Chief Investment Officer | Principal

In the mid-2000s, author Daniel H. Wilson published “Where’s My Jetpack?,” a book for frustrated futurists in search of techno wonders promised long ago. Somewhat like Wilson, investors have spent the first nine months of 2023 searching for something that has yet to arrive, namely the most-predicted economic recession in the history of predicting recessions. Indeed, as the annus horribilis unfolded in both the stock and bond markets in 2022—a year in which a portfolio of 60% stocks and 40% bonds fell over 15%—investors became increasingly confident that the U.S. economy was close to entering recession.1

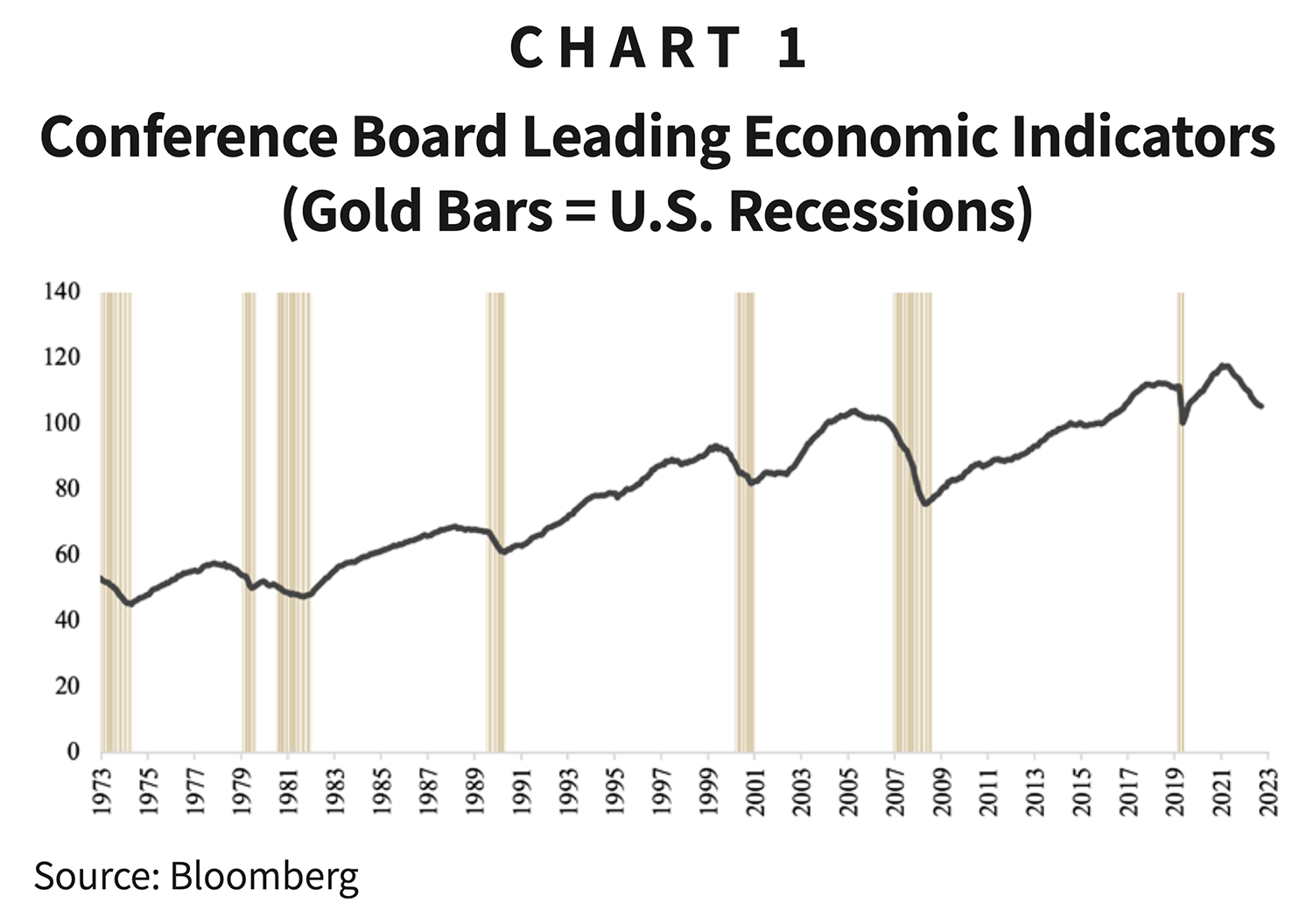

Not only did investors feel this way, but also many closely watched economic signals began to signal trouble ahead. One carefully watched series of signals, the Conference Board’s Leading Economic Indicators, began trending downward last summer, as shown in Chart 1.

With other indicators flashing red—such as a deeply inverted yield curve and the New York Federal Reserve’s Probability of Recession Indicator—most economic forecasters considered a 2023 recession a sure thing.2

Fears of recession were well founded. Entering the year, headline inflation was running over 7.0% on a year-over-year basis while the unemployment rate was near its historical low at 3.6%.3 A strong labor market, as evidenced by this historically low unemployment rate, had put the Federal Reserve in favorable position to continue raising interest rates in its attempt to lower inflation toward its 2% target.

Investors thus expected the Federal Reserve to continue raising interest rates into 2023, even after last year’s rapid pace of interest rate increases—the most aggressive pace of interest-rate increases in over 40 years. Because the effects of higher interest rates are thought to work with a delay, investors anticipated the effects of 2022’s rate increases to begin slowing economic activity in 2023. In addition to the constraining effects of higher interest rates, forecasters pointed to dwindling consumer savings and rising geopolitical risks as rationale for their pessimistic projections.4

Despite this gloomy backdrop, the U.S. economy has proven resilient through the nine months of 2023. Real, i.e., inflation-adjusted, gross domestic product grew at an annual rate of over 2% in the first half of the year; and projections for third-quarter growth, as measured by the Atlanta Fed’s GDP Now model, estimate a further acceleration in growth to 4.9%.5 How could the forecasters be so wrong? Two explanations stand out: 1) strong consumer spending, supported by a tight job market and growing incomes and 2) a burst of deficit-funded fiscal stimulus that has helped fuel business and residential investment.

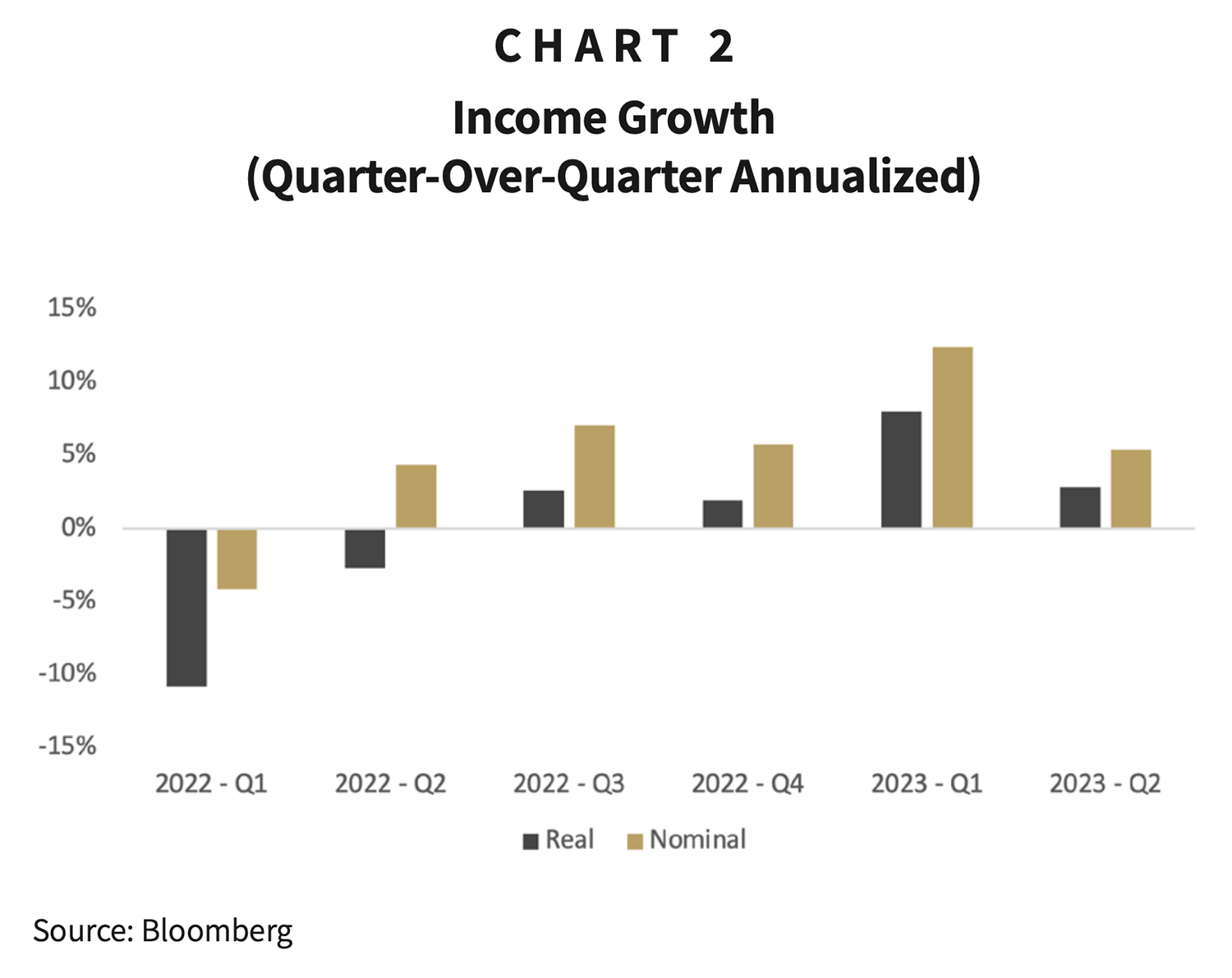

Through July of this year, consumer spending increased at an average pace of 6.7% on a year-over-year basis. Even adjusted for inflation, consumer spending increased at an average of 2.4% on a year-over-basis, indicating growing consumer appetite for goods and services and not simply absorption of price increases. Consumers have been especially keen to spend on services such as air travel, with inflation-adjusted purchases of airline services up an average of 9.7%.6 The Federal Reserve’s interest-rate increases—and concomitant increases in consumer borrowing costs—have not yet dampened consumer spending. Underpinning this spending impulse is strong growth in consumer income, evidenced by growth in disposable income over the first half of the year. See Chart 2.

While forecasters may have been correct to worry about dwindling savings, consumers have found money to spend through growing incomes and increased borrowing.

In addition to strong consumer spending, an underappreciated jolt of government stimulus has coursed through the U.S. economy year-to-date. Estimated at approximately $500 billion, the government’s fiscal stimulus has come in the form of $200 billion from the employee retention credit, with the balance coming from the CHIPS Act and the Inflation Reduction Act.7 The latter programs, by offering tax credits and subsidies to support investments in renewable energy and in U.S. semiconductor manufacturing, have stimulated business investment, an area of the economy that was slowing in late 2022.

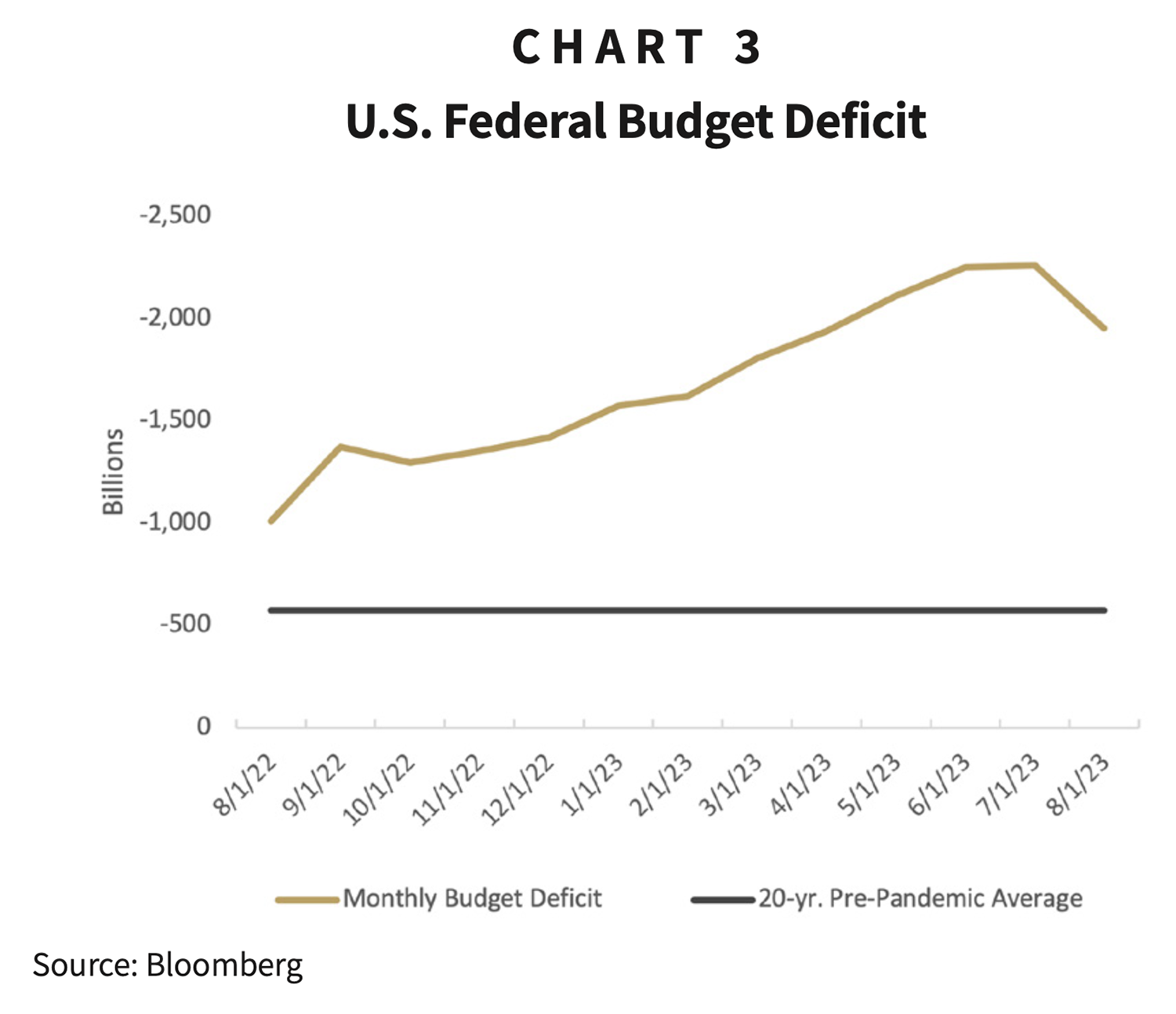

While, in theory, the constricting effects of higher rates should slow business and residential investment, these stimulus programs have encouraged it. Fixed business investment contributed to nearly half of the second quarter’s 2.1% growth in GDP. Fiscal support to encourage investment in U.S. semiconductor manufacturing supported that growth.8 The combined effect of these programs, along with reduced tax-collections year to date, are reflected in the U.S. federal budget deficit, which has nearly doubled in size from one year ago and sits well-above its pre-pandemic average. See Chart 3.

This underappreciated jolt of fiscal stimulus, shown in a ballooning government budget deficit, has effectively offset the intended effects of higher interest rates.

However incorrect forecasters may have been in their calls for a 2023 recession, the economic risks that led to those gloomy predictions are still relevant. At nearly 4%, inflation remains almost twice the level of the Federal Reserve’s target, despite having dropped meaningfully over the course of the year.9 The Federal Reserve will continue to fight inflation, perhaps by further increases in interest rates, but more likely by keeping rates high for an extended period.

And while the effects of those higher rates may not be apparent today, the effects are likely to emerge over time as businesses, consumers, and governments are forced to contend with the higher cost of money. Fighting inflation comes at the cost of economic growth, a cost which may not be paid in this year but for which a future bill may still await. Additional economic risks from the resumption of student-loan payments, rising energy prices, protracted union strikes, and the growing burden of government debt further cloud the economic outlook.

Given this backdrop, a level of caution is warranted. However, longer-term investors would do well to remember that—despite seven recessions over the past 50 years—the S&P 500 has produced annualized returns of 10.9%.10 Maintaining liquidity to meet spending needs and to buy stocks in periodic downturns will position investor portfolios for similar long-term growth. Facing rising economic risks, following a disciplined investment plan and staying invested remain an investor’s best defense.

1 Bloomberg US EQ:FI 60:40 Index, total return, calendar year 2022: -16.9%.

2 For example, a Bloomberg Economics model showed a 100% probability of recession starting in 2023. Bloomberg Intelligence. “U.S. Headed for a Fed-Induced Recession in 2H 2023.” December 28, 2022.

3 Bloomberg. Inflation as measured by the headline Consumer Price Index (November 31, 2022).

4 From December 2021 to December 2022, the personal savings rate had declined from 7.5% to 3.7%. Source: Bloomberg.

5 Bloomberg, as of September 19, 2023.

6 Bloomberg, as of July 31, 2023.

7 Chris Low et al. “Economic Weekly.” FHN Financial. September 8, 2023.

8 Anna Wong. “US REACH: Strong 2Q GDP Shows Bidenomics Working Against Fed.” Bloomberg. July 27, 2023.

9 As of August 31, 2023, headline and core inflation, as measured by the Consumer Price Index, increased on a year-over-year by 3.6% and 4.3%, respectively.

10 Bloomberg, total returns from August 31, 1973 through August 31, 2023.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.