Director of Wealth Planning | Senior Wealth Advisor

Principal

Morgan Housel in his book, Psychology of Money, discusses a phenomenon that is the obsession of many but achieved by few: creating significant wealth, as quickly as possible. He says that creating wealth involves “taking risks, being optimistic, and putting yourself out there” and probably an element of luck.1 Remaining wealthy, however, requires a different approach and mindset, a mindset that includes a level of humility, fear, and frugality. The key is knowing when and how to shift mindsets.

Rapid wealth creation can arise from holding a large position in a successful private or public company stock that has appreciated significantly. Whether the stock position was obtained through purchases, equity compensation (restricted stock, stock options, performance shares, etc.), or inheritance, once its size rises above 10% of your total portfolio, it is considered a concentrated position.

Some may consider that threshold low, as a holding equal to 10% or slightly more of your portfolio is not a significant threat to your standard of living should it decline in value. However, for many individuals that have gained wealth through a single stock, it often represents 50% or more of their portfolio’s value. At such highly concentrated levels, the stock that created their wealth becomes the largest risk to losing their wealth.

If you are in that situation, it is critical that you address the concentration. In doing so, remember that the financial purpose of each holding in your portfolio is to provide an attractive risk-adjusted return. Once a position reaches concentration level in your portfolio, added emphasis should be placed on the risk side of that equation.

Our experience in working with investors who have a concentrated holding is that they typically are divided into two camps, both with good reasons. The first is those who choose to do nothing. The second is those who want to do something but need help working through their options.

Doing nothing, and continuing to hold the concentrated position, is a common course of action. There are many reasons for this, including a belief that the stock will continue to appreciate, a reluctance to pay capital gains taxes, and feelings of loyalty or sentimentality regarding a stock.

If you are inclined to do nothing, you should ask yourself the following questions:

If the concentrated stock position were to drop significantly, will that substantially compromise my goals and lifestyle?

Is the stock’s price reasonable compared to the company’s fundamentals?

A valid tax reason for doing nothing applies to those who are late in life. Current tax law permits a stepped-up cost basis on your assets upon death, thereby eliminating tax on built-up unrealized gains as assets are passed on to your heirs. The tax savings from the stepped-up cost basis can be substantial and need to be considered in such cases. However, the risk of a sudden loss of value remains, so investors in this situation may want to consider different hedging options for their holding.

Regardless of your conclusions, remember that you are not faced with an all-or-nothing decision. By shifting to a mindset of staying wealthy, you can take meaningful actions to reduce your risks. We outline some of those actions below.

For investors wanting to reduce the risk of a concentrated stock holding, we recommend reviewing your options, beginning with the simplest and then considering the more complex depending upon your situation.

The simplest action to consider is selling or trimming the concentrated position. A systematic selling strategy at regular intervals may be the best approach. This can take emotion out of the equation and potentially spread out the tax liability if done over more than one tax year. You can also deploy a systematic strategy to accelerate selling when the stock’s price is at the higher end of a predetermined range and reduce the number of shares sold when it is at the lower end of the range. Proactive tax planning should be considered with this strategy to avoid moving into higher tax brackets as you realize capital gains on the sale of these positions. Selling other holdings with losses can help offset capital gains realized from the concentrated position.

Another consideration is where the sale proceeds will be reinvested. If the stock being sold is paying dividends, is there a need to replace this income stream? Or is it important to reinvest into a diversified stock portfolio that can continue to provide growth opportunities?

Another way to reduce a concentrated holding is through annual gifting. In 2024, federal law permits individuals to gift up to $18,000 to each person they choose without utilizing part of their lifetime exemption or being required to complete a gift-tax return. For example, if a couple has four adult children and eight grandchildren, they could give $432,000 in 2024 without using any of their lifetime exemption. Imagine how several years of gifting at this pace could substantially reduce a concentrated holding and potential future estate taxes.

Gifting can be a great way to benefit future generations during your lifetime, but it’s important to consider the tax consequences. Unlike assets passed through your estate, gifted assets do not receive a step up in cost basis. Recipients of gifted stock will owe capital gains taxes based on the original owner’s cost basis when they sell the holding. If the recipients are subject to lower tax brackets, this may be a beneficial action to consider.

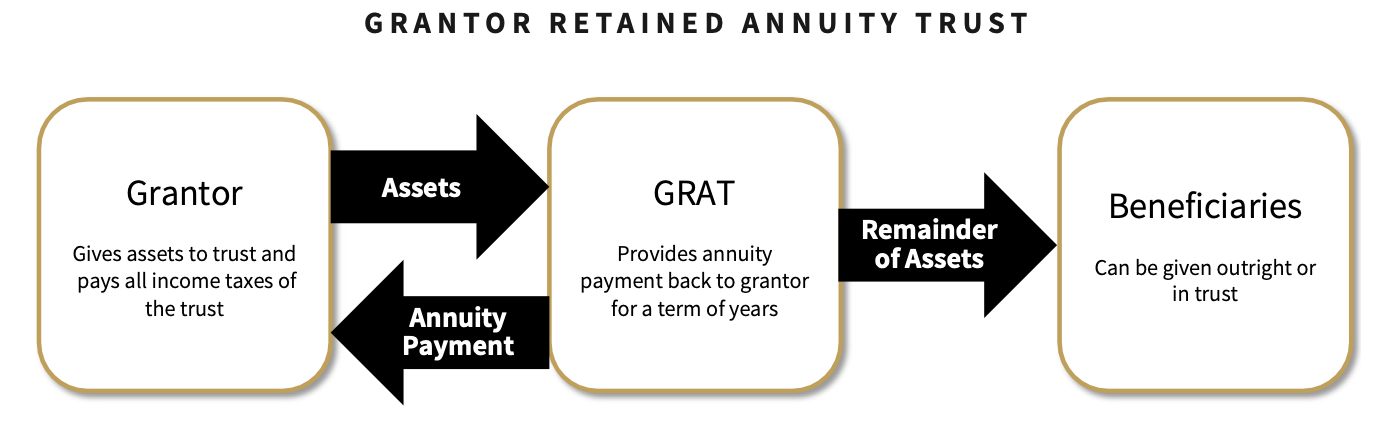

Individuals wanting to gift larger amounts, may wish to employ the use of a Grantor Retained Annuity Trust (GRAT). This strategy allows you to gift a portion of any future appreciation to the next generation. While this does not reduce your current exposure to a concentrated position, it can place a lid on that exposure by moving the stock’s future appreciation from you to the trust’s beneficiaries. If you believe the stock has strong future appreciation potential, you might consider this option. Note that shares that are transferred to beneficiaries through a GRAT do not receive a step up in basis. This can be rectified by substituting cash or other assets for the low-basis stock if the trust document permits.

If you have charitable intent, donating shares to a charity or donor-advised fund can help to reduce a concentrated holding in a tax efficient manner. When you donate stock with low cost basis, you also donate the unrealized capital gains, thus avoiding the tax liability created if you were to sell the stock. You are also eligible to receive a federal tax deduction for the fair-market value of the stock up to 30% of your adjusted gross income (AGI), provided the stock is donated to a qualifying charity or donor-advised fund. Donations of appreciated stock can also work in conjunction with a sale of shares of that same appreciated stock. This allows you to reduce your overall exposure, while creating liquidity and offsetting a portion of the realized gains with the charitable deduction.

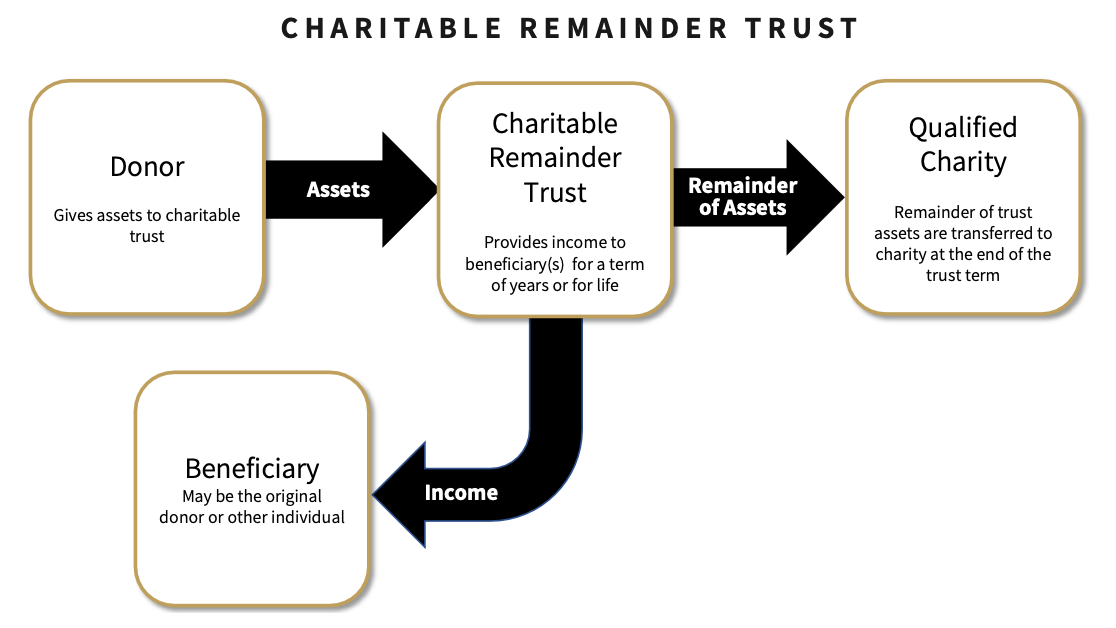

Another charitable strategy to consider is the Charitable Remainder Trust (CRT). A concentrated position can be gifted into a CRT, which can in turn provide income via an annuity stream to one or more individual beneficiaries while also providing a donation to a charity or charities at the termination of the trust. Typically, the concentrated position is sold within the CRT and reinvested into a diversified portfolio. The CRT structure allows for the taxation on capital gains to be spread over a period of years as a portion of distributions to the individual beneficiaries.

The tradeoff for this more favorable taxation is that you only receive a partial tax deduction based on the present value of the remainder distribution to the charitable beneficiary. However, since the CRT pays out an annuity stream, it can be an excellent way to replace or increase the income lost from the holding used to fund the CRT. By removing the gifted assets from your estate, you may also reduce future estate tax.

While complex and not for everyone, derivatives-based hedging strategies can be employed to limit or mitigate downside risk and, in some cases, generate income.

Here are some strategies to consider:

Put options can protect against future losses if the stock declines. When you buy a put contract, you are given the right, but not the obligation, to sell your stock at the predetermined strike price. Should the stock’s price fall below the strike price you can choose to either sell the stock or sell the put option. The put option’s price will reflect the difference between the stock’s price and the strike price. You would use this strategy if you wanted to retain the stock, but you are concerned about a sudden loss in its value.

This strategy involves selling a call option (a right to purchase a stock) for a premium payment on the stock position that you own. The buyer of the call option has the right to purchase the specified number of shares from you at the strike price. If the stock price doesn’t reach the strike price within the option’s term, the option will expire, and you will keep both the option premium and your stock. If the stock price rises above the strike price, you are obligated to sell your committed shares. While the premium can create some cash flow, you must be prepared to sell the shares covered by the call. This strategy is often used in conjunction with a systematic plan to sell or trim a concentrated holding.

A collar combines the above-mentioned put and call strategies. Typically, you would purchase a put option to limit downside loss, while selling a call option to generate income that will offset some or all of the price of the put option. With a collar strategy, you are putting in place both a floor and a ceiling on the stock’s price. Therefore, it both limits your potential losses and your potential gains.

A concentrated position in a single company has created great wealth for many investors. Once achieved, however, the strategy that created the wealth can become the strategy that takes it away. So whether you are comfortable or not with the risks provided by a concentrated holding, it is important to know your options. For decades, the team at Goelzer has helped clients with concentrated holdings. We consider your individual needs and incorporate tax planning to assess the merits and drawbacks of any single strategy or combination of strategies.

Some of the strategies outlined above take the time and coordination of other professionals such as CPAs and attorneys to execute That time and coordination is worth the effort. Do not miss an opportunity to better position you and your heirs to not only preserve but, more importantly, benefit from your wealth.

1 Getting Wealthy vs. Staying Wealthy, An excerpt from the book The Psychology of Money, Morgan Housel, November 29, 2022, collabfund.com/blog/getting-wealthy-vs-staying-wealthy.

DISCLAIMER: This report includes candid statements and observations regarding financial planning strategies; however, there is no guarantee that these statements will prove to be correct. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.