Chief Investment Officer | Principal

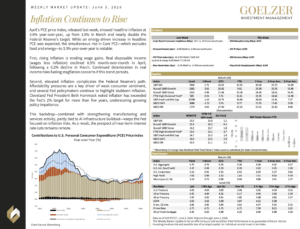

April’s PCE price index, released last week, showed headline inflation at 3.8% year-over-year, up from 3.5% in March and nearly double the Federal Reserve’s target. While an energy-driven increase in headline PCE was expected, the simultaneous rise in Core PCE—which excludes food and energy—to 3.3% year-over-year is notable.

April’s PCE price index, released last week, showed headline inflation at 3.8% year-over-year, up from 3.5% in March and nearly double the Federal Reserve’s target. While an energy-driven increase in headline PCE was expected, the simultaneous rise in Core PCE—which excludes food and energy—to 3.3% year-over-year is notable.

First, rising inflation is eroding wage gains. Real disposable income (wages less inflation) declined 0.5% month-over-month in April, following a 0.2% decline in March. Continued deterioration in real income risks fueling stagflation concerns if this trend persists.

Second, elevated inflation complicates the Federal Reserve’s path. Affordability pressures are a key driver of weak consumer sentiment, and several Fed policymakers continue to highlight stubborn inflation. Cleveland Fed President Beth Hammack noted inflation has exceeded the Fed’s 2% target for more than five years, underscoring growing policy impatience.

This backdrop—combined with strengthening manufacturing and services activity, partly tied to AI infrastructure buildout—keeps the Fed focused on inflation risks. As a result, the prospect of near-term interest rate cuts remains remote.

Weekly Market Update: June 3, 2026