Sara J. Omohundro

CFA

Investment Strategist

Investment Strategist

The typical term of a private asset investment drawdown fund is ten years, meaning the fund manager should exit all deals return capital to investors by the tenth year. However, many funds are nearing the end of their term in an environment with limited exit opportunities—M&A has slowed down in recent years, and IPOs have become nearly nonexistent. As a result, funds are hanging on to their deals for longer. Fund investors who want liquidity sooner rather than later must turn to the secondaries market to sell their positions. The secondaries market is not a public exchange, but rather the private dealings of investors buying and selling illiquid fund holdings before a traditional exit.

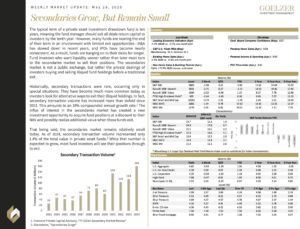

Historically, secondary transactions were rare, occurring only in special situations. They have become much more common today as investors look for alternative ways to exit their illiquid holdings. In fact, secondary transaction volume has increased more than sixfold since 2013. This amounts to an 18% compounded annual growth rate.1 The influx of interest in the secondaries market has created a new investment opportunity to acquire fund positions at a discount to their NAV and possibly realize additional value when those funds exit.

That being said, the secondaries market remains relatively small today. As of 2024, secondary transaction volume represented only 1.4% of the total value in private asset funds.2 While that number is expected to grow, most fund investors will see their positions through to exit.

1. Evercore Private Capital Advisory, “FY 202a4 Secondary Market Review”

2. Blackstone, “Secondaries Surge”

Weekly Market Update: May 28, 2025