Senior Consultant

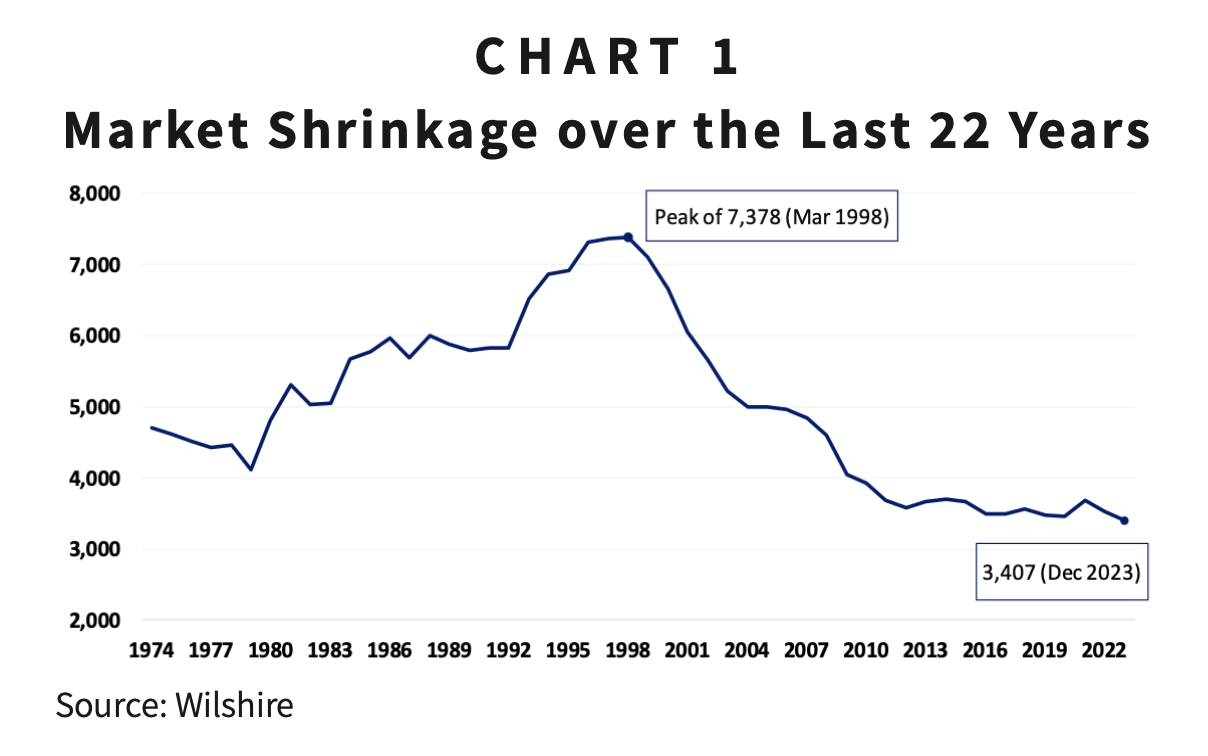

A frequent topic in the financial world has been the downward trend in the number of publicly listed companies in the U.S. stock markets. Peaking back in the mid-1990s at around 7,400, a noticeable and consistent decline can be observed in reaching the approximately 3,400 publicly traded companies in the U.S. today.1

While many factors are at play, consensus around what is driving this phenomenon generally focuses on at least three factors:

In his most recent shareholder letter, JPMorganChase CEO Jamie Dimon acknowledges the serious implications of this trend citing these and other challenges facing public companies and calls for a “frank assessment of the regulatory landscape.”2 While a comprehensive report of the current and potential consequences of this trend is outside of the scope of this paper, we will point out two important observations we have seen and the potential implications for investors.

The motivation for private companies to stay private provides an expanding choice of older, more stable, and more profitable companies accessed via private equity investing. While we acknowledge there is more to it, all else being equal, more and better choices of quality investments, with proven track records increases the attractiveness of private equity at the expense of public equity.

According to IPO research compiled by Professor Jay R. Ritter of the University of Florida, private companies are getting older and larger before IPO (i.e., “going public”).3 Since 1999, the median age of a company at IPO has tripled from 4 years to 12 years while the median market cap at issuance has increased 312% from $453 million to over $2 billion. This delay of issuance also allows private equity investors the opportunity to extract greater value from an entity before public offering. Public investors interested in companies like Uber, Spotify, and Airbnb would have been required to wait over 10 years from their formation before purchasing shares.

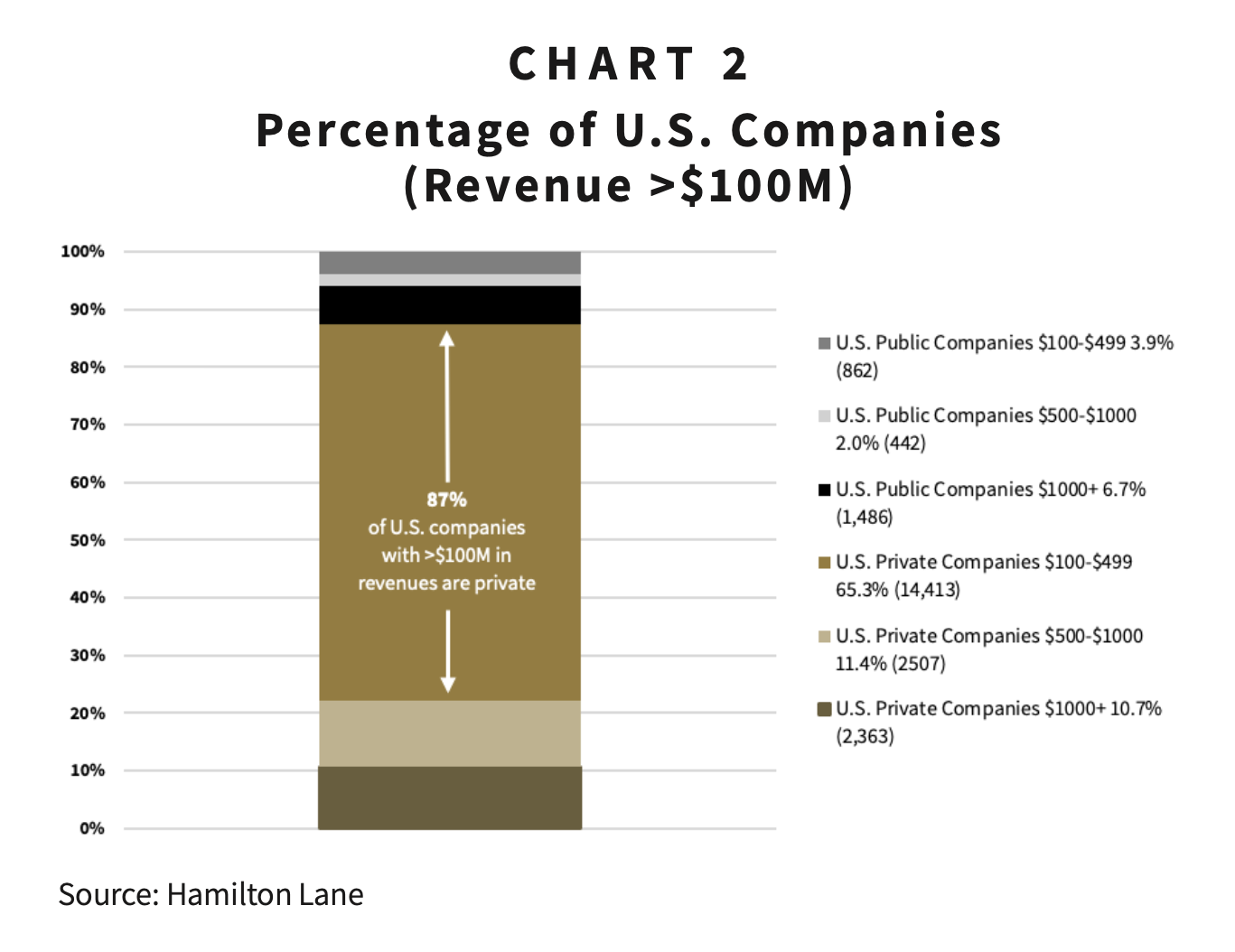

Today, we see significantly more U.S. private companies with over $1 billion in annual revenues compared to public companies and a substantial dispersion of the number of companies with over $100 million. As Chart 2 shows, 87% of U.S. companies with revenue greater than $100 million are privately owned.4

For sophisticated and suitable investors, the ability to choose from an expanded opportunity set of attractive investment opportunities increases the likelihood of earning greater returns in their portfolios. The important drawback of this phenomenon is that retail investors having limited or no access to private equity markets are kept from this opportunity. Thus, eliminating an important avenue for wealth creation among smaller U.S. investors, forcing them to choose among a pool of fewer, less diversified, public companies.

Another result of the decline in the number of public companies is the characteristics of some of the more popular market indices, particularly those constructed based primarily on a static membership count. A recent paper published by Wilshire illustrates the potential implications of this phenomenon. The Russell Indices are constructed by static membership count of eligible U.S. stocks ranked in size from largest to smallest. The top 200 stocks in this index (known as the Russell 200) are considered “large cap.” The next 800 are considered mid cap, and stocks ranking from #1,001 to #3,000, and the Russell 2000 are considered small. When the universe of stocks was much larger, there were plenty of companies from 3001 and lower (called microcap), considered by many investors to be too small and risky for inclusion in a portfolio. Today, with a universe of closer to 3,400, very few companies fall below the threshold of the Russell 2000 index.

This has caused the Russell 2000 Index to look much different today. Investors who are not paying attention could be buying a small cap index with much different risk characteristics than they anticipated or were used to 10 to 15 years ago.

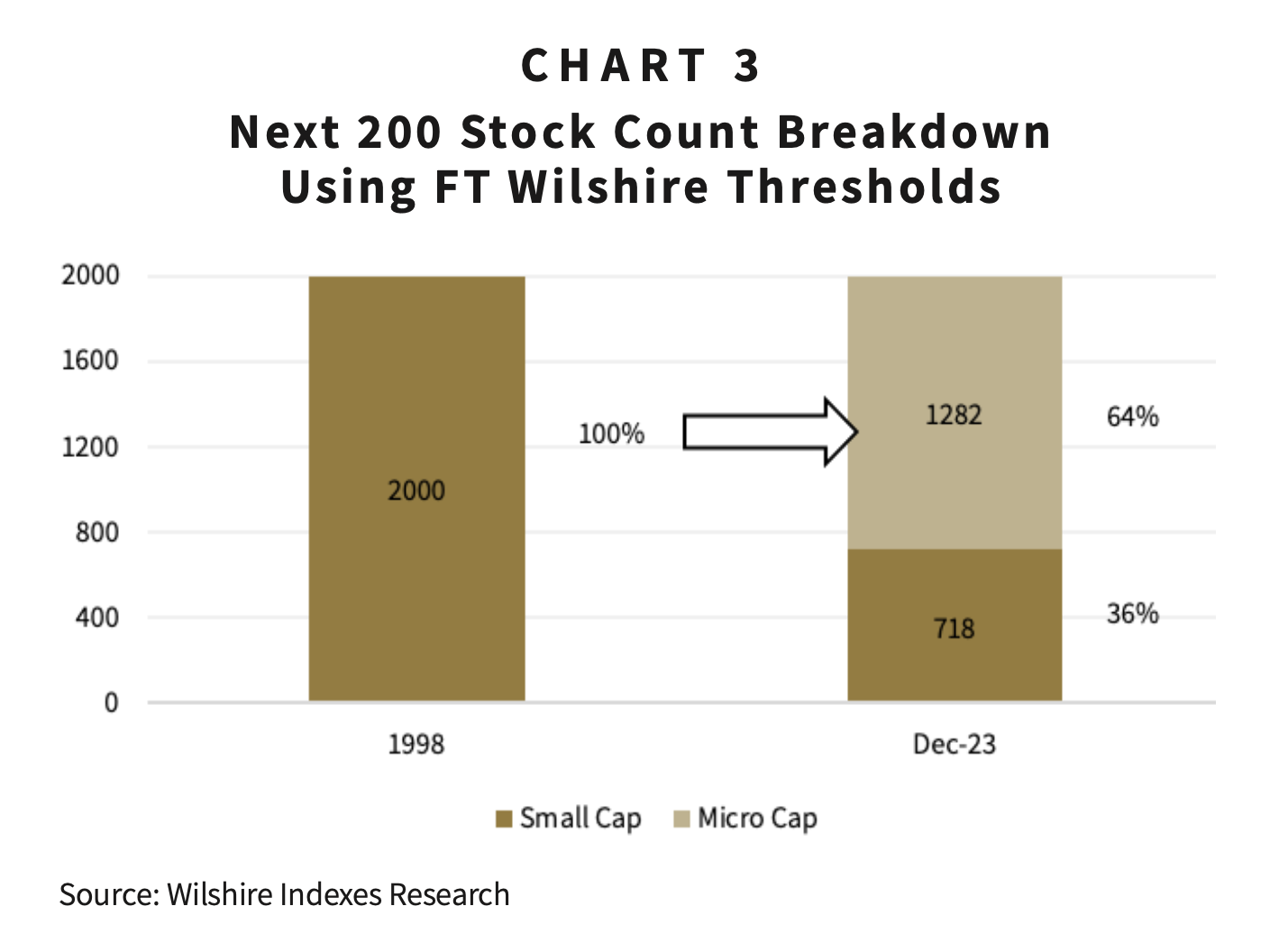

Chart 3 illustrates that when applying consistent size thresholds, based on percentage of market cap, to a universe from 1998 to that of today, the static count index holds considerably less small cap stocks and a majority of those considered micro-cap. Historically, microcaps have been a more volatile, less certain investment, classified by the SEC’s Office of Investor Education and Advocacy as “among the most risky” types of investments.5

For years, Goelzer has warned clients about the potential risks of using a static count index with no consideration for the profitability of the constituent, this market dynamic of fewer public stocks further supports our case for being thoughtful in index selection.

The structure and funding of the capital markets continue to evolve. With that in mind investors need to be aware of how these developments can affect their current portfolios and investment strategy. A declining opportunity set within the publicly traded markets should inform investors to explore additional options in the private markets. Given these developments, they should also be mindful of the underlying exposures that may have inadvertently built within their passive index funds.

At Goelzer, we are committed to ensuring our clients are aware of structural changes in the capital markets, providing access to a wide array of public and private investments and most importantly delivering education to our clients so they know what they own and why.

1 Avoid the Size Trap, Wilshire Indexes Research, April 2024, www.wilshireindexes.com/index-research-papers/avoid-the-size-trap.

2 Annual Report 2023, JPMorganChase & Co., www.jpmorganchase.com/content/dam/jpmc/jpmorgan-chase-and-co/investor-relations/documents/annualreport-2023.pdf.

3 Jay R. Ritter, University of Florida, Warrington College of Business, IPO Data, site.warrington.ufl.edu/ritter/ipo-data.

4 Hamilton Lane, “Private Market Investing: Staying Private Longer Leads to Opportunity,” April 14, 2022, www.hamiltonlane.com/en-us/insight/staying-private-longer.

5 U.S. Securities & Exchange Commission, Investor Bulletin: Microcap Stock Basics (Part 3 of 3: Risk), Oct. 21, 2016, www.sec.gov/resources-for-investors/investor-alerts-bulletins/ib_microcap_3.

DISCLAIMER: The information provided in this piece should not be considered as a recommendation to buy, sell or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.

ABOUT GOELZER: With over 50 years of experience and more than $3.5 billion in assets under advisement, Goelzer Investment Management is an investment advisory firm that leverages our proprietary investment and financial planning strategies to help successful families and institutions Dream, Invest, and Live.