Gavin W. Stephens

CFA

Chief Investment Officer

Chief Investment Officer

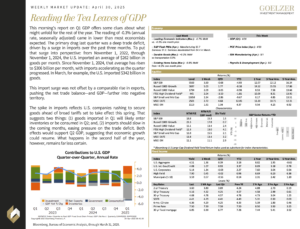

This morning’s report on Q1 GDP offers some clues about what might unfold for the rest of the year. The reading of -0.3% (annual rate, seasonally adjusted) came in lower than most economists expected. The primary drag last quarter was a deep trade deficit, driven by a surge in imports over the past three months. To put that surge into perspective: from November 1, 2022, through November 1, 2024, the U.S. imported an average of $262 billion in goods per month. Since November 1, 2024, that average has risen to $306 billion per month, with imports accelerating as the quarter progressed. In March, for example, the U.S. imported $342 billion in goods.

This import surge was not offset by a comparable rise in exports, pushing the net trade balance—and GDP—further into negative territory.

The spike in imports reflects U.S. companies rushing to secure goods ahead of broad tariffs set to take effect this spring. That suggests two things: (1) goods imported in Q1 will likely enter inventories or be consumed in Q2; and, (2) imports should slow in the coming months, easing pressure on the trade deficit. Both effects would support Q2 GDP, suggesting that economic growth could resume. What happens in the second half of the year, however, remains far less certain.

Weekly Market Update: April 30, 2025