Senior Portfolio Analyst

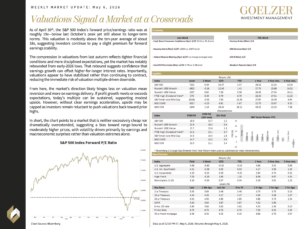

As of April 30th, the S&P 500 Index’s forward price/earnings ratio was at roughly 19x—below last October’s peak yet still above its longer-term norms. This valuation is modestly above the ten-year average of about 18x, suggesting investors continue to pay a slight premium for forward earnings stability.

As of April 30th, the S&P 500 Index’s forward price/earnings ratio was at roughly 19x—below last October’s peak yet still above its longer-term norms. This valuation is modestly above the ten-year average of about 18x, suggesting investors continue to pay a slight premium for forward earnings stability.

The compression in valuations from last autumn reflects tighter financial conditions and more disciplined expectations, yet the market has notably rebounded from early-2026 lows. That rebound suggests confidence that earnings growth can offset higher-for-longer interest rates. Importantly, valuations appear to have stabilized rather than continuing to contract, reducing the immediate risk of valuation multiple-driven downside.

From here, the market’s direction likely hinges less on valuation mean reversion and more on earnings delivery. If profit growth meets or exceeds expectations, today’s multiple can be sustained, supporting modest upside. However, without clear earnings acceleration, upside may be capped as investors remain reluctant to push valuations back toward prior highs.

In short, the chart points to a market that is neither excessively cheap nor dramatically overextended, suggesting a bias toward range-bound to moderately higher prices, with volatility driven primarily by earnings and macroeconomic surprises rather than valuation extremes alone.

Weekly Market Update: May 6, 2026