Senior Portfolio Manager

The conflict between hard and soft economic data is becoming increasingly relevant as we approach the end of the first quarter. Economic indicators have weakened, including a sizable drop in consumer sentiment and downward revisions to earnings growth projections. On the positive side, a steady unemployment rate, moderating inflation, healthy credit spreads, and strong corporate fundamentals are helping to cushion uncertainty in the current market and political environment.

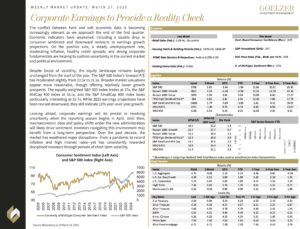

Despite bouts of volatility, the equity landscape remains largely unchanged from the start of the year. The S&P 500 Index’s forward P/E has moderated slightly from 22.5x to 21.5x. Broader market valuations appear more reasonable, though offering relatively lower growth prospects. The equally weighted S&P 500 Index trades at 17x, the S&P MidCap 400 Index at 16.1x, and the S&P SmallCap 600 Index looks particularly interesting at 15.7x. While 2025 earnings projections have been revised downward, they still indicate 11% year-over-year growth.

Looking ahead, corporate earnings will be pivotal in resolving uncertainty when the reporting season begins in April. Until then, macroeconomic data and policy shifts under the new administration will likely drive sentiment. Investors navigating this environment may benefit from a long-term perspective. Over the past decade, the market has weathered major disruptions—from a pandemic to record inflation and high interest rates—yet has consistently rewarded disciplined investors through periods of short-term volatility.

Weekly Market Update: March 27, 2025