Senior Partner | Principal

In our April 2021 edition of Insights, I wrote that inflation would become the new worry for investors. With the consumer price index above 8% the past three months, that statement now seems…well, understated. But now that inflation has the Federal Reserve’s full attention, a new change is taking place: the value of money is rising.

The recent wave of inflation is the result of the government’s efforts to reflate an economy that was partially closed by pandemic lockdowns. To reverse the initial deflation caused by lockdowns and to avoid a prolonged recession, the Federal Reserve cheapened the value of money via a zero-interest-rate policy and a rapid increase in money supply. Meanwhile, Congress distributed that newly created money into the economy through numerous stimulus programs. But the sharp rise in inflation shows that that the scale of those programs was excessive, especially when paired with shortages of goods, services, and workers. Together, this resulted in numerous mismatches between supply and demand and, therefore, a sharp rise in inflation.

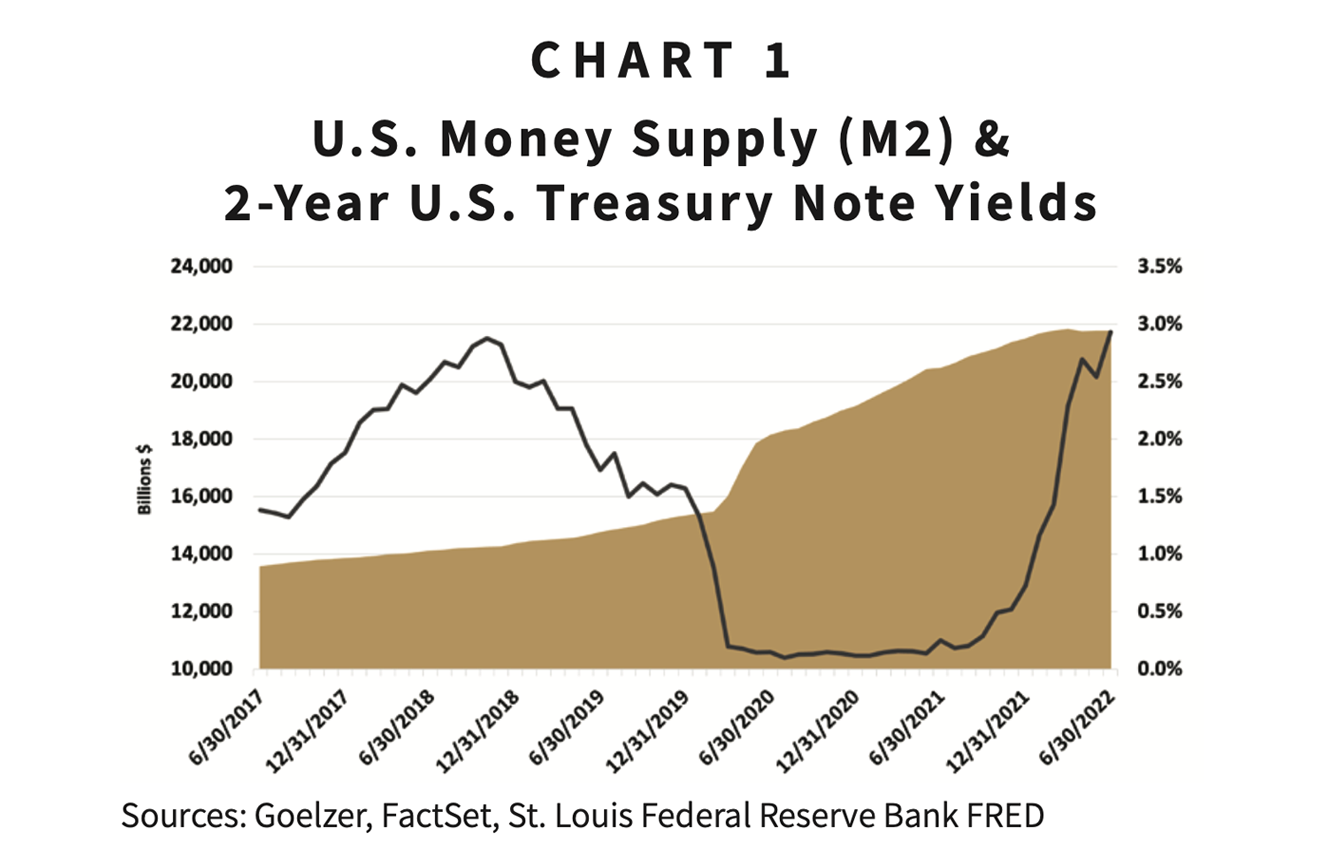

To tame inflation, the Federal Reserve is reversing those prior policies. Evidence of this policy reversal can be seen on Chart 1, which shows that U.S. money supply has stopped growing and the 2-year U.S. Treasury bond’s yield, which leads changes in the federal funds rate, has been rising. These changes reflect the Federal Reserve’s efforts to raise the value of money, thereby taming price increases for goods and services.

In basic terms, the value, or price, of money is the interest rate paid on it. One example of the rising value of money is the 30-year mortgage rate. Just prior to the start of the pandemic, the national-average interest rate for a 30-year fixed-rate mortgage was 3.72%. As an example, at that rate the monthly principal and interest payment was $1,384 on a $300,000 mortgage. By early 2021, the national-average mortgage rate had fallen to 2.65%. That lower interest rate enabled home buyers to get a larger $344,000 mortgage with the same monthly payment, allowing them to pay more for a home. Therefore, the lower value of money, in this case reflected by a lower borrowing cost, helped fuel the sharp rise in home prices.

This year, however, the value of money has risen. The average interest rate on a 30-year mortgage is now 5.70%. To match the same monthly payment, home buyers would need to limit their mortgage to $239,000, a drop of 31% from the low point for mortgage rates in 2021. As a result, we should see an end to the rapid inflation in home prices.

Another way to measure the value of money is to look at how much it costs to obtain it. We don’t normally think about the cost of money in the way that we think about the cost of items like food or gasoline. For those items, we think in terms of how many dollars it costs to buy something. But inversely, we can think of the value of money in terms of how much of something it cost to buy one dollar. When looked at that way, we see that the cost of a dollar has gone up 8% this year when measured in Euros, 14% when priced in 10-year U.S. Treasury bonds, and 25% when measured in units of the S&P 500 Index.1 In other words, by declining in value, financial assets are already responding to the Federal Reserve’s efforts to raise the value of money.

At this point you may be thinking this pivot in Federal Reserve policy is not good. The value of money going up has caused the value of financial assets to decline while prices for consumer goods and services continue to rise. And you are correct, at least so far.

Financial markets anticipate and react ahead of the implementation of Federal Reserve policy changes. The real economy, however, responds with a delay to those changes. It was only in February that the Federal Reserve stopped growing money supply by increasing its balance sheet; and only in June did the Federal Reserve begin to reduce its balance sheet. Additionally, the federal funds rate has been increased by just 1½ percentage points so far from a near-zero starting point. Financial markets already reflect the effect of those adjustments as well as the consensus expectation for additional changes. The effect of these changes on prices for goods and services is just beginning.

The key questions for investors going forward are: “How soon and by how much will inflation fall?” The sooner the inflation rate falls, the sooner financial markets will respond positively. Sustained high inflation, however, risks greater actions by the Federal Reserve that would raise the risk of recession and add to the stock market’s challenges.

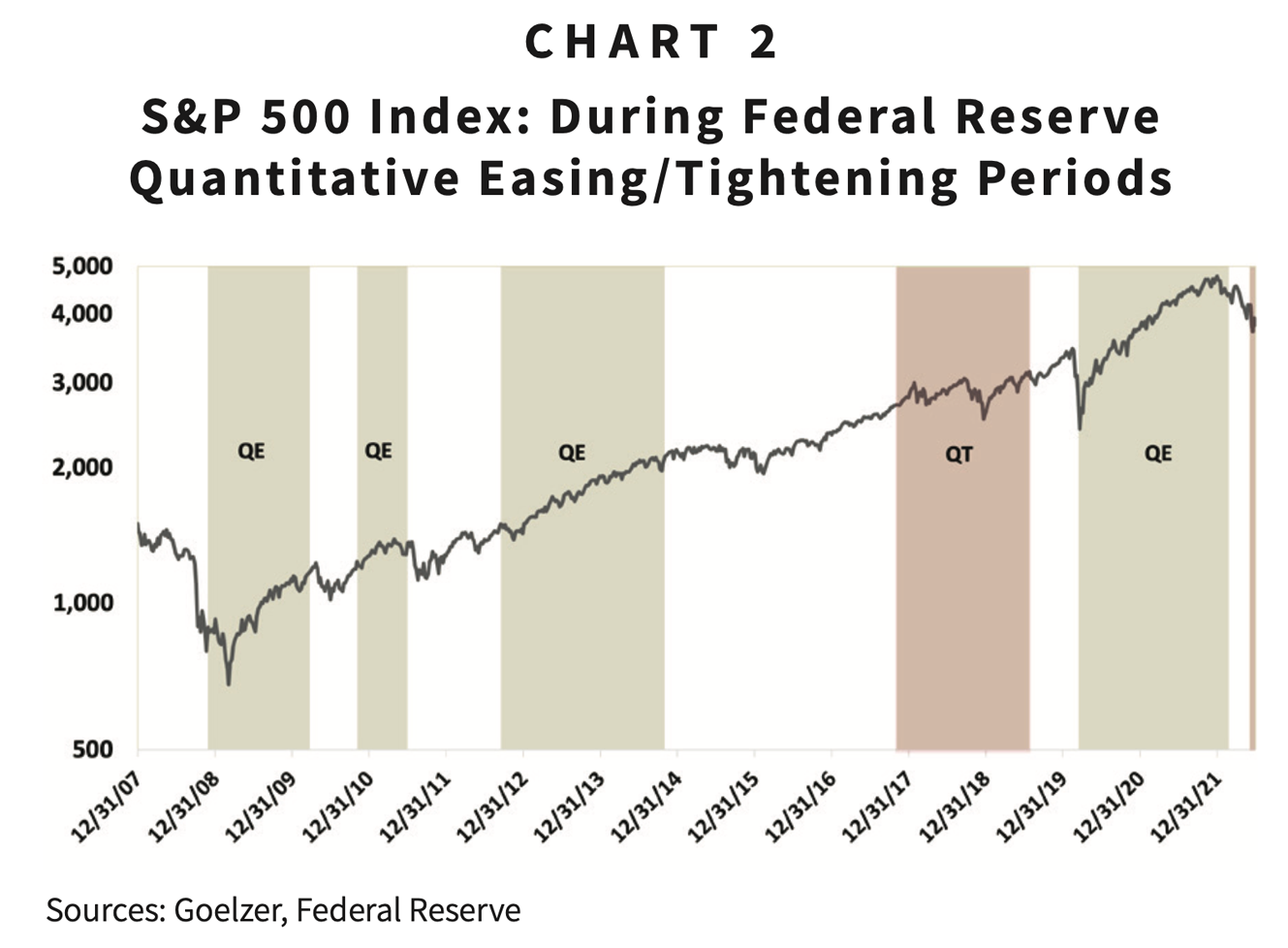

Chart 2 shows the price of the S&P 500 Index during the four quantitative easing (QE) periods and one quantitative tightening (QT) period since the beginning of 2008. Quantitative easing is a Federal Reserve program designed to stimulate the economy by injecting new money via bond purchases. Quantitative tightening is the opposite. As shown, the stock market responded positively during periods of quantitative easing but struggled to gain ground between those periods. The stock market also struggled during the one quantitative tightening period, rising higher once it was ended but then falling at the start of the pandemic.

Stock market investors have limited experience with quantitative easing and tightening. Prior to 2008, quantitative easing had not been used by the Federal Reserve since the 1930s. Therefore, we should be cautious in making forecasts based on its limited history. Recent experience, however, shows that investors have become conditioned to obeying the mantra, “Don’t fight the Fed.” With the Federal Reserve just beginning a tightening program, a sustained rally that pushes stock indexes to new highs seems unlikely until market participants sense that an end to the program is within sight. While many will view that forecast negatively, opportunists will see it as providing more time to invest ahead of the next major market advance.

1 As of June 30, 2022

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $2.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.