Chief Investment Officer | Principal

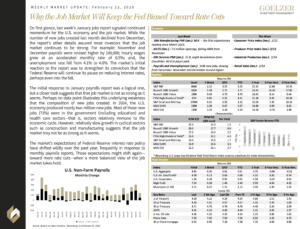

On first glance, last week’s January jobs report signaled continued momentum for the U.S. economy and the job market. While the number of new jobs created last month declined from December, the report’s other details assured most investors that the job market continues to be strong. For example: November and December payrolls were revised higher by 100,000; hourly wages grew at an accelerated monthly rate of 0.5%; and, the unemployment rate fell from 4.1% to 4.0%. The market’s initial reaction to the report was to strengthen its conviction that the Federal Reserve will continue its pause on reducing interest rates, perhaps even into the fall.

The initial response to January payrolls report was a logical one, but a closer look suggests that that job market is not as strong as it seems. Perhaps no data point illustrates this underlying weakness that the composition of new jobs created. In 2024, the U.S. economy produced nearly two million new jobs. Most of these new jobs (73%) were in the government (including education) and health care sectors—that is, sectors relatively immune to the economic cycle. However, relatively slow growth in cyclical sectors such as construction and manufacturing suggests that the job market may not be as strong as it seems.

The market’s expectations of Federal Reserve interest-rate policy have shifted wildly over the past year, frequently in response to monthly payrolls reports. Those expectations might shift again—toward more rate cuts—when a more balanced view of the job market takes hold.

Weekly Market Update: February 12, 2025