Chief Investment Officer | Principal

For much of the past 15 years, low bond yields have helped push up stock prices as investors found few alternatives to stocks in attempting to reach their return objectives.

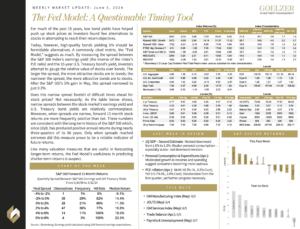

Today, however, high-quality bonds yielding 5% should be formidable alternatives. A commonly cited metric, the “Fed Model,” suggests as much. By measuring the spread between the S&P 500 Index’s earnings yield (the inverse of the index’s P/E ratio) and the 10-year U.S. Treasury bond’s yield, investors attempt to gauge the relative value of stocks over bonds. The larger the spread, the more attractive stocks are to bonds; the narrower the spread, the more attractive bonds are to stocks. After the S&P 500’s 5% gain in May, this spread narrowed to just 0.3%.

Does this narrow spread foretell of difficult times ahead for stock prices? Not necessarily. As the table below shows, narrow spreads between the stock market’s earnings yield and U.S. Treasury bond yields are relatively commonplace. Moreover, when spreads are narrow, forward 12-month stock returns are more frequently positive than not. These numbers are consistent with the long-term history of the S&P 500 which, since 1928, has produced positive annual returns during nearly three-quarters of its 96 years. Only when spreads reached extremes did this measure prove to be a reliable indicator of future returns.

Like many valuation measures that are useful in forecasting longer-term returns, the Fed Model’s usefulness in predicting shorter-term returns is suspect.

Weekly Market Update: June 6, 2024