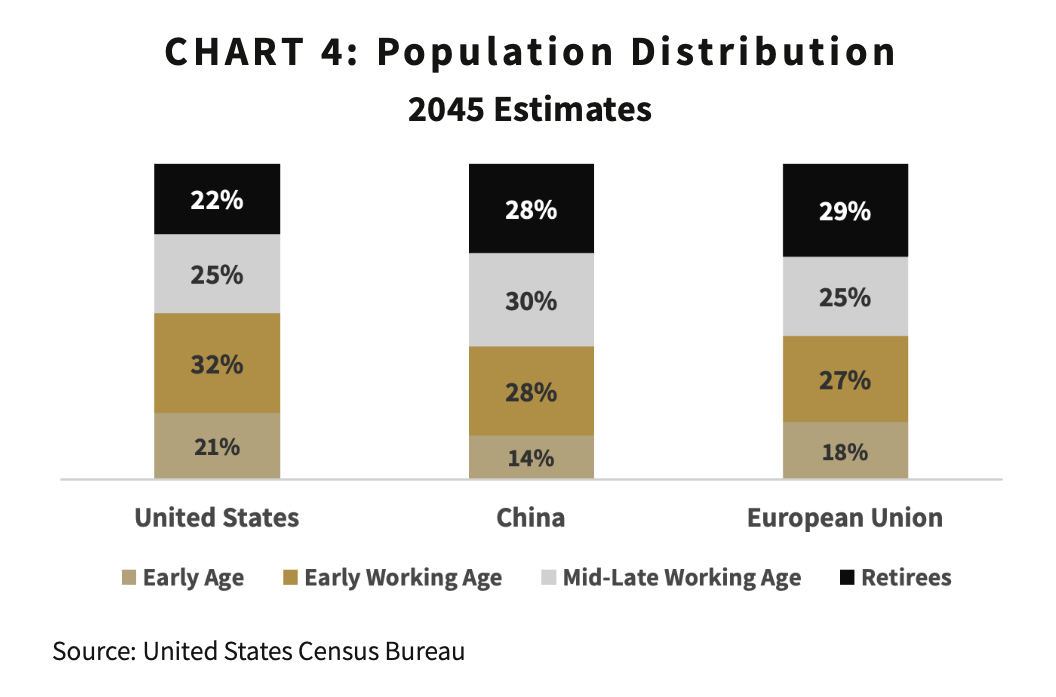

In the U.S., the transition of the large Baby Boomer generation from the workforce to retirement has gathered significant attention. That transition, of course, has many implications for the economy and specific industries. Lost among those headlines, however, is the relatively large number of new entrants into the workforce and the large group that will enter it in the coming years. As the chart below shows, relative to both China and the EU, the U.S. has a significantly greater proportion of people who are either in the early-to-middle stages of their careers or not yet in the workforce.9 See Chart 4.

As the workforce of the U.S. grows proportionally larger than those of China and the EU, the U.S. economy should benefit from more economic output, higher investment in technology and infrastructure to support this workforce, and greater consumption as these workers earn wages. Comparatively speaking, this simple difference in population distribution offers the U.S. a basic and powerful economic advantage.

Less tangible, but also powerful, is the American culture of risk-taking and the legal and financial institutions that support it. It is well known that the U.S. is home to the largest corporations in the world, including those most closely associated with the development of artificial intelligence. Perhaps less appreciated, however, is the underlying financial and legal ecosystem that supports this risk-taking culture. The U.S.’s broad and deep capital markets have allowed many more companies to be incubated, grown, and ultimately taken public over the years. Low tax rates on capital gains also encourage investment into the economy.10 Finally, well-defined bankruptcy laws provide support for failure and implicitly encourage risk-taking. These factors, among others, have led the U.S. to consistently rank among the top countries in the Global Innovation Index.11

Perhaps the degree to which investors considered America exceptional was never entirely realistic. The combined value of the U.S.’s Magnificent Seven stocks, for example, had grown to exceed the value of the entire European stock market by the end of last year.12 An adjustment in expectations for those U.S. companies is reasonable. More concerning, however, are the clouds forming over the economy, whether in the form of changing trade relationships or growing government debt. While last year’s boom may indeed be fading, the U.S.’s advantages in people, institutions, and ethos should persist—keeping its status as exceptional intact.

1 Average annualized growth in quarter-over-quarter real GDP from 2015 through 2024. Data accessed via Bloomberg. China—the world’s second largest economy by GDP following the U.S. and the EU—averaged 5.9% over these same 10 years. However, that growth rated decelerated over the prior decade while the U.S.’s growth rate accelerated.

2 Market capitalization of the MSCI USA Index as a percentage of the market capitalization of the MSCI All World Equity Index. Data accessed via Bloomberg.

3 U.S. stock market represented by the S&P 500 Index. Developed markets ex U.S. represented by the MSCI EAFE Index. Emerging Markets represented by the MSCI Emerging Markets Index. Illustration of hypothetical investment in representative indexes, assuming total returns, gross dividends. Illustrated returns do not represent performance of Goelzer strategies.

4 Rebecca Patterson, “America’s Economic Exceptionalism Is on Thin Ice,” The New York Times, March 21, 2025, nytimes.com/2025/03/21/opinion/trump-economy-us-exceptional.html.

5 MSCI All World ex U.S. Index and S&P 500, quarterly total returns as of March 31, 2025. Accessed via Bloomberg.

6 Bill Dudley, “Stagflation Is Now America’s Best-Case Scenario,” Bloomberg, April 7, 2025, bloomberg.com/opinion/articles/2025-04-07/stagflation-is-now-america-s-best-case-scenario.

7 The Budget and Economic Outlook: 2025 to 2035, Congressional Budget Office, January 17, 2025, cbo.gov/publication/60870.

8 Niall Ferguson, “Debt Has Always Been the Ruin of Great Powers. Is the U.S. Next?,” The Wall Street Journal, February 21, 2025, wsj.com/politics/policy/debt-has-always-been-the-ruinof-great-powers-is-the-u-s-next-02f16402.

9 International Database (IDB), U.S. Census Bureau, census.gov/data-tools/demo/idb. The U.S. is the largest economy in the world as measured by Gross Domestic Product ($27.9T), followed by the EU ($18.5T) and China ($17.7T).

10 For example, the U.S. has a progressive capital-gains tax system ranging from a 20% tax rate on long-term capital gains for high-income earners while the equivalent tax rate is 26.375% in Germany and 30% in France.

11 World Intellectual Property Organization (WIPO) Global Innovation Index 2024, September 26, 2024, wipo.int/pressroom/en/articles/2024/article_0013.html.

12 Bloomberg Magnificent Seven Index (Apple, Microsoft, Amazon, Nvidia, Alphabet, Meta Platforms, and Tesla) and Bloomberg Euro 600 Index, market capitalization as of December 31, 2024.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.