Gavin W. Stephens

CFA

Chief Investment Officer

Chief Investment Officer

We are frequently asked about the upcoming U.S. election and how the results of that election might affect the economy and markets. What follows is a concise summary of certain policy differences between former President Donald Trump and current President Joe Biden that we view as most relevant to investors. The summary is not intended to be comprehensive or to imply any judgment on the policies proposed.

Further, we should note that the policy ideas outlined below may not become reality in their fullest expression; the possibility of a divided government will require compromise to enact portions of what we discuss here. We also note that, despite obvious differences in style and substance, the two candidates appear to share similar attitudes toward trade and debt. Finally, we conclude with some guidance from history—guidance that points to the likely relief that markets may feel when the election season is over.

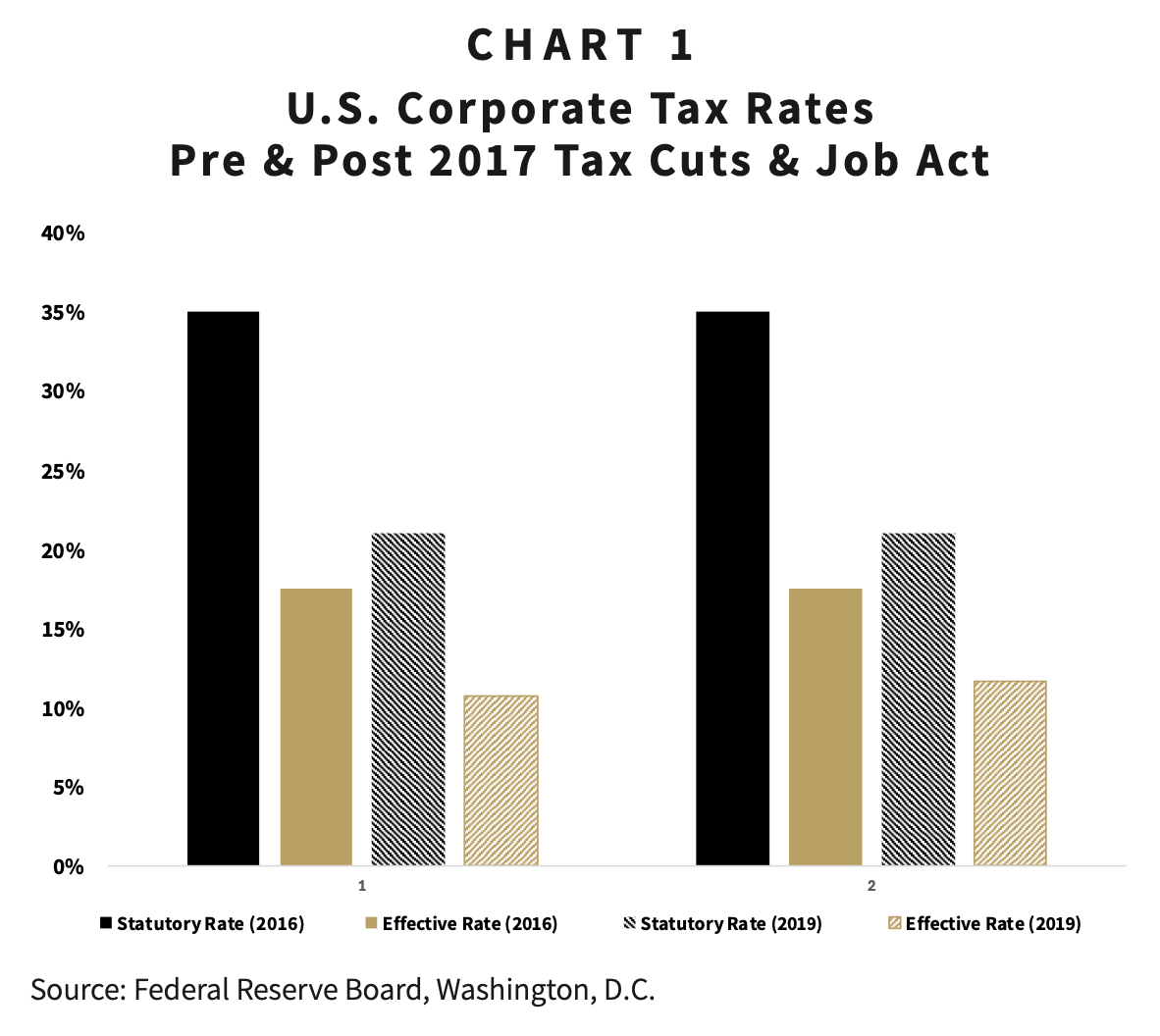

Our two presidential candidates differ sharply on individual and corporate tax policy. These policy differences come into relief when considering how each candidate proposes to address the looming expiration of certain sections within 2017’s Tax Cuts and Jobs Act (TCJA). Aimed to simplify the personal tax code and to accelerate economic growth, the TCJA lowered personal tax rates, increased the level of the standard deduction, limited deductions on state and local taxes and mortgage interest, and doubled the lifetime estate-tax exclusion—among other changes to the U.S. tax code. The TCJA also permanently reduced the corporate tax rate from 35% to 21%. Without congressional action, the changes to individual tax policy will expire at the conclusion of 2025.

Former President Trump has pledged to make the expiring provisions of the TCJA permanent and to further reduce the corporate tax rate to 20%. President Biden, alternatively, has proposed increasing the top individual income tax rate to 39.6% and, for those earning above $1 million, taxing long-term capital gains and qualified dividends at ordinary income rates. He has also proposed taxing unrealized capital gains at death above a $5 million exemption. In addition to raising income taxes on high income earners, President Biden has argued for raising the corporate tax rate to 28% and increasing taxes on foreign-derived corporate income.1

For investors, higher corporate tax rates would likely pose a challenge to corporate earnings, especially to earnings from large U.S. multinational corporations that would be subject to higher taxes on foreign-derived income. As Chart 1 shows, publicly traded multinational companies have benefited most from the TCJA’s lowering of the corporate tax rate, with their average effective tax rate falling nearly 7% after the passing of the TCJA.2

An increase in the statutory corporate rate from 21% to 28% is unlikely to be met with an equal increase in the effective tax rate; the effect on corporate earnings would thus be smaller than implied by the increase to the statutory rate. Nevertheless, any increase in the corporate tax rate would weaken a source of earnings growth among the U.S.’ largest public companies.

The two candidates also differ sharply on energy policy and their preferred sources of energy production. Former President Trump has expressed preference for fossil-fuel production and skepticism regarding renewable energy sources such as wind. It would be reasonable to expect a second Trump administration to loosen barriers to fossil-fuel production and to expand access to domestic drilling sources. On the other hand, the Biden Administration has explicitly favored renewable energy sources, having declared its intention to move the U.S. economy on “path to achieve net-zero emissions, economy-wide, by no later than 2050.”3 The resulting policy actions, through executive orders and legislation, have resulted in tax incentives favoring the expansion of renewable energy sources and regulations that have increased the cost of fossil-fuel production.

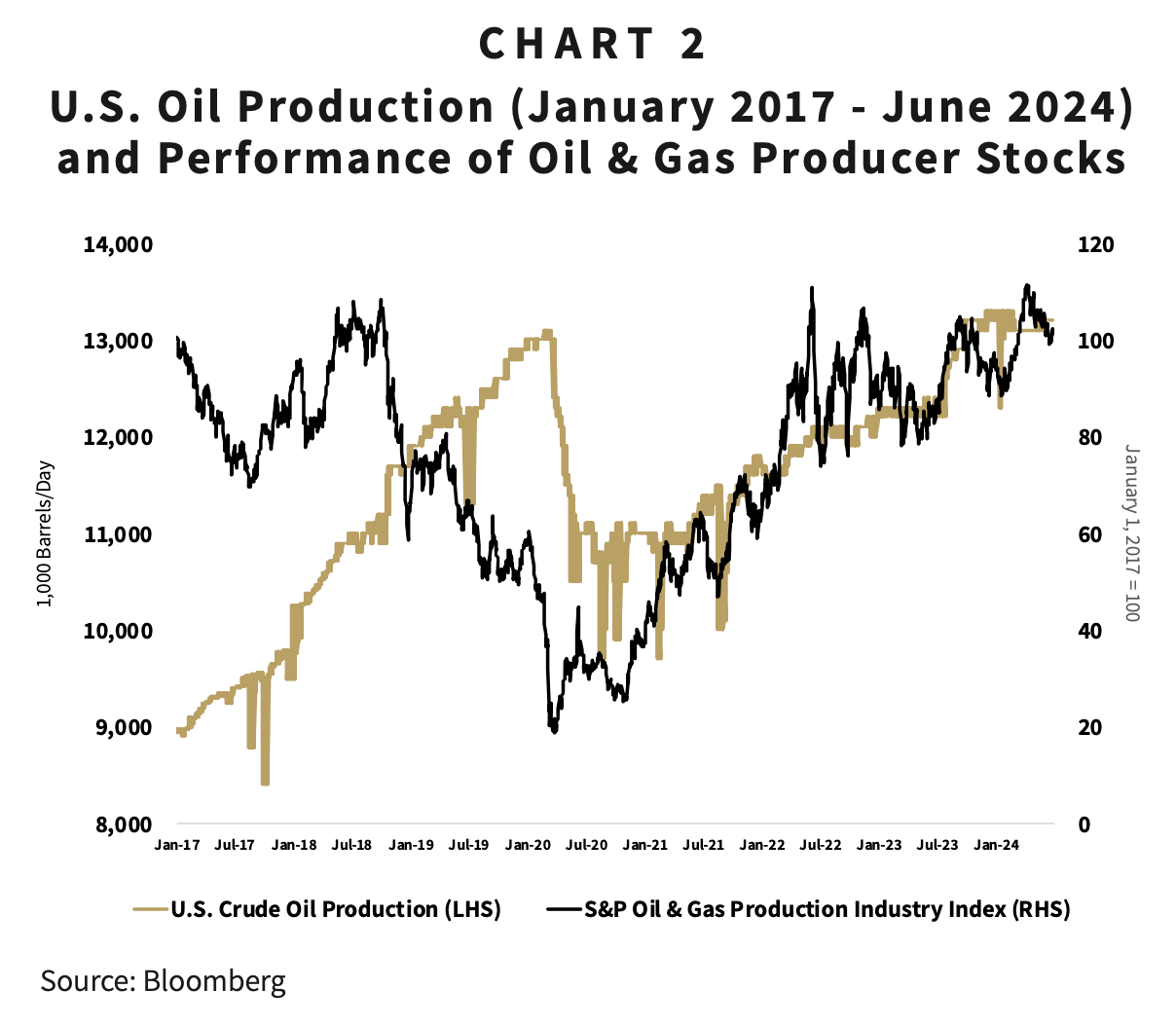

While the candidates’ energy preferences are clear, the effects of those preferences on markets are less so. On first glance, a pro-fossil fuel agenda would appear to auger well for returns from oil and gas stocks. However, to the extent that such policies lead to increased oil supply, the price of oil is subject to fall. The profits of oil and gas companies could decline as a result. Alternatively, increased oil and gas regulation could lower supply and increase energy prices, thus supporting the profits of oil and gas companies. As Chart 2 shows, this dynamic occurred during the Trump and Biden administrations.4

During the first three years of the Trump administration, U.S. oil production increased by 13% per year from 8.8 million barrels per day (BPD) to 13 million BPD. Looser regulation during the Trump administration helped drive oil supply higher but did not prove helpful to the returns of oil and gas producers’ stocks. Returns from the S&P Oil and Gas Explorers Index were negative 61% during the first three years of the Trump administration, whereas during the first three years of the Biden administration—a period in which oil production increased more modestly—returns from that same index were a positive 161%. The implications for stock returns are not as obvious as policies might suggest.

While the candidates may contrast sharply on taxes and regulation, they appear to share similar views on trade and debt. Both Trump and Biden administrations have instituted tariffs on foreign goods, particularly goods imported from China. China has fallen from being the U.S.’ largest source of imported goods to its fourth largest behind Europe, Mexico, and Canada.5 In addition, neither candidate has expressed commitment to lowing the federal budget deficit and slowing the growth in the U.S. national debt, the latter of which is approaching 100% of GDP. Combined with higher interest rates, the growing level of U.S. debt is expected to raise spending on interest to the third-largest item in the federal budget, ahead of defense and behind only Medicare and Social Security.6 Either outcome to this year’s Presidential election will likely result in continued economic strains between the U.S. and China and a growing burden of debt on the U.S. economy.

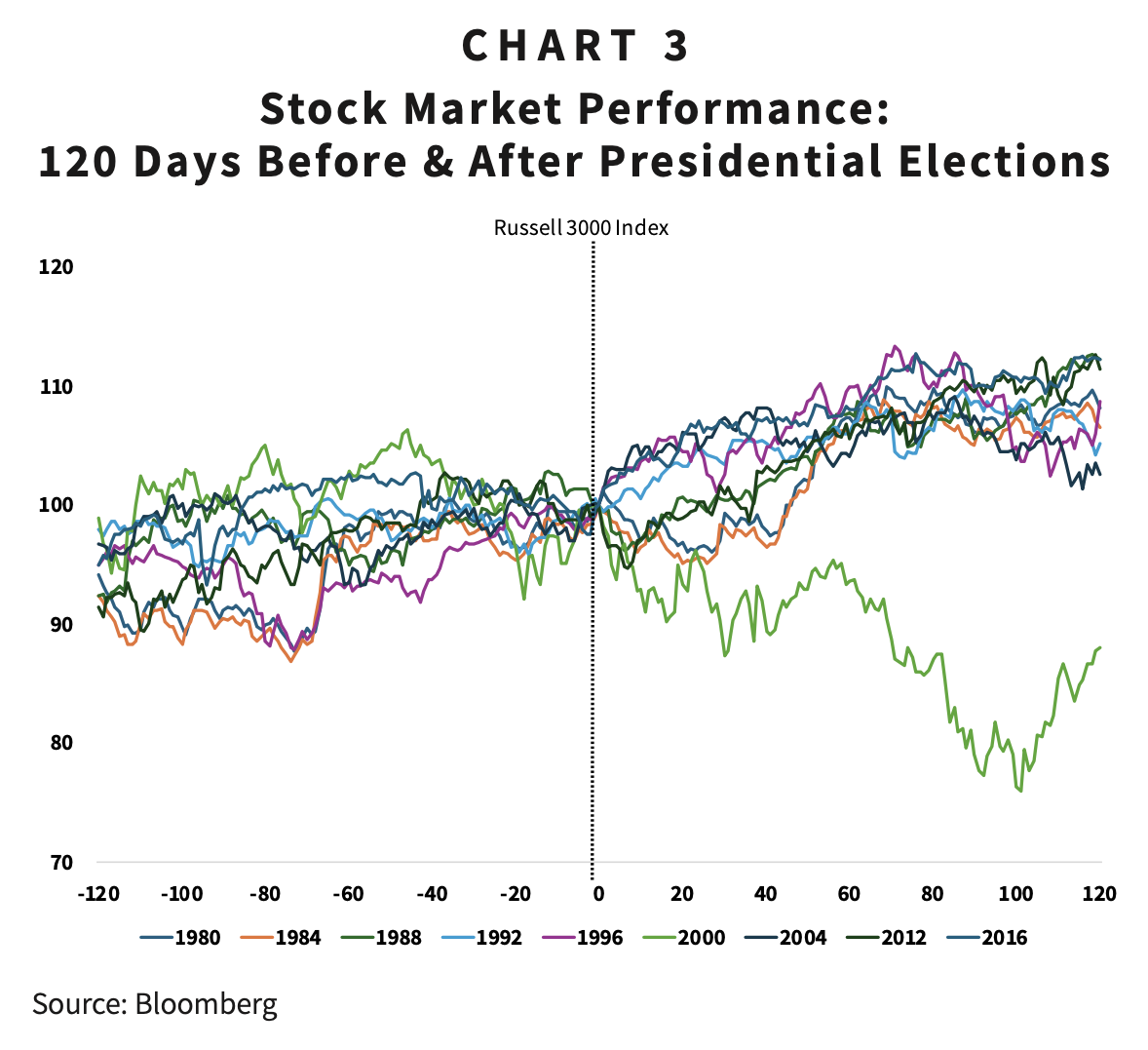

Just as we cannot predict the outcome of this year’s election, we cannot predict how the prices of certain financial assets will react when that outcome becomes clear. What we expect, however, is that markets are likely to experience heightened volatility in the months preceding the election as investors weigh the probabilities of various electoral outcomes. As that outcome is clear, however, volatility is likely to abate. Chart 3 illustrates this dynamic.7

In the election years included above, we see that stock prices have struggled to find direction in the months preceding presidential elections. Following the election, however, stocks have produced positive returns 8 of 9 times, with an average return of 8% in the 120 days following an election. (The data include six instances in which a Republican won the election and three in which a Democrat prevailed.8) While policy will affect the economy and the markets, uncertainty about which policy will prevail appears to be the largest obstacle to positive returns.

Perhaps like the U.S. electorate, the stock market breathes a sigh of relief once the election ends.

1 Esha Dey. “What the Biden-Trump Rematch Means for U.S. Stocks: Quick Take.” Bloomberg. June 25, 2024. See also, “Where Do The Candidates Stand on Taxes?” The Tax Foundation, http://www.taxfoundation.org/research/federal-tax/2024-tax-plans. Top individual tax rates would apply to individuals earning over $400,000 and joint filers earning over $450,000. In addition to proposing an increase in the corporate tax rate, President Biden has proposed increasing the global intangible low-taxed income (GILTI) tax rate from 10.5% to 21% and raising the tax rate on foreign-derived intangible income (FDII).

2 Dobridge, Christine L., Patrick Kennedy, Paul Landefeld, and Jacob Mortenson (December 2023). “The TCJA and Domestic Corporate Tax Rates,” Finance and Economics Discussion Series 2023-078. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2023.078.

3 “Executive Order on Tackling the Climate Crisis at Home and Abroad,” The White House, January 27, 2021, https://www.whitehouse.gov/briefing-room/presidential-actions/2021/01/27/executive-order-on-tackling-the-climate-crisis-at-home-and-abroad.

4 Bloomberg, U.S. Department of Energy, S&P Oil & Gas Exploration & Production Select Industry Total Return Index, from November 6, 2016 through June 24, 2024.

5 JP Morgan, “Investing in an Election Year,” December 31, 2023.

6 Congressional Budget Office, “An Update to the Budget and Economic Outlook: 2024 to 2034,” June 2024, https://www.cbo.gov/publication/60419.

7 Bloomberg. The Russell 3000 Index is composed of 3,000 U.S. companies and captures stocks in large, mid, and small-capitalization indexes

8 We exclude the election of 2008, the only election year under consideration that occurred in the middle of an official economic recession.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.