Chief Investment Officer

Last year, we published two quarterly Insights papers noting the narrow performance of the U.S. stock market, and for good reason. Over half of the S&P 500 Index’s 24.2% price return in 2023 was driven by a small group of large technology companies.1 This year, we find it necessary to explore further this narrow stock market, attempting to explain how we got here and what we might expect going forward.

Through the first three months of 2024, the S&P 500 has again produced an unexpectedly strong total return of 10.6%, leaving the index at a level higher than the most optimistic of year-end estimates.2 A small cohort of large U.S. technology companies, each associated with the development and application of artificial intelligence (AI), have accounted for much of this positive performance. Through the first quarter, the largest six companies in the S&P 500—each valued at over $1 trillion—have produced just over 50% of the S&P 500’s price return.3 As a result, the prominence of large-cap technology stocks—measured below by the combined market capitalization of these “Super Six” technology companies—has grown to nearly 30% of the S&P 500’s total value.4

Experiencing a narrow stock market again, investors may wonder whether we stand atop of stock market bubble, supported largely by hopes and dreams rather than durable earnings extending into the future.

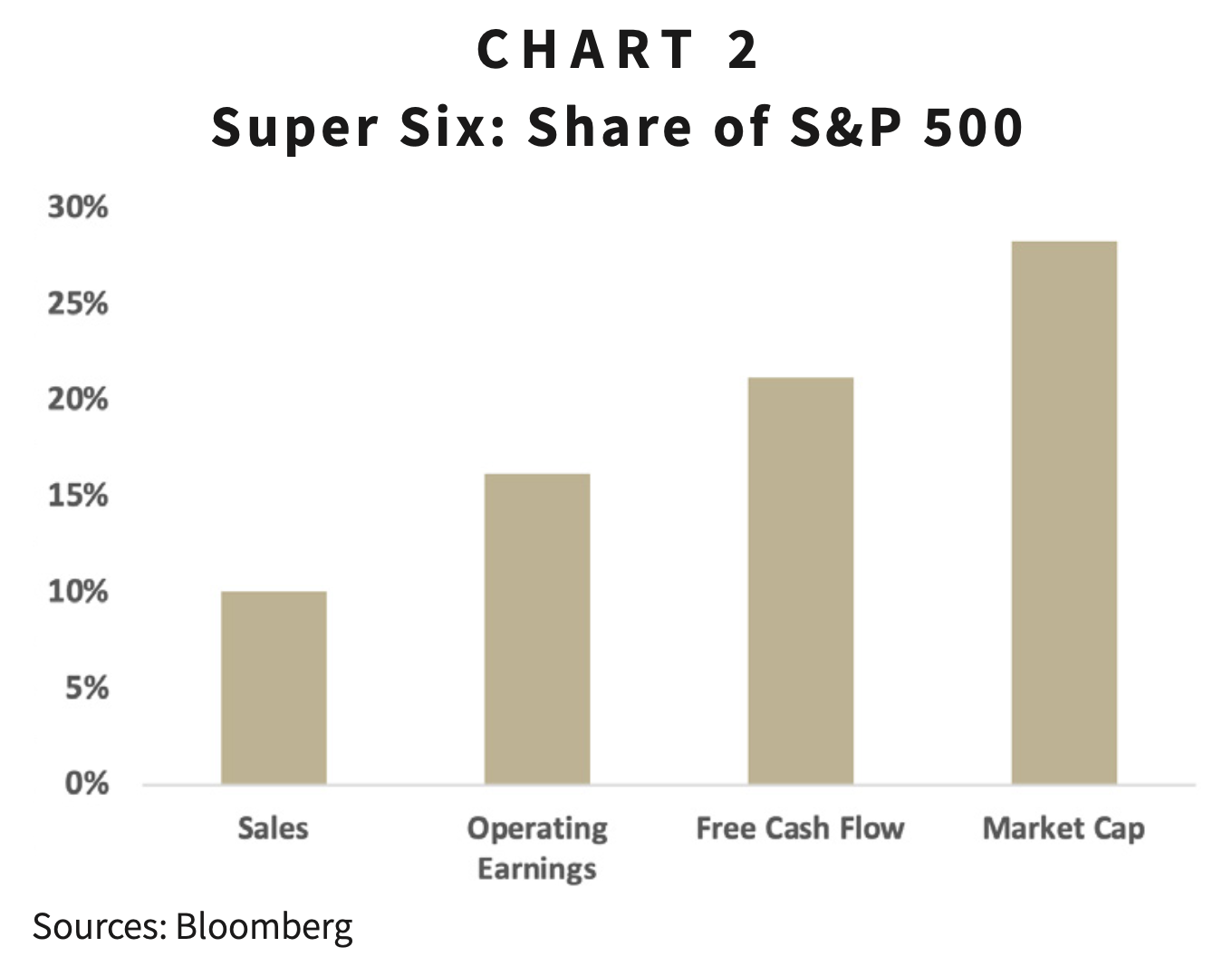

Dismissing the stock returns of the Super Six as manifestations of groundless exuberance might feel satisfying. But to do so would be to ignore the remarkable profitability that these companies have achieved. Not only have companies such as Nvidia grown their revenues at astonishing rates, but they have also done so while growing profits. Chart 2, for example, shows how much these companies contribute to the aggregate revenues, profits, and cash flows of companies within the S&P 500.

While these companies have grown to occupy a historically large portion of the index’s total size, it is equally noteworthy that these companies have contributed a large portion of that market’s profits. The Super Six account for just over 1% of companies in the S&P 500; yet they generate over 15% of the S&P 500’s operating earnings and over 20% of its cash flow.5

How much farther can these stocks go? As much as we might wish, we cannot answer that question. However, we find three things of note.

First, the larger these companies become, the more scrutiny they will invite—both from competitors and, perhaps, from regulators. The former could threaten future returns by introducing more competition for profits. The latter may declare that competition is unfair and that these companies need to be broken up or somehow constrained, challenging their current advantages of scale.

Second, expectations for these companies are high: among the Super Six, expectations over the next five years are for average annual earnings growth of 21%.6 To put these expectations into context, the S&P 500 has averaged 6% annual earnings growth over the past two decades.

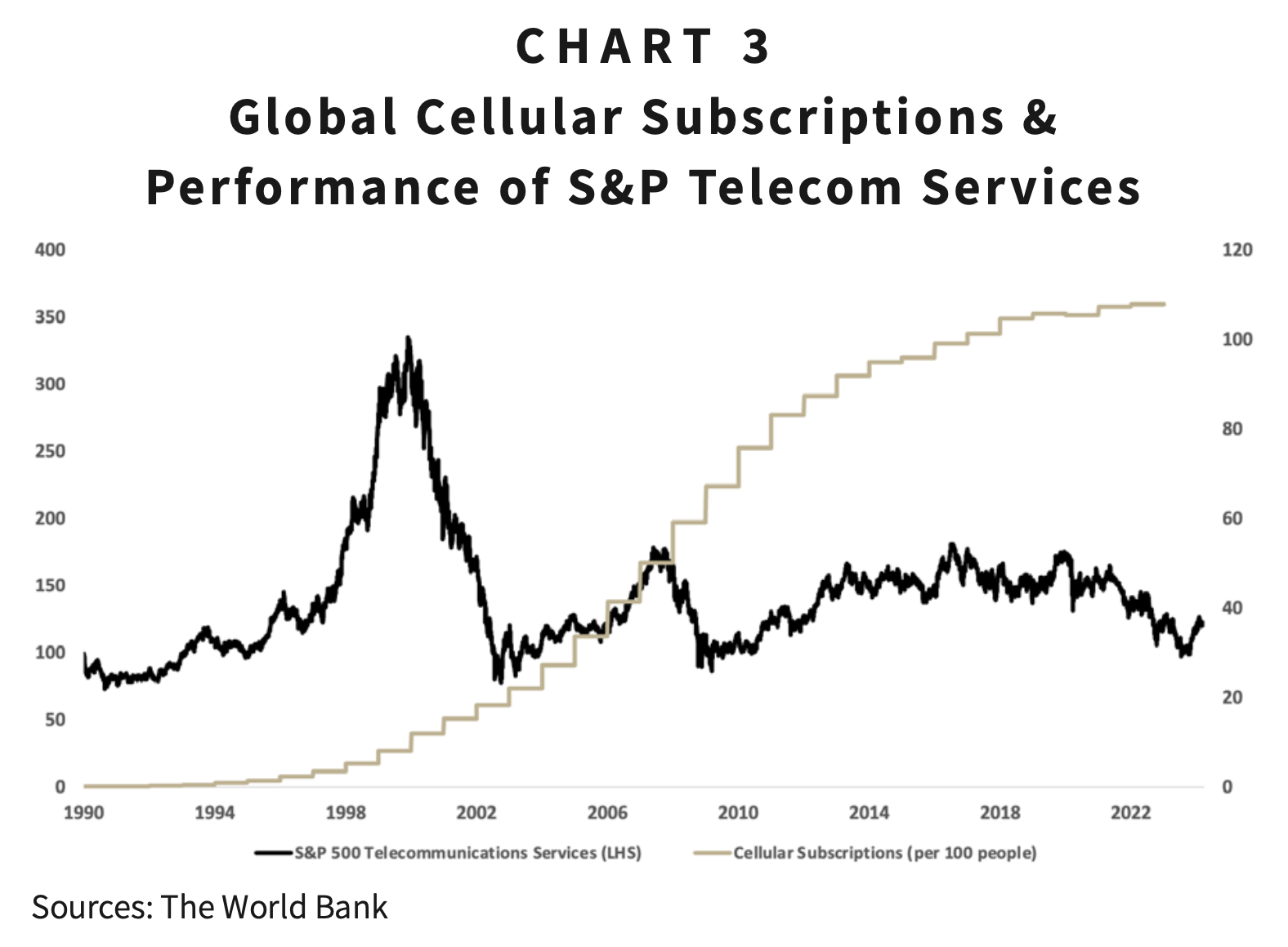

Third, while the market may be correct in its enthusiasm over the transformative potential of AI, that enthusiasm does not ensure strong investment returns moving forward. In fact, to the degree that this enthusiasm has expressed itself in higher stock prices, the prospects for future returns get tougher. For example, in the early 1990s, investors expressed similar excitement over cellular phone technology by bidding up the shares of companies providing its critical infrastructure.

Investors were correct in their assessment of the growth in cellular technology. According to the World Bank, more cellular subscriptions exist today than people.7 As these subscriptions have skyrocketed, however, the once-loved cellular technology stocks have produced disappointing returns for investors. Since 1990, the S&P Telecommunication Services Industry Group has returned 4.8% annually while the S&P 500 produced 10.4% over the same period.8

Rather than predicting whether the stock prices of the Super Six will fall, we find it more useful to ask this question: “What might make the past year’s laggards collectively perform as well or better than the Super Six going forward?”

We find two factors working in favor of the laggard group.

First, lower growth expectations for these stocks equates to greater probability of positive earnings surprises and a reassessment of earnings potential. For example, the expected 2024 year-over-year growth rate for the S&P 500’s Financials sector is 4%; a modest beat of those expectations, say by 1%, equals a relative surprise of 25%. With much higher earnings growth expectations, a similar 1% earnings surprise among the Super Six would likely underwhelm—perhaps even disappoint—investors.

Second, starting valuations are reasonable among the larger universe of U.S. stocks. The equal-weight S&P 500, which neutralizes the effect of the Super Six on the index’s price, trades at a forward 12-month price-to-earnings ratio of 18, a level close to its 10-year long-term average; among the Super Six, the average of that same ratio is 30, reflecting expectations for growth that leave scant room for error.

Companies that grow into market leaders should be doing something right. By providing key infrastructure into what could be the most transformative technology since the widespread adoption of the internet—and doing so on top of their other growing and highly profitable businesses—today’s market leaders undoubtedly are doing something right. The superior fundamentals of the Super Six are mesmerizing. Investors should be careful, however, to keep their portfolios from becoming overly concentrated in these stocks. For while much of the promise of these six stocks has been realized, the growing value of many of the market’s laggards has gone unrecognized. The latter fact sets the stage for better relative performance in the days ahead.

It is appropriate to pause and recognize the remarkable profits generated by the market’s recent winners. It is even more appropriate to stay diversified.

1 Last year, the “Magnificent Seven” (Alphabet, Amazon, Apple, Microsoft, Meta Platforms, Nvidia, and Tesla) accounted for over 50% of the S&P 500’s price return.

2 Lu Wang. “Strategists’ S&P 500 Index Estimates for Year-End 2024.” Bloomberg, January 19, 2024. Two analysts—FundStrat’s Tom Lee and Oppenheimer’s John Stolzfus—predicted that the S&P 500 would end the year at 5,200. It closed the first quarter at 5,254. Year-to-date returns are total returns.

3 Bloomberg, as of March 31, 2024.

4 Bloomberg, as of April 4, 2024. Calculations based on holdings of iShares S&P 500 Index ETF (IVV). The “Super Six” include Alphabet, Amazon, Apple, Microsoft, Meta Platforms, and Nvidia.

5 Bloomberg, as of March 21, 2024. Holdings based on iShares S&P 500 ETF (IVV). Figures are based on trailing 12 months.

6 Bloomberg, as of March 24, 2024.

7 The World Bank. Accessed at https://data.worldbank.org/indicator/IT.CEL.SETS.P2?end=2022&start=1990. Chart produced originally by Deutsche Bank’s Jim Reid.

8 Bloomberg, total annualized returns from December 31, 1989 through March 31, 2024.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.