Director of Wealth Planning | Senior Wealth Advisor

Principal

The past few years have presented a chaotic landscape of new rules and regulations related to federal income taxes. The recent passing of SECURE Act 2.0 in late 2022 created more choices and complexities than ever for funding and taking distributions from retirement vehicles. Many of these choices allow for a higher level of control over your current and long-term tax situation. When faced with more choices, however, it is easy to shut down and stick with the status quo, potentially foregoing the most beneficial options for your specific situation. With proactive tax planning significant income tax savings may be possible.

For those in the accumulation phase, employer-sponsored retirement plans such as 401(k)s and 403(b)s have been funded primarily with pre-tax contributions. These are known as traditional plans. With traditional plans, participants benefit from both pre-tax contributions and tax-deferral while assets are held in the plan. The downside is that withdrawals from traditional plans are taxed as ordinary income. A second type of plan, known as a Roth plan, requires funding from post-tax dollars. The primary benefits of Roth plans are tax-free growth within the plan and the ability to take withdrawals on a tax-free basis.

In the past few years, employers have increasingly provided employees with the option to make post-tax contributions into Roth plans. A 2021 survey from Plan Sponsor Council of America showed that 88% of employer plans offered a Roth option.1 But according to that same survey, only 28% of employees have taken advantage of these Roth options.

With the SECURE Act 2.0, more Roth options are becoming available. And in some cases, these are not options but, in fact, requirements.

Here are a few:

With this growing shift toward Roth options, how do you decide whether to make Roth (after-tax) or traditional (pre-tax) contributions? As is often the case, it truly depends on your unique situation.

Typically, it is better to make Roth contributions if your tax bracket is currently low and expected to be higher in the future at the time of distribution. Conversely, it is typically more advantageous to make traditional contributions if your tax bracket is high now and expected to be lower in the future.

Of course, it is impossible to know the level of tax rates well into the future. For most people though, lower earnings, and therefore lower tax rates, occur early in their career, and sometimes in the early years of retirement before they are required to take withdrawals from traditional retirement plans. From a long-term tax savings standpoint, Roth contributions could be more beneficial than traditional plan contributions during these lower tax bracket years. On the other hand, those later in their career are more likely to be in higher tax brackets due to higher earnings. If that is the case, they could benefit from the current tax deduction associated with traditional plan contributions.

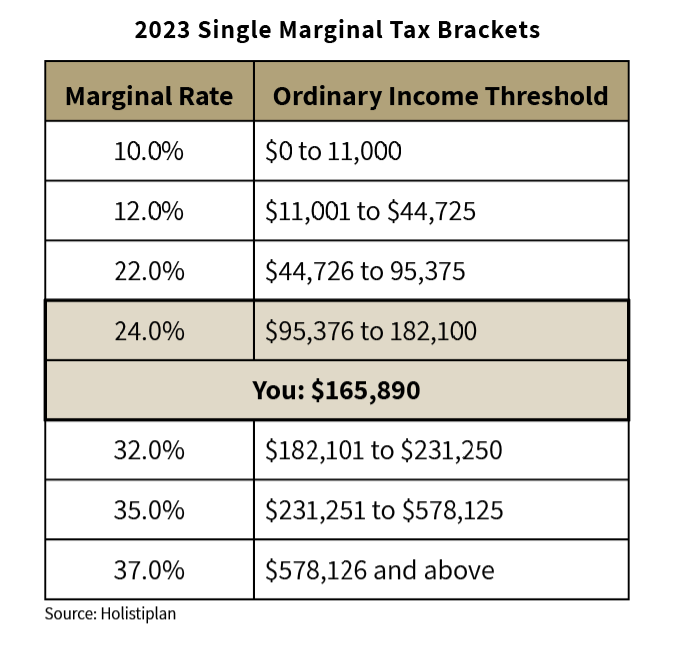

Another key piece of information that should inform these decisions is your Federal marginal tax rate. Your marginal tax rate is the amount of tax that you would pay on the next dollar of income. Under current tax law, there are seven different marginal tax brackets. A common misunderstanding of our tax system is that when your income crosses into the next marginal bracket, all your income is taxable at that rate, but that is not true. Income up to each threshold is taxed at that specific bracket.

To provide greater clarity, let’s look at an example. As shown in the following table, the marginal tax bracket for an individual filer with income of $165,890 in 2023 is 24%, but not all their income is taxed at that rate. Amounts under $95,376 are taxed at the lower rates shown. Further, they could earn up to $182,100 without being subject to a higher tax bracket.

Knowing your tax bracket helps you understand how contributions to a Roth or traditional plan will affect your tax situation. If in the example above the individual was contributing to a Roth 401(k) but receiving pre-tax employer contributions totaling $15,000, they could potentially change their employer contribution to Roth and pay tax on the employer match while maintaining a top marginal tax bracket of 24%.

While SECURE Act 2.0 brought more flexibility for creating and building an after-tax retirement bucket in the form of Roth accounts in the accumulation phase, both SECURE Act 2.0, and the original SECURE Act, created provisions that both added flexibility and limited options (forced decisions) for those in the distribution phase.

These include:

1. Later Ages for Required Minimum Distributions (RMDs)

2. Qualified Charitable Distributions (QCDs)

3. Inherited IRAs for Non-spouse Beneficiaries

Just as the addition of Roth provisions creates opportunities to improve tax planning in the accumulation phase, these changes also prompt planning choices in the distribution phase.

The delayed RMD ages create opportunities for Roth conversions in potentially lower earning years immediately following retirement. By realizing taxes at a potentially lower tax rate before the required beginning date for RMDs, you may be able to prevent your RMDs from pushing you back into higher tax brackets. This strategy is especially useful for those with taxable assets (investment accounts, savings, etc.) outside of their traditional retirement accounts to draw from living expenses and paying taxes on the conversion.

With QCDs still available as early as 70 ½, you could consider sourcing charitable funds from IRAs, rather than low basis stock held outside IRAs. This could reduce the balance of large IRAs, potentially reducing RMDs and the resulting tax rate.

For those receiving inherited IRAs, consider both current and future tax brackets to determine the most tax efficient distribution plan. The range of options include even distributions over a 10-year period to delaying distributions until potentially lower tax bracket years.

Understanding your tax bracket in the distribution phase provides clarity on the actions to take in specific years, allowing you to realize income in lower tax years and defer income in higher tax years. While realizing income in a lower tax year can be advantageous, the marginal tax bracket is not the only number to watch. One must be aware of phaseouts for credits and deductions (if applicable), additional taxes that may come into play at certain income levels (such as the Net Investment Income Tax), and, for those at or approaching Medicare age, income related adjustments to Medicare Part B and D premiums that take effect even if you surpass the income thresholds by $1.

For many, the topic of taxes may be fraught with feelings of anxiety and frustration. The rapid changes to tax regulations over the past few years have added turmoil and mayhem to the tax landscape. When there is chaos, it may seem like we lack control or the ability to make choices when in fact there are many opportunities to make choices in your current and future tax years due to the recent changes. While these choices do necessitate careful and thoughtful tax planning, they also afford you the opportunity to minimize your taxes now and in the future.

Where do you go from here? Reach out to your Goelzer advisor to have a conversation about how tax planning might be beneficial for you.

1 “88% of employers offer a Roth 401(k),” Greg Iacurci, CNBC, https://www.cnbc.com/2022/12/16/88percent-of-employers-offer-a-roth-401k-how-to-take-advantage.html, December 16, 2022.

DISCLAIMER: This report includes candid statements and observations regarding financial planning strategies; however, there is no guarantee that these statements will prove to be correct. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Past performance is not a guarantee of future results.