Chief Investment Officer | Principal

For all but a few prognosticators, 2023 was a humbling one. As we mentioned in last quarter’s Insights, most economists entered 2023 predicting a recession. And stock market forecasters were equally cautious in 2023: the average year-end price-level prediction for the S&P 500 Index was 4009, which would have made for a mediocre 4.4% calendar year return.1

Neither prediction proved true. Quite the opposite, in fact: economic growth was positive throughout 2023, with the U.S. economy growing at an average rate of nearly 3%. And at 4,770, the S&P 500 produced an impressive 26% total return, although returns for many other stock market indexes were far more modest.2

The year that began with pessimism and caution proved to be rewarding for most investors and humbling for most prognosticators.

Forecasters’ struggles in 2023 speak to the challenge of predicting short-term market changes. In this annual “look ahead” at the markets, we will not offer short-term predictions on stock and bond markets. Rather, we offer 10-year return forecasts generated from models that we have used and refined over many years.

For stocks, these models incorporate 20 years of market data and project forward trends in corporate earnings and dividends for the next 10 years. We then apply an estimate of equilibrium valuations to arrive at total return forecasts. Our fixed income models also incorporate equilibrium valuations, yet account for the many different paths interest rates are likely to take over the forecast period.

Although not shown here, our evolving forecasts for private assets—including private equity, private credit, and private real estate—require consideration of several factors unique to private assets. Those factors include pricing relative to publicly traded assets and the expected additional return that investors will require for making long-term capital commitments.

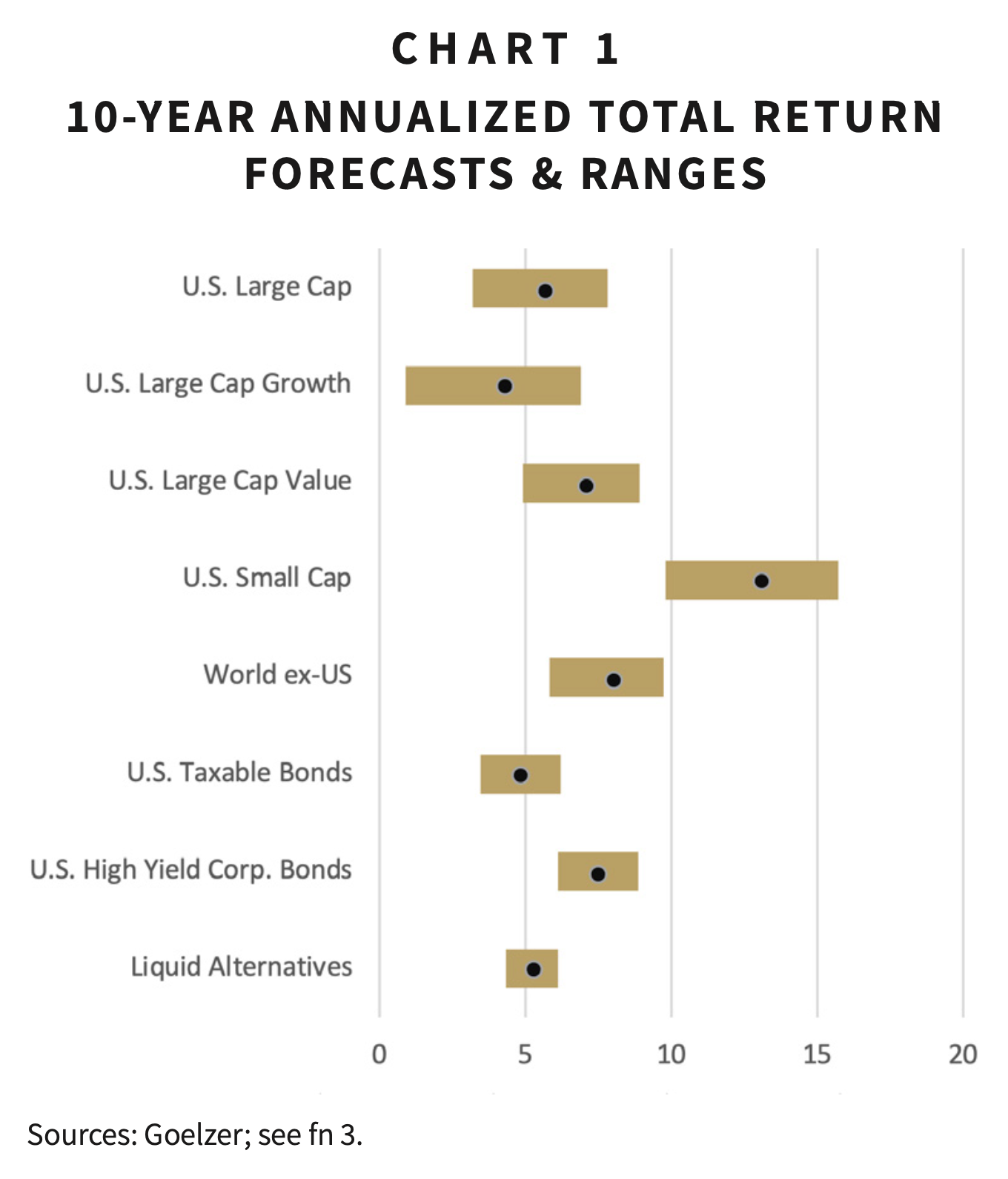

Chart 1 shows our 10-year forecasts for different classes of publicly traded stocks, bonds, and alternative assets.3

Compared to one year ago, our 10-year outlook for stocks is mixed, with return forecasts reduced for some segments and increased for others. Specifically, our outlook for U.S. large-cap and large-cap growth stocks, which rose sharply in 2023, is reduced. At the same time, our outlook for a broader spectrum of stocks, particularly those of smaller companies, has improved.

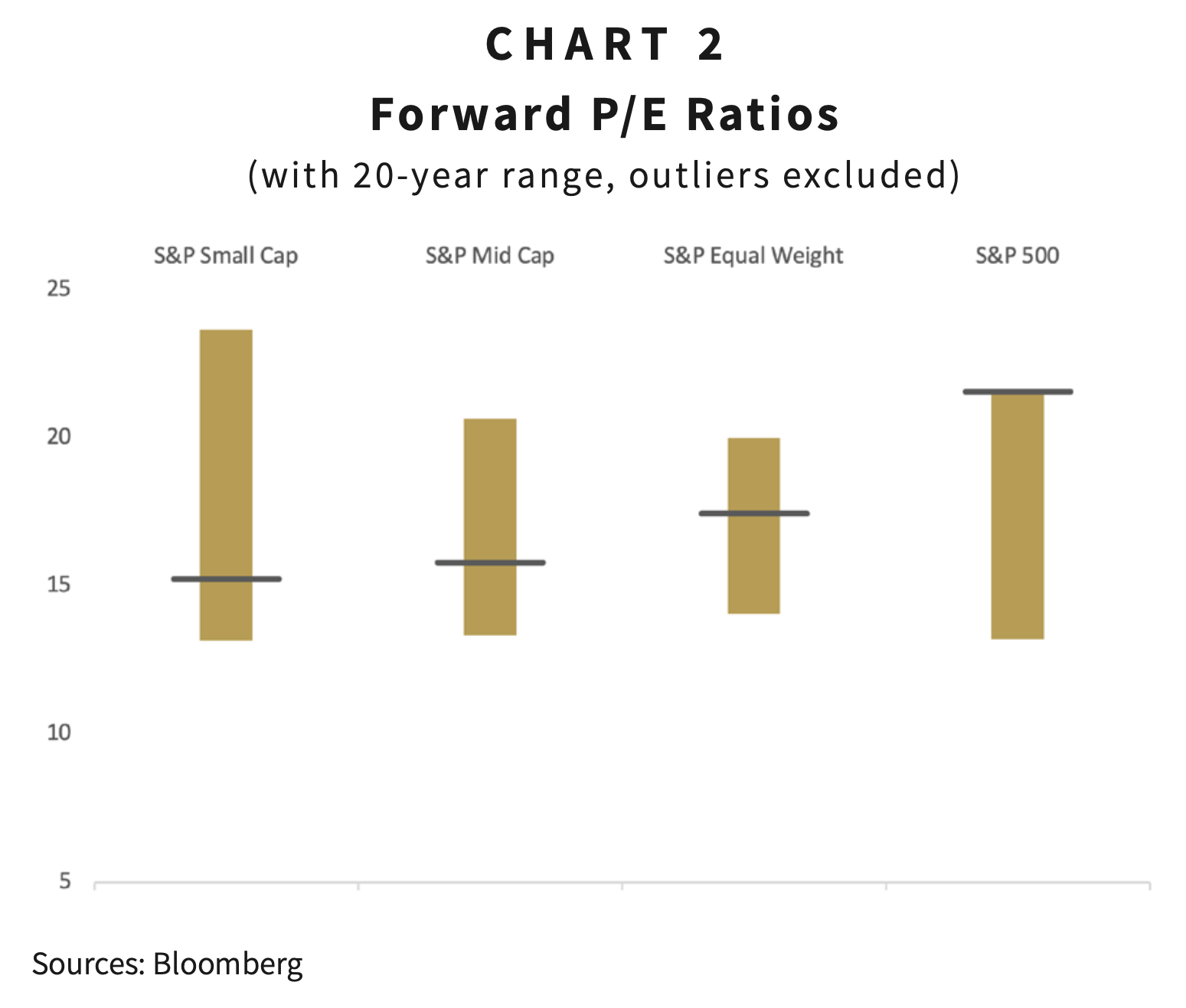

The dimmer outlook for growth stocks results from the strong performance of a small number of mega-cap stocks and their contribution to the S&P 500’s 2023 returns. The so-called “Magnificent Seven” companies produced a total return of 107% and accounted for over 1/2 of the S&P 500’s 2023 price return.4 As a result of this remarkable performance, the S&P 500 ended the year trading near its all-time high and at a historically expensive price-to-earnings ratio of 22. Such strong performance among this cohort of stocks reduces their future return potential, which is reflected in our revised 10-year return assumptions.

Fortunately, this picture is quite different when assessed from other perspectives. While the S&P 500 may indicate that stocks have fully recovered from a punishing 2022, other measures of the stock market show that the recovery is incomplete. The S&P 500 Equal Weight Index which, by weighting each member of the index equally, neutralizes the price impact of the “Magnificent Seven,” trades below its high-water mark from 2021. The same is true of other stock market indexes: U.S. small and mid-cap indexes and international equity indexes have yet to recover from their previous highs. As a result, the indexes that in 2023 trailed the S&P 500 and its “Magnificent Seven” are priced at more attractive levels, as Chart 2 shows.5

These more attractively priced areas of the stock market show better return potential according to our 10-year forecasts.

We should also note that expected returns from U.S. bonds have improved significantly over the past two years due to higher yields. After years of exceptionally low bond yields and low expected returns, investors can now capture higher starting yields and therefore higher expected returns. Equally important, higher starting yields decrease the likelihood of negative bond returns should interest rates rise, further adding to the rediscovered appeal of bonds. Outside of public markets, we see opportunities for improved returns and enhanced diversification in private assets.

We offer these updated 10-year forecasts with full awareness that, over the short term, markets will move in different directions that our forecasts indicate. Over the next year, for example, investors will grapple with many variables as they determine the prices to pay for stocks, bonds, and other financial assets. The direction of inflation, the path of interest rates, the durability of corporate earnings, ongoing wars in Eastern Europe and the Middle East—these are only a few variables that investors will weigh. Markets will shift accordingly as these variables change. For most, attempting to predict with precision how these variables will shift over a short time horizon will prove once again to be a humbling exercise.

Using history as our guide, we instead offer these longer-term forecasts to aid in asset-allocation decisions. We also offer one important reminder: all forecasts are based on a single end point and do not account for the probability of temporary market declines over the 10-year horizon. Such moments offer the possibility for better 10-year returns to those who invest new cash or rebalance their portfolios appropriately. Investors with strategic plans in place in advance of these temporary declines will be best positioned to reap the potential rewards.

1 Lu Wang. “Burned Stock Pundits Ditch Two Decades of Unbroken Bullishness.” Bloomberg. December 1, 2022.

2 Bloomberg. GDP grew at an annual quarterly rate of 2.2%, 2.1%, and 4.9% over the first three quarters of 2023. As of December 22, 2023, the Atlanta Fed GDP Now Forecast estimates 4Q GDP growth of 2.3%. S&P 500 Index returns include dividends reinvested into the index.

3 Indexes used include the following: S&P 500, Russell 1000 Growth, Russell 1000 Value, S&P Mid Cap, S&P Small Cap, MSCI ACWI ex-US, Bloomberg U.S. Aggregate Bond, Bloomberg U.S. Corporate High Yield, Credit Suisse Liquid Alternatives. Forecasts as of December 1, 2023.

4 The “Magnificent Seven” includes Nvidia, Microsoft, Apple, Google, Meta (Facebook), Tesla, and Amazon. Price returns from The Bloomberg Magnificent 7 Total Return Index (BM7T) and the S&P 500 Index (SPX).

5 Bloomberg, as of December 29, 2023. Top 10% and bottom 10% of observations excluded.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.