Senior Partner | Principal

I am often asked, “When will things return to normal?” Despite their daily routines returning to normal, investors continue to feel the aftershocks of the Covid-19 pandemic in the economy and financial markets. For example, bond yields, which initially fell to record lows, recently rose to the highest levels in 15 years, only to suddenly fall again.1 The stock market has experienced two bear markets, yet it is higher than at the start of the pandemic. And the economy currently combines fears of recession with historically low unemployment.

Financial markets, of course, reflect the economy. And while the economy is not yet normal, it is on a path back to normal. What is normal? For the economy, we define it as following longer-term trends. So to get a sense of where the economy is relative to normal, let’s take a look at three distinct measures: money supply, retail sales, and employment.

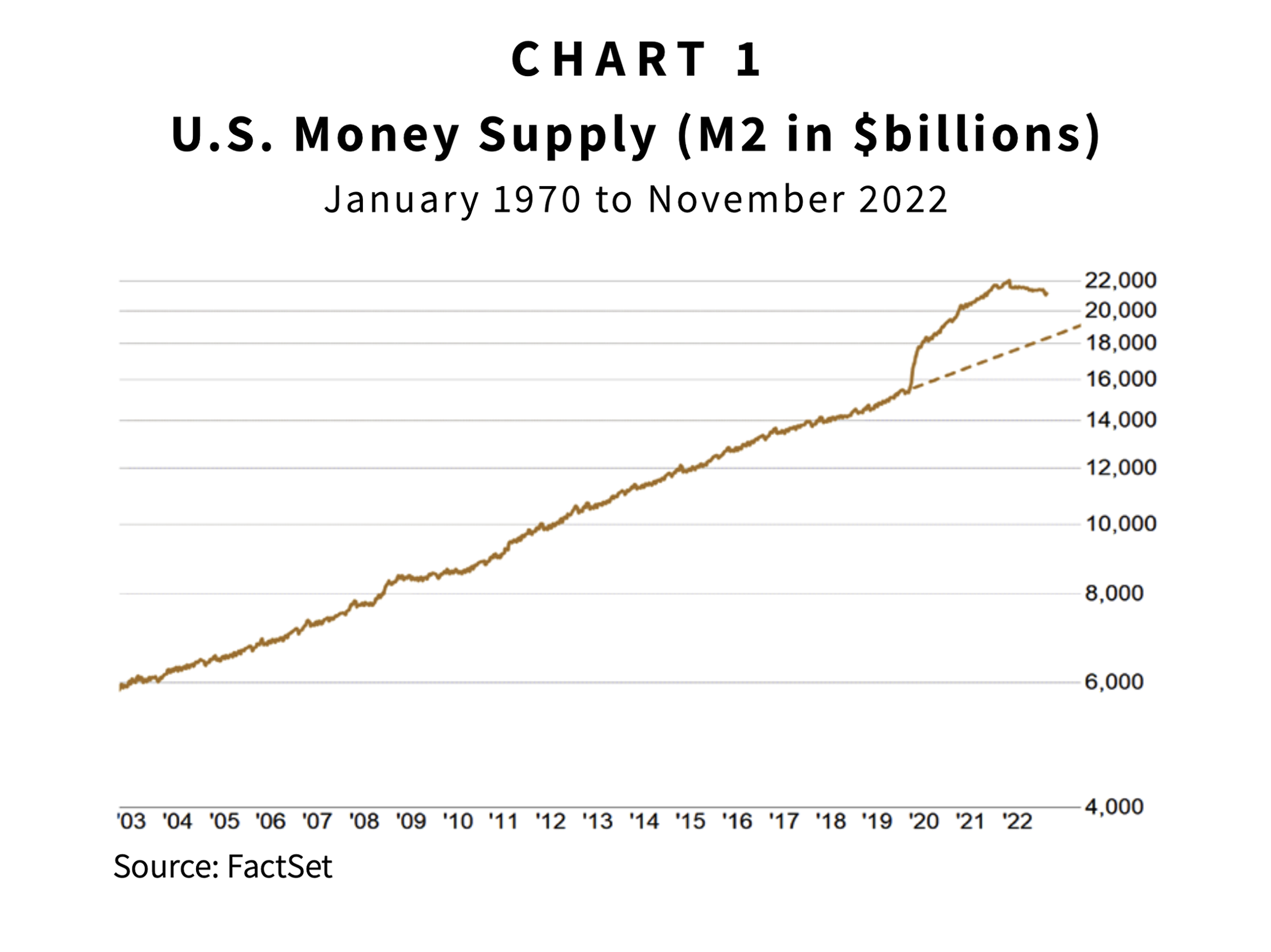

As shown on Chart 1, money supply soared during 2020 and 2021 as the Federal Reserve funded Congress’ massive stimulus programs. The annualized growth rate for money supply during those two years was 18.4% versus 6.1% during the prior 10 years.2 In simple terms, money supply should grow at a rate equal to real economic growth plus inflation. So it’s no surprise that the surge in money supply led to soaring inflation.

But in 2022, something happened that had not occurred in over 70 years: money supply fell. Why? Because reducing money supply is one of the Federal Reserve’s tools for lowering inflation. However, despite the recent drop, money supply remains well above where it would be had the longer-term trend persisted, as shown by the chart’s dotted line.

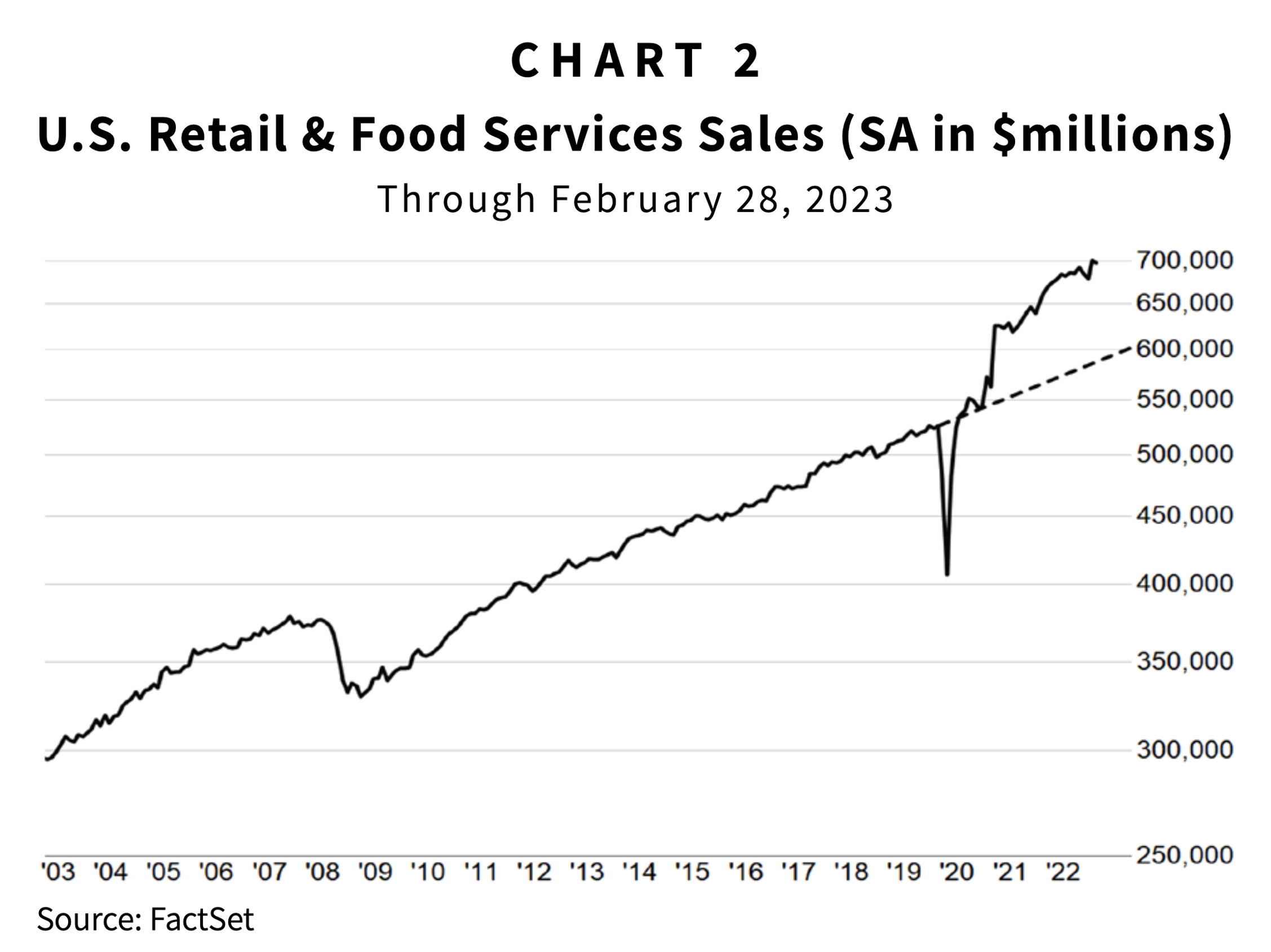

Retail sales initially plunged at the start of the pandemic as businesses labeled non-essential, including stores and restaurants, were required to close. Once those businesses reopened, consumers, flush with government-stimulus cash, went on a spending spree. Chart 2 reflects the surge in retail sales that began in 2020. During that year, spending was abnormally tilted toward the purchase of goods as many people avoided travel and dining in restaurants for fear of Covid. That changed in 2021, causing a surge in spending on services.

Then inflation kicked in. Retail sales, as shown on the chart, include price increases. So while the quantity of goods and services sold in 2022 was lower than in 2021, higher prices caused the total amount spent to remain abnormally high compared to the longer-term trend. Getting back to that trend in the near future requires a drop in retail sales large enough to offset the recent effects of both stimulus programs and price increases. Such a drop in sales, unfortunately, would likely be the result of a painful economic recession. Another possibility, however, is that retail sales growth reverts back to its pre-pandemic trend but does so from today’s higher starting point.

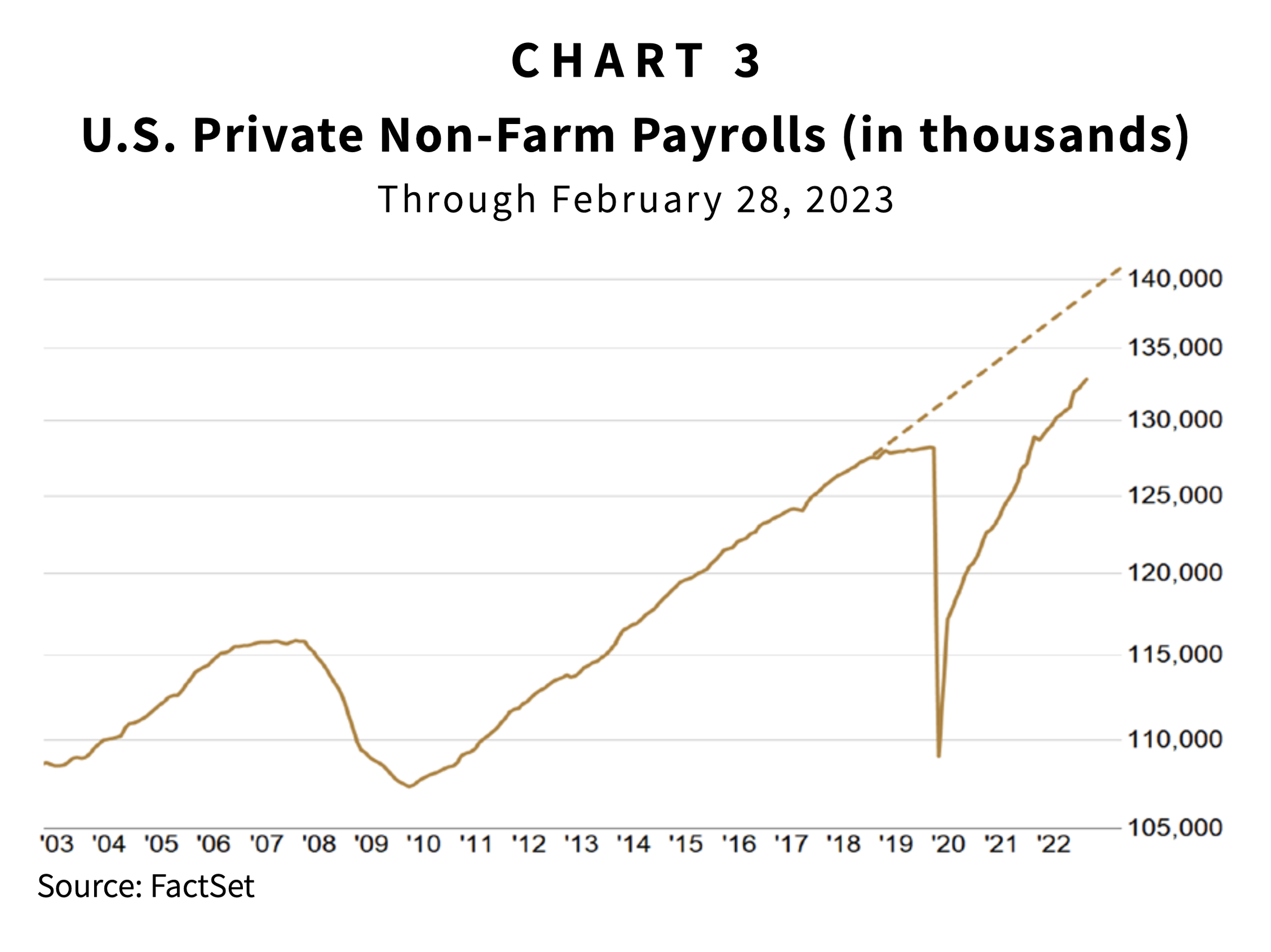

The current unemployment rate of 3.6% gives the impression that the job market is fully recovered. However, a closer look paints a different picture. The number of people employed in the U.S., outside of government, plunged at the start of the pandemic. After a partial snap-back following the end of most lockdowns, employment grew at a faster-than-normal rate, reaching pre-pandemic levels in 2022. However, at the current level, the number of private sector U.S. workers remains more than five million below where it would be if the pre-pandemic job trend had continued, as shown by the dotted line on Chart 3.

The trends that existed before the pandemic existed for a reason. Economic growth tracks a combination of population and productivity growth, which tend to be steady over time. Therefore, it is reasonable to expect that our economy will eventually return to those trends. However, just as the pandemic caused a bumpy path away from the longer-term trends, it will likely be a bumpy path back to those trends. And, unfortunately, some of the bumps may be quite jarring. A recent example of this is the banking industry’s troubles exposed by the Federal Reserve’s rapid interest-rate increases.3

Investors should expect the bumpy path to normal will continue to produce above average volatility in the stock, bond, real estate, and commodity markets. The protection against this volatility, as always, is to maintain proper diversification along with sufficient liquidity for your upcoming spending needs. Following these tried-and-true rules should put you in a good place to benefit from the eventual return to normal.

1 10-year U.S. Treasury bond yield

2 Federal Reserve Bank of St. Louis (FRED)

3 For more about the recent banking industry troubles, see our March Insights titled, “Thoughts on the Fallout from Silicon Valley Bank,” https://goelzerinc.com/insights_post/thoughts-on-the-fallout-from-silicon-valley-bank/.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $2.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.