Chief Investment Officer | Principal

As we enter April, investors continue to grapple with the consequences of an eventful March. We refer, of course, to the U.S. and Israel’s attack on the Republic of Iran and the evolving effects that have emerged since. For U.S. investors, those effects center on disruption in energy markets and the potential implications for economic growth, consumer prices, and interest rates. Unlike last spring’s fallout following the announcement of reciprocal tariffs (“Liberation Day”), the resolution of last month’s attacks may not be swift.

As we enter April, investors continue to grapple with the consequences of an eventful March. We refer, of course, to the U.S. and Israel’s attack on the Republic of Iran and the evolving effects that have emerged since. For U.S. investors, those effects center on disruption in energy markets and the potential implications for economic growth, consumer prices, and interest rates. Unlike last spring’s fallout following the announcement of reciprocal tariffs (“Liberation Day”), the resolution of last month’s attacks may not be swift.

First, as widely reported, the Strait of Hormuz—a critical chokepoint through which roughly 20% of the world’s oil supply typically passes, much of it destined for Asia—is effectively closed. Prior to the conflict, more than 100 oil and refined‑fuel vessels transited the strait each day; today, only a handful are able to pass through this vital corridor. Countries heavily dependent on imported oil and natural gas now face elevated risks of sustained energy price increases, creating immediate inflationary pressure and raising the prospect of slower economic growth in the months ahead.

Second, resolution of the hostilities—and the associated energy and economic disruption—depends on multiple parties, not solely the United States. Chief among them is the Iranian regime, whose overriding priority of self‑preservation complicates the prospects for a rapid de‑escalation. As a result, markets must contend with a prolonged period of uncertainty, particularly in energy prices and inflation expectations.

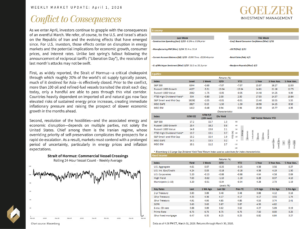

Weekly Market Update: April 1, 2026