Senior Portfolio Manager

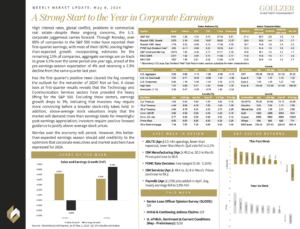

High interest rates, global conflict, problems in commercial real estate—despite these ongoing concerns, the U.S. corporate juggernaut carries forward. Through Monday, over 85% of companies in the S&P 500 Index have reported their first-quarter earnings, with most of them (80%) posting higher-than-expected growth. Incorporating estimates for the remaining 15% of companies, aggregate earnings are on track to grow 6.5% over the same period one year ago, ahead of the pre-earnings-season expectation of 4% and reversing a 2.5% decline from the same quarter last year.

Has the first quarter’s positive news cleared the fog covering the outlook for the remainder of 2024? Not so fast. A closer look at first-quarter results reveals that the Technology and Communication Services sectors have provided the heavy lifting for the S&P 500. Excluding these sectors, earnings growth drops to 3%, indicating that investors may require more convincing before a broader stock-rally takes hold. In addition, above-average stock valuations imply that the market will demand more than earnings beats for meaningful post-earnings appreciation; investors require positive forward guidance to justify above-average stock prices.

Worries over the economy will persist. However, this better-than-expected earnings season should add credibility to the optimism that corporate executives and market watchers have expressed for 2024.

Weekly Market Update: May 8, 2024