Chief Investment Officer | Principal

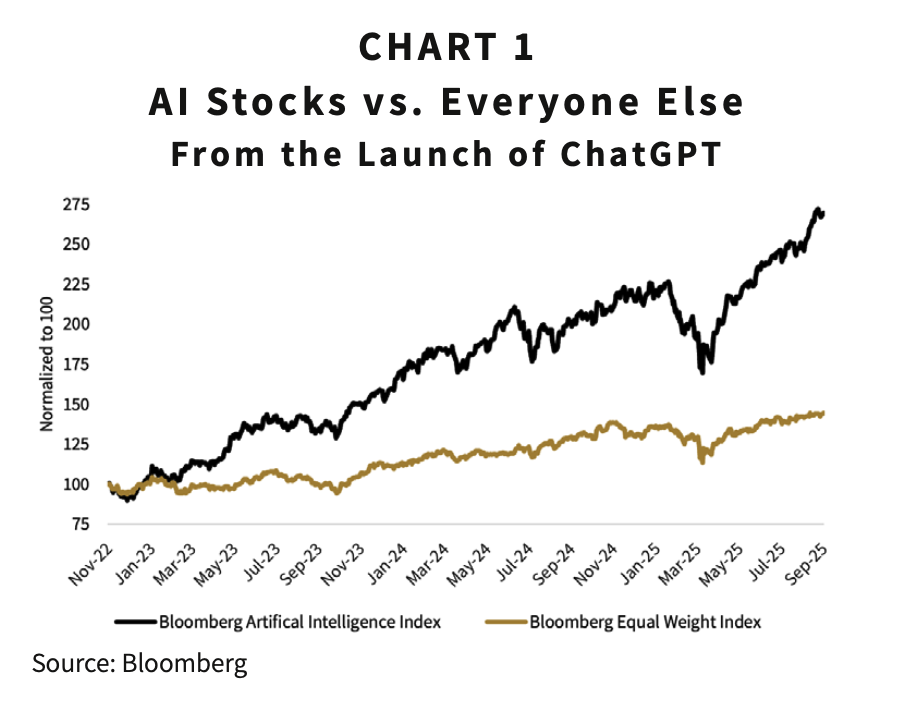

Since the launch of ChatGPT nearly three years ago, both enthusiasm and apprehension surrounding the rapid development of artificial intelligence (AI) have intensified. Rather than subsiding, this enthusiasm has continued to grow, with the stock prices of companies perceived as AI beneficiaries outperforming the broader U.S. equity market by a factor of nearly two to one.1 This surge has been so pronounced that the five largest stocks in the S&P 500 now represent nearly 30% of the index’s total market capitalization—a concentration reminiscent of previous market peaks, including that of 2000.2

Since the launch of ChatGPT nearly three years ago, both enthusiasm and apprehension surrounding the rapid development of artificial intelligence (AI) have intensified. Rather than subsiding, this enthusiasm has continued to grow, with the stock prices of companies perceived as AI beneficiaries outperforming the broader U.S. equity market by a factor of nearly two to one.1 This surge has been so pronounced that the five largest stocks in the S&P 500 now represent nearly 30% of the index’s total market capitalization—a concentration reminiscent of previous market peaks, including that of 2000.2

The swift ascent of these stocks—coupled with widespread public fascination with AI—has prompted a critical question: “Are we in an AI bubble?” In other words, has optimism about AI inflated expectations to unsustainable levels, creating a bubble poised to burst and leaving disillusioned investors to suffer? To be clear: we are not calling a top in the AI market, but rather stating that today’s conditions exhibit the hallmarks of a bubble—one that could continue to grow but, like all bubbles, that will eventually deflate or pop. The following discussion explores potential implications for investor portfolios and the broader economy. Although we lack a crystal ball, we believe the most immediate risks lie in investor portfolios, while the longer-term promise resides with economic growth.

The AI boom exhibits the defining characteristics of a speculative bubble, as outlined by Chris Watling of Longview Economics:

A compelling narrative emerges to justify elevated valuations.3

AI enthusiasm satisfies all these criteria. The post–Global Financial Crisis era of historically low interest rates provided fertile ground for aggressive investment in emerging technologies. Tight corporate credit spreads further reduced borrowing costs, encouraging firms to finance AI-related initiatives through debt. Investor optimism has propelled AI-linked equities to record highs, with valuations of AI-related stocks trading at a nearly 40% premium to a broader basket of equally weighted stocks across various industries.4 Confronted with these realities, investors often invoke persuasive narratives—such as AI’s transformative potential or the exceptional margins and cash flows of leading AI firms—to rationalize elevated prices.

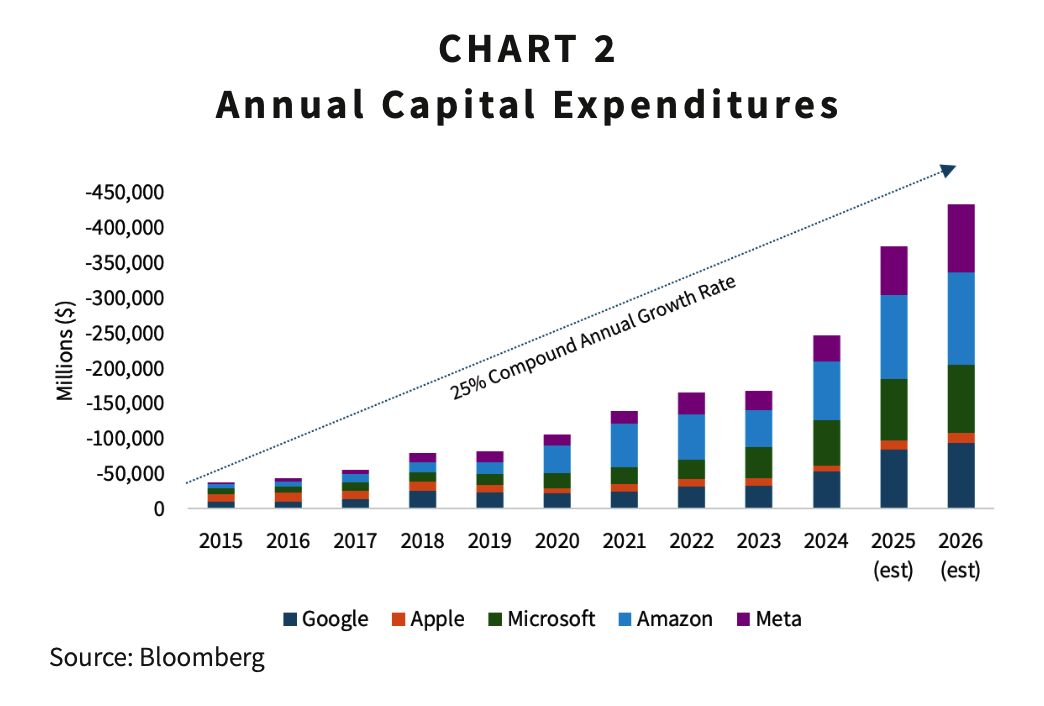

It is perhaps inevitable that a technology as revolutionary as AI would give rise to speculative excess. History suggests that investors frequently overreact to technological breakthroughs in the short term—a tendency reflected in today’s share prices and in the extraordinary capital expenditures by AI-focused firms. For example, annual capital spending by hyperscalers has grown at a 25% compound rate over the past decade and is projected to exceed $450 billion this year, reaching $2 trillion by 2028—an amount roughly equivalent to the GDP of Mexico.5, 6 These figures underscore the scale of capital chasing AI-driven returns. See Chart 2.

Such magnitude increases the likelihood that not all investments will prove profitable. Even projects deemed “safe” carry uncertainty. The closest historical parallel is the late-1990s dot-com boom, during which some of the most respected technology companies such as Microsoft and Cisco lost over 2/3 of their market value when the bubble burst. Microsoft required more than 15 years to regain pre-crash valuations.7 While we hesitate to draw direct comparisons, the lessons are clear: today’s exuberance suggests that both sound and unsound ideas will attract capital, and excessive expectations may ultimately go unmet.

If short-term overreaction to innovation can inflate bubbles, long-term underreaction often obscures the enduring benefits of technological progress. While speculative excess may lead to poor investment decisions, it does not negate AI’s transformative potential.

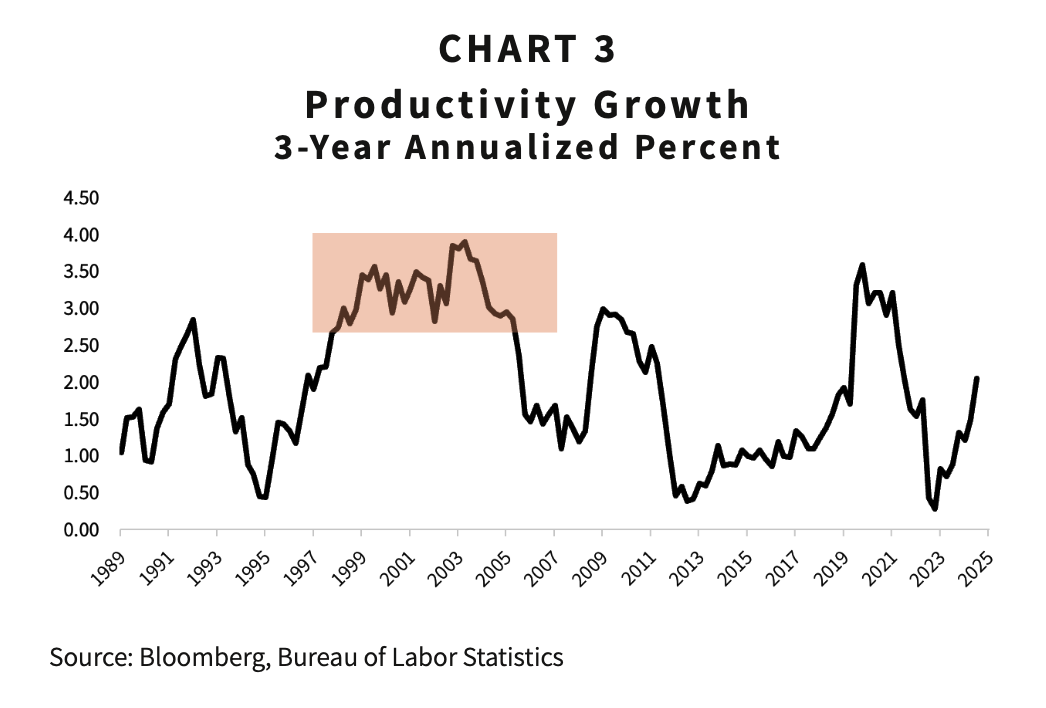

One of AI’s most compelling promises lies in productivity gains. Enhanced search capabilities, rapid document review, and other streamlined workflows are only a few examples of efficiencies AI can deliver. Economists increasingly anticipate a resurgence in productivity growth—defined as output per unit of input—driven by AI adoption. Indeed, the U.S. economy’s resilience in recent quarters, despite labor market softening, has led some to speculate that this trend is already underway. Historical precedent reinforces this view: during the 1990s internet boom, productivity grew at an average annual rate of 2.6%, a pace not sustained since. Higher productivity not only accelerates economic growth but also raises living standards. During that period, real per-capita income rose 2% annually, compared with 1.6% in the subsequent two decades.8

Finally, fears of mass unemployment appear overstated. Rather than wholesale job displacement, AI is likely to reshape roles, reducing routine cognitive tasks and elevating work requiring judgment and coordination. Translation, document review, and error detection may increasingly fall to machines, with humans overseeing quality and context. As economist Roger Bootle observes: “The essence of the coming technological change is to remove umpteen mechanistic jobs from human beings and to leave them in the realm of the truly human.”9 In short, AI should augment human capability, enabling individuals to focus on higher-value activities and fostering a more productive economy.

The surge in AI-related investment bears the hallmarks of a bubble, a bubble that may yet continue to grow before it deflates or pops. Yet technological bubbles such as this one contain transformative potential. While near-term risks for portfolios are real, the long-term outlook for the economy remains promising. AI’s ability to replace routine mental work, enhance productivity, and create new economic opportunities suggests that its ultimate impact will be profound.

1 Bloomberg Artificial Intelligence Aggregate TR equity index and Bloomberg 500 Equal Weight TR equity index, total return from November 30, 2022 through September 30, 2025.

2 As of October, 3, 2025 the top five stocks in the S&P 500 make up 29.8% of the index’s total market capitalization. Figures derived from iShares S&P 500 ETF (IVV).

3 As cited in John Authers. “Assume AI Bubble. What Difference Would It Make?” Bloomberg. October 1, 2025.

4 Bloomberg, price to earnings ratio based on 12-month forward estimates (BE051). Bloomberg Artificial Intelligence Aggregate TR equity index and Bloomberg 500 Equal Weight TR equity index.

5 Bloomberg, Trailing 12-month capital expenditures through June 30, 2025.

6 Rashika Singh and Joel Jose. “Citigroup Forecasts Big Tech’s AI Spending to Cross $2.8 Trillion by 2029.” Reuters. September 30, 2025. GDP by country from the World Bank.

7 Bloomberg. Microsoft common stock total return from 12/27/99 to 12/20/00: -65.2%. Cisco common stock total return from 3/27/00 to 9/27/01: -86.0%. For more lessons from the dot-com bust see GQG Partners. “Dotcom on Steroids.” GQG Research. September 11, 2025. Accessed at https://gqg.com/insights/dotcom-on-steroids/.

8 Bloomberg, Bureau of Labor Statistics. Three-year annualized calculations from Cameron Crise. “The AI Miracle Has Been More Micro Than Macro So Far.” Bloomberg. October 2, 2025. Dot-com boom is defined from the period from December 31, 1995 through December 31, 2005. Real per capita income data from Bloomberg and the Bureau of Economic Analysis.

9 Roger Bootle. The AI Economy: Work, Wealth and Welfare in the Robot Age. Nicholas Brealy Publishing, 2019, pg. 149.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $4 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.