Director of Wealth Planning | Senior Wealth Advisor

Principal

As Thanksgiving approaches, our thoughts often shift to loved ones and our communities. The season of giving also begins with Giving Tuesday taking place the week after Thanksgiving. Many people have annual gifting plans that benefit both charities and loved ones. With the volatility in the markets and conflict across the world, does it still make sense to consider sharing your wealth with others? If so, what are the most tax efficient ways to share wealth?

In addition to charitable gifts, many individuals choose to gift to family and friends.

Annual gifting allows individuals to gift a maximum of $16,000 (soon to be $17,000 in 2023) per recipient each year without utilizing their lifetime exemption. The lifetime exemption is the amount that passes free from federal estate tax. Currently an individual with more than $12.06 million ($12.92 million in 2023) and couples with more than $24.11 million ($25.84 million in 2023) would have taxable estates. Amounts over these thresholds are taxed at rates up to 40%.

While few people have taxable estates now, the sun is literally setting on these amounts. In 2026, barring further action, the tax rates will sunset back to the 2017 tax rates (adjusted for inflation) in place prior to the Tax Cuts and Jobs Act. If this occurs, the lifetime exemption amounts will drop to approximately $6.8 million per individual and $13.6 million per couple—causing more people to have taxable estates.

It might seem that $16,000 annually wouldn’t transfer significant wealth to family members. However, consider a couple maximizing their gifting to their two children. Each parent can gift $16,000 to each child, a total of $64,000 from both spouses. In twenty years, the annual gifts would total $1,280,000. Assuming a 6.50% average return and an income tax rate of 35%, net of taxes, these gifts would be worth $2,345,806, thus removing over $2.3 million from their estate and representing a tax savings of over $800,000 assuming a taxable estate.

Gifting strategies should be considered as a part of your overall financial plan. Common gifting methods include:

When you gift stock, it is important to remember that the recipient (donee) receives your original cost basis. For example, if someone gifted $10,000 of stock with a cost basis of $5,000, and the donee immediately sold the stock, they would realize a $5,000 capital gain. This effectively shifts the taxable gain and any future appreciation to the donee.

Often people choose not to donate low basis stock in favor of letting family members inherit the stock with a stepped up basis. Under current law, the inheritor’s basis becomes the value as of the donor’s date of death. In our example above, if the loved one inherited the stock (versus receiving it as a gift) and immediately sold the stock for $10,000, there would be no taxable event.

Keep in mind, there are still circumstances where donors may choose to gift appreciated stock:

It is not beneficial to gift depreciated stock. If the original purchaser sells a stock that has lost value, he or she now has a realized loss that can offset gains. If they gift that same stock with a loss, due to carry over basis rules, the loss evaporates and neither party benefits from the loss.

Another opportunity in this challenging market environment is that you may be able to gift more shares today, due to the lower values, than you could have at the beginning of the year. If the recipient plans to hold the stock long term, it’s a great opportunity for appreciation due to possible future gains.

Turbulent economic conditions create a heightened need for donations for many charities to continue meeting the needs of the communities they serve. Interestingly, donors often increase their charitable giving during difficult times. According to Fidelity Charitable, charitable giving in 2020, the first year of the pandemic, was a record setting $471 billion, a 5% increase over 2019.

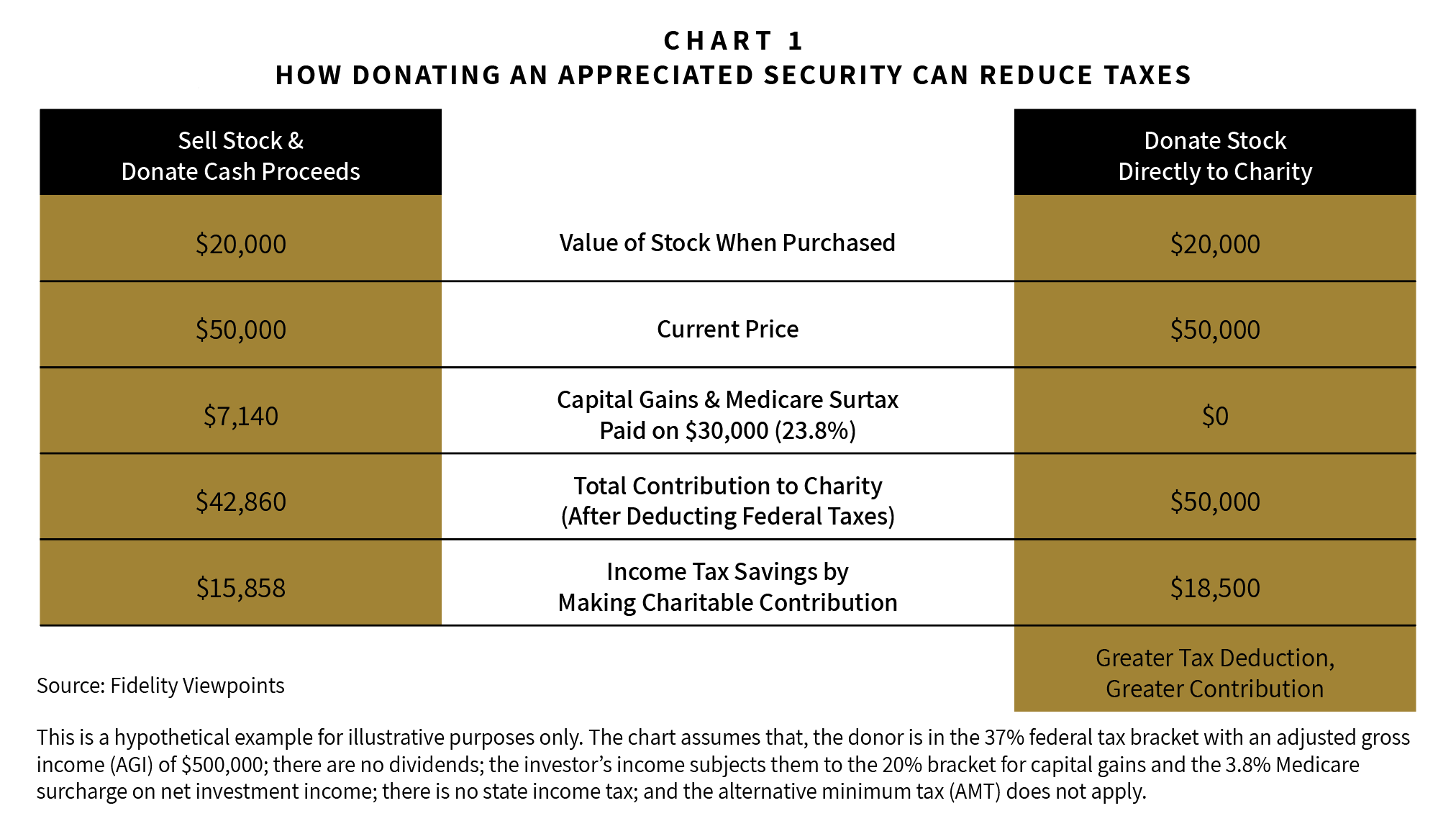

Charitable donations can have tax benefits. If you itemize, in 2022 you can receive a deduction for cash donations to a public charity of up to 60% of your AGI (Adjusted Gross Income) or up to 30% of your AGI for donations of stock to a public charity, provided the assets have been held for more than one year. While you receive a larger deduction (60% of AGI) for cash, financial professionals usually recommend donating appreciated stock versus cash. Why is that?

The chart below highlights the tax savings of donating an appreciated stock directly to a charity versus selling the stock and gifting the cash proceeds.

Considerations when donating appreciated stock:

Common methods for donating stock to a charity:

For most charities, both small and large, it is much easier to receive donations from either a DAF or via a QCD since the donation is in the form of cash. If a stock is donated directly to a charity, it necessitates that the charity has a brokerage account with which to receive and then sell the stock. This can create an unnecessary expenditure of valuable time and resources.

As we gather to give thanks, it is an opportune time to revisit tax efficient strategies that can benefit our communities and our loved ones. Volatile markets call for special consideration, but they need not derail your giving plan. Before implementing any of these strategies, please consult your wealth advisor to ensure that they are consistent with your individual situation and wealth plan.

DISCLAIMER: The information provided in this material should not be considered as a recommendation to buy, sell, or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER INVESTMENT MANAGEMENT: With over 50 years of experience and more than $2 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.