Gavin W. Stephens

CFA

Chief Investment Officer

Chief Investment Officer

Everyone loves a story—even people in finance. To tell stories is as human as eating and drinking. And, just like those essential acts, storytelling can—and arguably should—be a joyful thing. But the impulse to tell a story has a downside. That downside lies in what gets left out or discarded as irrelevant or improbable. The urge to narrate is particularly risky when imposed on complex, multifaceted phenomena such as global economies or financial markets. Omnipresent media—constantly hungry for the next story—only makes these risks more acute.

Everyone loves a story—even people in finance. To tell stories is as human as eating and drinking. And, just like those essential acts, storytelling can—and arguably should—be a joyful thing. But the impulse to tell a story has a downside. That downside lies in what gets left out or discarded as irrelevant or improbable. The urge to narrate is particularly risky when imposed on complex, multifaceted phenomena such as global economies or financial markets. Omnipresent media—constantly hungry for the next story—only makes these risks more acute.

What follows is a brief exploration of why narratives are so prevalent yet fundamentally untrustworthy. We then consider two market narratives that, while not entirely misguided, became overextended and led to unpleasant outcomes for those who embraced them. Finally, we turn to today’s prevailing narrative—offering a cautionary view of its seductive logic and advocating for an investment discipline that acknowledges the fallibility of our understanding.

We interpret data and experiences as naturally as we breathe. In The Black Swan (2007), Nassim Nicholas Taleb argues that our impulse to interpret—or to arrange data and events into sequences of cause and effect—stems from the challenge of storing and retrieving information.1 It takes effort to obtain, store, and recall information. By shaping it into a story, we compress it into something easier to remember.

But this storytelling instinct also distorts reality. It makes the world seem more orderly and predictable than it truly is, excluding the possibility of events that lie outside our narrative frame. While all stories are inherently flawed, narratives in domains with high randomness and vast data—like financial markets—are especially dubious. These narratives become even more suspect when presented as definitive explanations of how things have come to be.

Here are three examples of fallible market narratives at work.

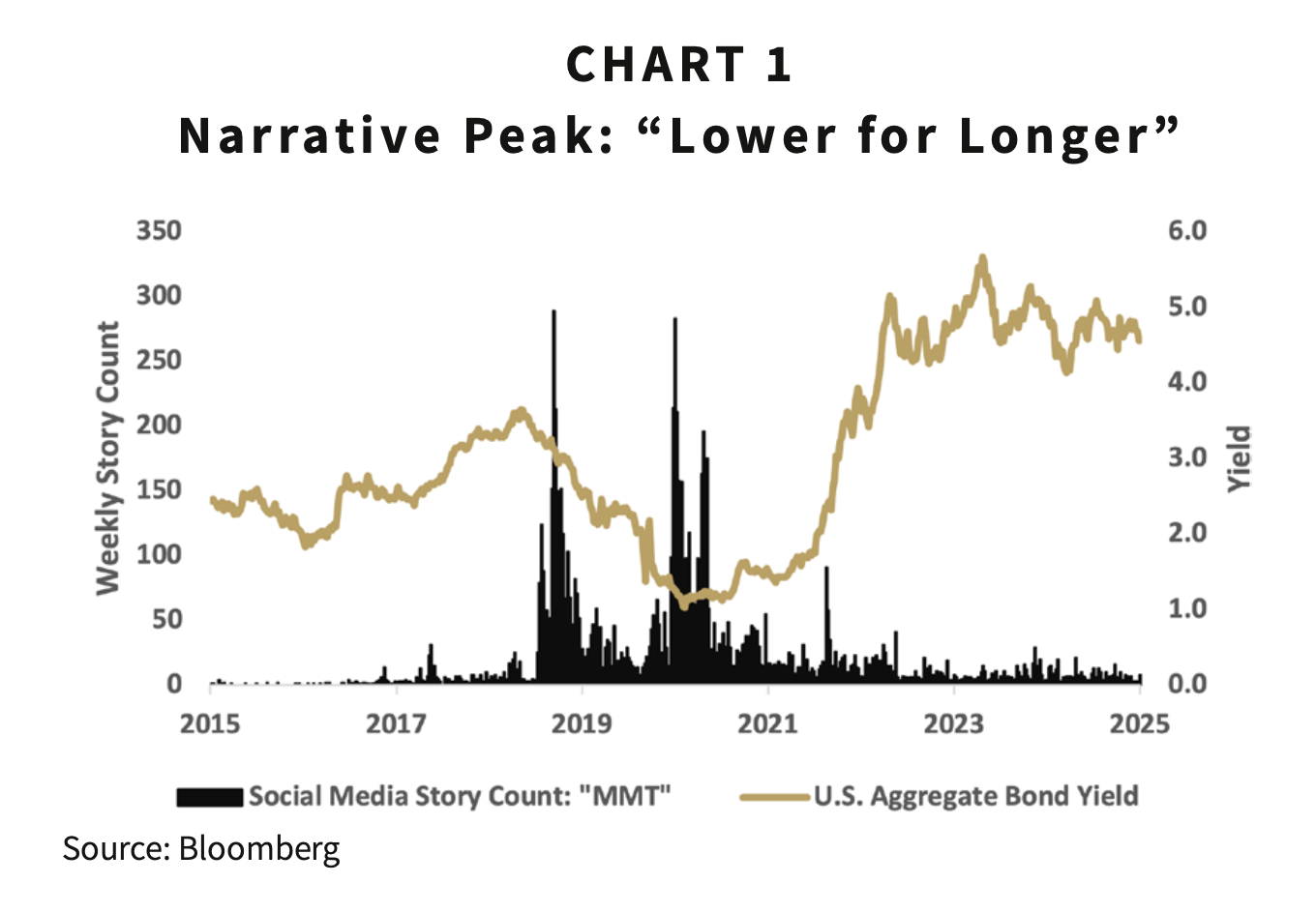

In the decade following the Great Financial Crisis (GFC) of 2008-2009, the 10-year U.S. Treasury bond’s yield averaged 2.5%—a sharp departure from its 50-year pre-GFC average of 7%.2 By the summer of 2016, the 10-year yield had fallen to 1.4%, leaving many seasoned investors baffled. Others, however, saw this drop as evidence that the U.S. economy had fundamentally changed and that interest rates should remain structurally low.

This idea—captured in terms like “Secular Stagnation” or the “New Normal”—argued that evolving demographics, changing savings patterns, and slowing productivity should constrain economic growth and inflation. A novel theory called “Modern Monetary Theory” (MMT) also gained prominence, arguing that governments with control over their currencies should not allow concerns over budget deficits—and their potential inflationary effects—to affect government spending decisions.3 Together, these narratives suggested that interest rates would remain persistently low.

It is perhaps no coincidence that just as interest in MMT peaked, yields on U.S. investment-grade bonds bottomed.4

What the “interest-rates-have-moved-structurally-lower” narrative missed was a resurgence in inflation and a sharp increase in federal spending, partly driven by the needs of an aging U.S. population.5 Those and other factors pushed bond yields higher, with the 10-year Treasury yield peaking at 5% in the fall of 2023. Today, prominent business leaders and strategists forecast that higher yields may persist—or even rise. The “lower-for-longer” narrative has been broken, and investors who bought into it at the peak were left holding the bag: since the bottoming of rates in August 2020, U.S. investment-grade bonds have produced an annualized return of -1.1%.6

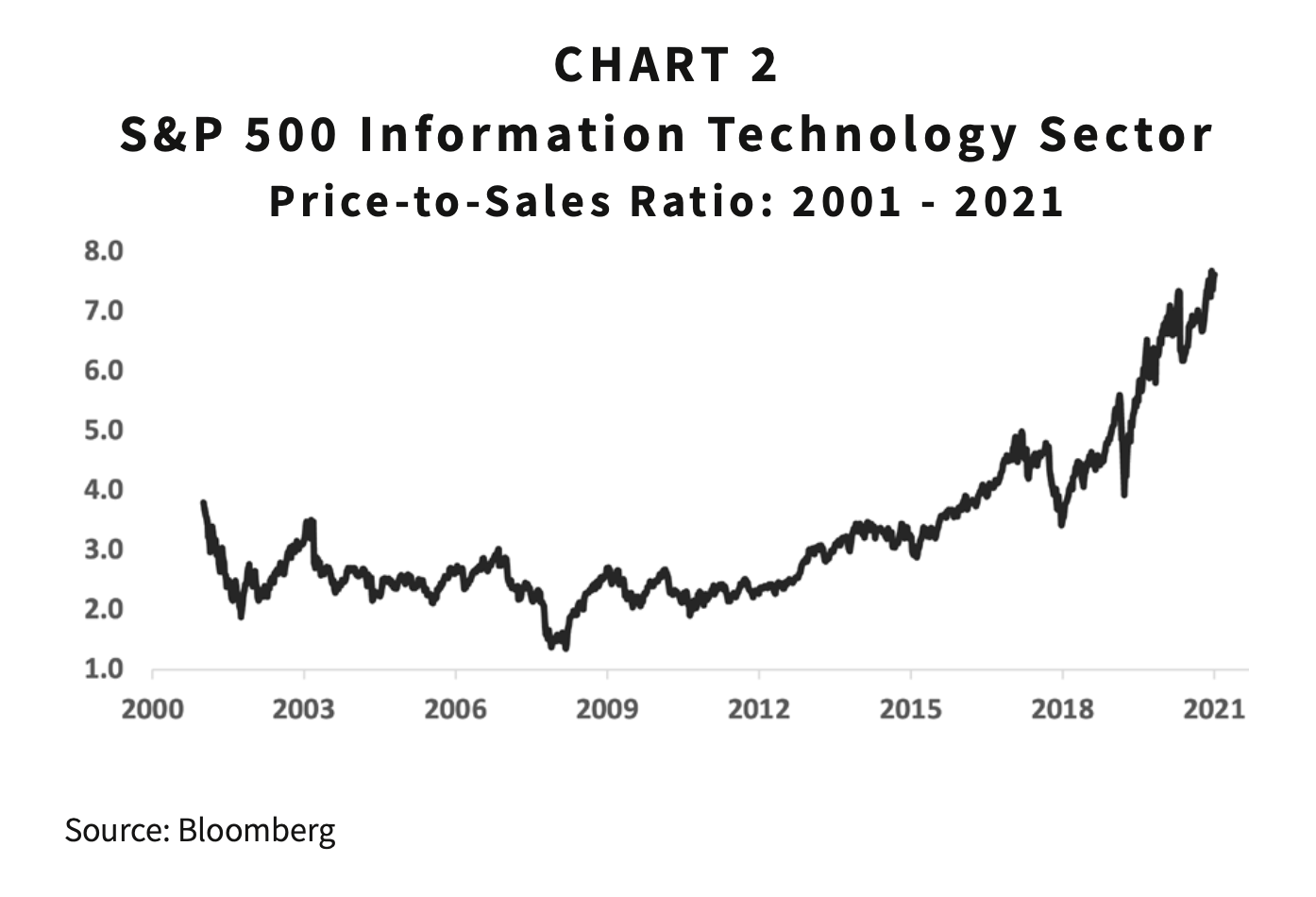

One of the oddities of 2020 was the underperformance of what had traditionally been considered defensive stocks. Consumer staples companies, for example, are generally insulated from economic cycles and have historically outperformed more economically sensitive sectors during recessions. But during the sharp, brief recession of early 2020, consumer staples stocks lagged behind. Instead, technology stocks—which had previously been considered cyclical—outperformed. In 2020, the S&P 500’s Consumer Staples sector trailed the Information Technology sector by 33%.7

Some wrote this off as a once-in-a-century anomaly. Others saw it as validation of the “new economy” narrative, which emphasized the growing dominance of technology and other asset-light industries. These companies appeared relatively immune to the economic shocks of COVID-19, reinforcing their perceived invincibility and their status as the new defensive stocks.

But while their products and services geared toward working from home may have helped them navigate the COVID-19 recession, their stock prices were not immune to market risks. Having emerged from 2020 as market winners, technology stocks continued to rally through 2021. From the March 2020 trough through year-end 2021, the S&P 500 Information Technology sector returned 69%, compared to 56% for the broader index.8 By the end of 2021, the sector’s price-to-sales ratio had reached 7.1x—a 145% premium to the S&P 500 overall.9 That raised the bar for the level of forward profit growth required to propel technology stocks higher.

When recession fears grew in early 2022, these “new defensive” stocks proved not so defensive. Investors began to question how much they were willing to pay for companies with such lofty expectations. For the calendar year 2022, the Information Technology sector underperformed the Consumer Staples sector by 27%.10

As we noted at the outset, narratives are natural—but they can also be dangerous. A dominant narrative in early 2025 is the “end of American exceptionalism,” driven by the recent outperformance of international stocks and the U.S. dollar’s weakest first-half performance in over 50 years.11 In our Insights in January, we addressed this narrative and explained why it—like all narratives—is flawed.12 The U.S. faces real challenges, including unsustainable fiscal policies and a troubling debt burden. But its demographic advantages, robust financial markets, and entrepreneurial culture make the narrative not only flawed, but premature.

So how should one build a portfolio in an era of narrative overreach? A healthy dose of skepticism is essential—both for the stories others tell and the ones we tell ourselves. That skepticism should translate into a portfolio designed to withstand what your best narrative might overlook or dismiss as irrelevant. A truly diversified portfolio may not yield the perfect result if your favored narrative plays out. But it is far more likely to produce an acceptable outcome when that narrative proves incomplete.

1 Nassim Nicholas Taleb. The Black Swan: The Impact of the Highly Improbable. Random House, 2007.

2 Bloomberg, average daily yield of 10-year U.S. Treasury notes, 10 years following and 50 years preceding the fall of Lehman Brothers on September 15, 2008.

3 Modern Monetary Theory (MMT) posits that governments that control their own currencies should not be constrained by budget deficits and related inflationary concerns when it comes to government spending. For background on MMT see Jeanna Smialek, “Is This What Winning Looks Like?” The New York Times, February 6, 2022, nytimes.com/2022/02/06/business/economy/modern-monetary-theory-stephanie-kelton.html.

4 Bloomberg. Weekly social-media story count with the topic “Modern Monetary Theory.” Bond yield is the yield-to-worst of the U.S. Aggregate Bond Index, which fell to an all-time-low of 1.02% on August 4, 2020.

5 For more on the relationship between higher bond yields and an aging U.S. population see Allison Schrager’s article, “We Are Probably All Wrong About Interest Rates.” Bloomberg. February 9, 2023.

6 Bloomberg, total annualized return of the U.S. Aggregate Bond Index from August 4, 2020 through June 30, 2025.

7 Bloomberg, total return of S&P 500 Level 1 Information Technology and Consumer Staples sectors from January 1, 2020 through December 31, 2020.

8 Bloomberg, total return of S&P 500 Level 1 Information Technology sector and S&P 500 Index from March 23, 2020 through December 31, 2021.

9 Bloomberg, forward price-to-sales ratio of S&P 500 Information Sector and S&P 500 Index as of December 31, 2021.

10 Bloomberg, total return of S&P 500 Level 1 Information Technology and Consumer Staples sectors from January 1, 2022 through December 31, 2022.

11 George Lei and Cater Johnson. “Dollar Index Slumps 10.8% in Biggest First-Half Loss Since 1973.” Bloomberg. June 30, 2015.

12 Gavin W. Stephens, Insights, “American Exceptionalism Amid a Gloom Bloom,” January 2025, goelzerinc.com/insights_post/american-exceptionalism-amid-a-gloom-bloom.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.