Chief Investment Officer | Principal

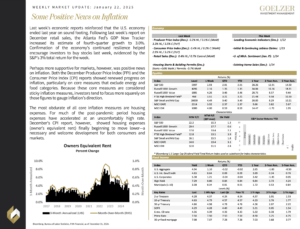

Last week’s economic reports reinforced that the U.S. economy ended last year on sound footing. Following last week’s report on December retail sales, the Atlanta Fed’s GDP Now Tracker increased its estimate of fourth-quarter growth to 3.0%. Confirmation of the economy’s continued resilience helped encourage investors to buy stocks last week, evidenced by the S&P’s 3% total return for the week.

Perhaps more supportive for markets, however, was positive news on inflation. Both the December Producer Price Index (PPI) and the Consumer Price Index (CPI) reports showed renewed progress on inflation, particularly on core measures that exclude energy and food categories. Because these core measures are considered sticky inflation measures, investors tend to focus more squarely on those figures to gauge inflation’s direction.

The most obdurate of all core inflation measures are housing expenses. For much of the post-pandemic period housing expenses have accelerated at an uncomfortably high rate. December’s CPI report, however, showed housing expenses (owner’s equivalent rent) finally beginning to move lower—a necessary and welcome development for both consumers and markets.

Weekly Market Update: January 22, 2025